Key Takeaways

- Saab's international expansion and increased defense spending position them for substantial future revenue growth in defense products.

- Profitability improvements and strategic sustainability investments suggest potential increases in net margins and shareholder returns.

- Saab faces financial risks from geopolitical uncertainties, dependency on defense spending, project mix variability, capacity expansions, and reliance on new international fighter deals.

Catalysts

About Saab- Provides products, services, and solutions for military defense, aviation, and civil security markets Internationally.

- Saab's operational capacity ramp-up strategy, including new facilities in the U.S., India, the U.K., Finland, and additional staffing, positions them for increased future production capability. This should drive future revenue growth as demand increases for defense products.

- European defense spending trends, with countries like Sweden aiming for 3.5% of GDP, suggest increased future investments in defense capabilities. Saab is well-positioned, particularly with their Gripen Fighter and submarines, to capitalize on these increased allocations, potentially boosting future revenue and earnings.

- Saab's geographic expansion and international order backlog, now representing 74% of their business, indicate a strong pipeline for future growth. This international diversification is expected to positively impact future revenue generation.

- Profitability improvements across business units, particularly in Aeronautics, driven by currency effects and a return to profitability in Aerostructures, alongside strategic hedging, suggest a potential for increased net margins moving forward.

- Saab's proactive stance on sustainability and capacity investments highlights an operational focus on long-term growth, which could signal improved shareholder returns and a stable increase in earnings over time.

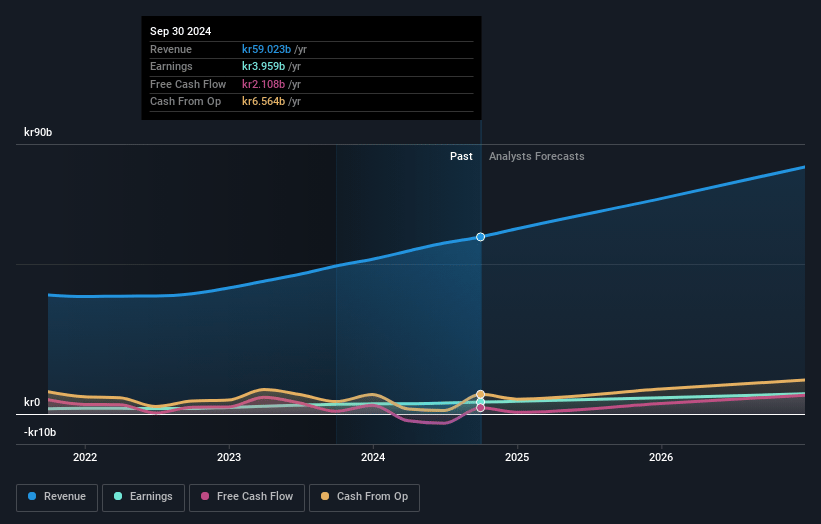

Saab Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Saab's revenue will grow by 17.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.1% today to 8.3% in 3 years time.

- Analysts expect earnings to reach SEK 8.9 billion (and earnings per share of SEK 16.41) by about May 2028, up from SEK 4.7 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 28.5x on those 2028 earnings, down from 51.4x today. This future PE is lower than the current PE for the GB Aerospace & Defense industry at 44.6x.

- Analysts expect the number of shares outstanding to grow by 0.41% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 4.82%, as per the Simply Wall St company report.

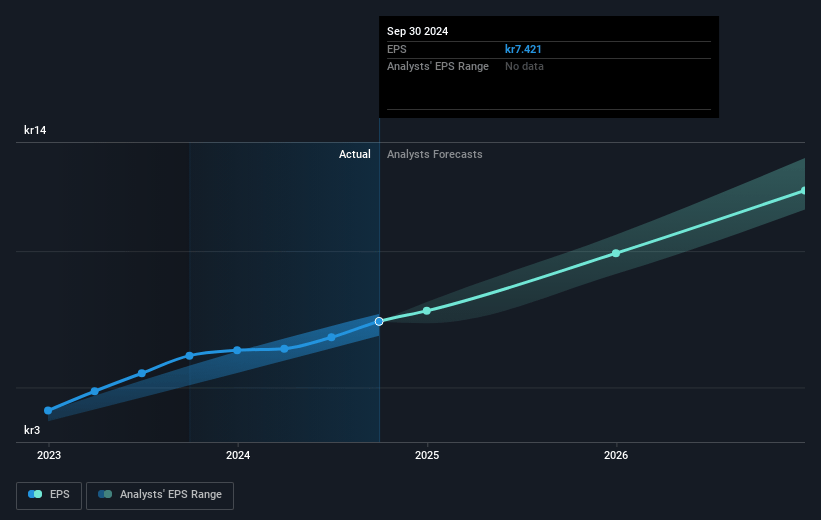

Saab Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The geopolitical uncertainties and potential trade wars could impact Saab's revenue and profitability, despite the company claiming some resilience due to regionalized supply chains.

- Saab's continued dependency on defense spending increases, especially in Europe, poses a risk if political decisions do not translate into actual contracts swiftly, potentially impacting future revenue growth.

- The fluctuation in quarterly EBIT margins due to project mix variability may lead to unpredictable earnings, especially if negative impacts occur more frequently across its business units.

- The planned production capacity expansions and increased investments, although necessary, could strain profitability if demand does not materialize as anticipated, affecting net margins.

- Saab's growth targets and cash flow projections rely significantly on the successful negotiation and completion of new international fighter deals, such as those with Thailand and Colombia, placing its future earnings at risk if these deals are delayed or fall through.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK404.143 for Saab based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK540.0, and the most bearish reporting a price target of just SEK260.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK106.1 billion, earnings will come to SEK8.9 billion, and it would be trading on a PE ratio of 28.5x, assuming you use a discount rate of 4.8%.

- Given the current share price of SEK447.9, the analyst price target of SEK404.14 is 10.8% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.