Key Takeaways

- Decentralized decision-making at Troax Group enhances agility and customer satisfaction, boosting revenue growth by aligning teams closer to market demands.

- Strategic expansion in the U.S. and APAC regions, particularly in automotive and warehousing, could improve market share and sustain revenue growth.

- Weaker demand and lower organic growth in Europe, combined with rising costs, threaten Troax Group's margins and future revenue stability.

Catalysts

About Troax Group- Through its subsidiaries, produces and sells mesh panels in the Nordic region, the United Kingdom, North America, Europe, and internationally.

- Troax Group's reorganization to decentralize decision-making and empower teams closer to customers is expected to enhance agility and cater to diverse customer preferences. This could lead to improved customer satisfaction and quicker responses to market demands, positively impacting future revenue growth.

- The expansion and progress of the factory in Tennessee, along with the planned shutdown of the current facility in Illinois, signifies a strategic move towards enhancing production capacity in the U.S., potentially leading to increased market share and revenue in this region.

- Significant growth in the APAC region, particularly in the automotive and warehousing segments, highlights a favorable market trend. Continued strong performance in these segments could sustain or increase Troax's revenue in this high-potential region.

- Active safety segment growth presents an opportunity to capitalize on a strategically important niche. Success in this area could contribute to revenue growth and improved net margins due to its specialized and potentially higher-margin nature.

- SG&A costs and employee expenses are being addressed, with potential impacts on net margins. Cost management efforts, particularly in underserved markets or segments, could improve the EBITA margin by reducing overheads relative to revenue.

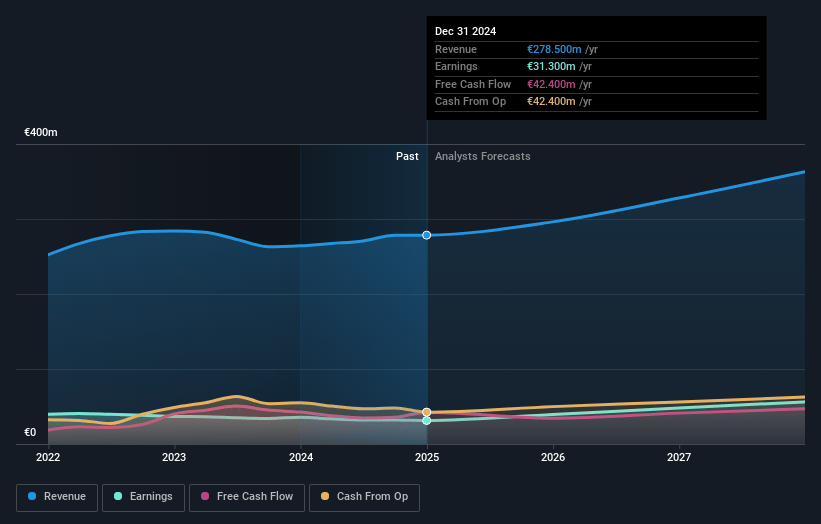

Troax Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Troax Group's revenue will grow by 6.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.8% today to 15.1% in 3 years time.

- Analysts expect earnings to reach €50.5 million (and earnings per share of €0.77) by about May 2028, up from €29.9 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €56.5 million in earnings, and the most bearish expecting €43 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 24.7x on those 2028 earnings, up from 24.5x today. This future PE is greater than the current PE for the GB Machinery industry at 21.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.84%, as per the Simply Wall St company report.

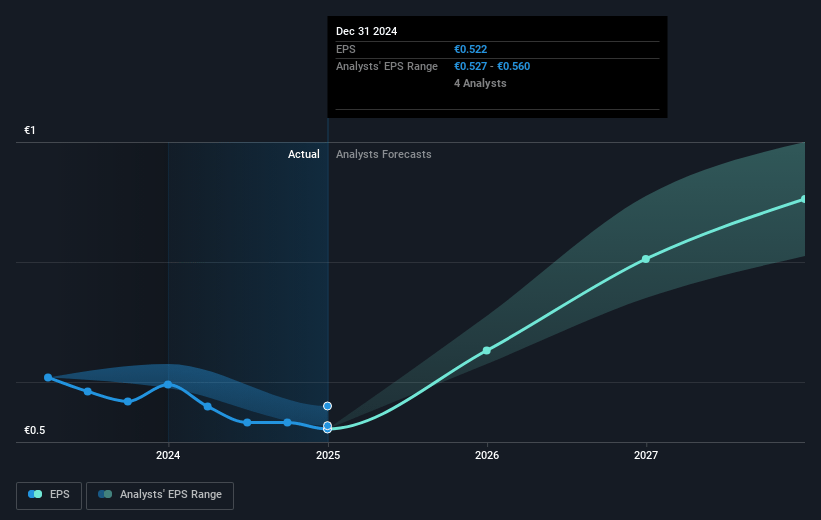

Troax Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The weaker demand in Europe, particularly in the construction market and general industry in Northern Europe, poses a risk to Troax Group's future revenue and growth prospects.

- The lower EBITA margin reported, driven by high SG&A costs and decreased production volumes in Europe, could impact Troax Group's profit margins if not addressed effectively.

- The decrease in organic growth by 5% in both order intake and sales, compared to previous year, indicates potential risks in maintaining or increasing revenue.

- Although the Americas and APAC showed growth, the reliance on a few large orders in APAC suggests potential volatility in revenue and earnings if such orders do not recur.

- Increased SG&A expenses, despite a decrease in headcount, driven by salary inflation, discretionary spending, and digitalization initiatives, might continue to pressure net margins if not controlled.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK195.83 for Troax Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK212.61, and the most bearish reporting a price target of just SEK159.86.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €333.7 million, earnings will come to €50.5 million, and it would be trading on a PE ratio of 24.7x, assuming you use a discount rate of 5.8%.

- Given the current share price of SEK134.2, the analyst price target of SEK195.83 is 31.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.