Key Takeaways

- Divesting FoodTech allows Munters to streamline operations, enhancing cash flow and margins by focusing on core areas.

- Regional production strategies and product innovation boost cost efficiency and revenue growth amidst strong demand in data centers.

- Decline in AirTech and geopolitical risks may strain revenues and margins, with increased leverage and higher costs limiting financial flexibility and earnings stability.

Catalysts

About Munters Group- Provides climate solutions in the Americas, Europe, the Middle East, Africa, and Asia.

- Munters Group has signed an agreement to divest the FoodTech equipment offering, which is expected to be completed in Q2 2025. This strategic divestiture will allow Munters to focus on its core areas, potentially improving cash flow and operating margins as operations are streamlined.

- There are plans for a step-wise improvement in the AirTech business area, with specific cost savings initiatives aimed at returning to desired profitability levels. This is likely to positively impact net margins as the company identifies further opportunities beyond the initial SEK 100 million savings target.

- Munters Group emphasizes increasing its product innovation capacity, with award-winning new products that deliver higher energy efficiencies. This focus on new, innovative products could drive revenue growth as the company addresses demand in high-growth areas like data centers.

- Munters is leveraging its regional production strategy (in the region for the region) to mitigate the impacts of tariffs and trade uncertainties. This manufacturing strategy can help maintain cost efficiency, which is beneficial for operating margins, especially given the high production utilization in key markets like the U.S.

- The company’s Data Center Technology segment reported one of its best starts to the year in terms of order intake, driven by high demand from hyperscalers and colocators. This strong order backlog, including sights set on orders filling into 2026 and beyond, is a catalyst for sustained revenue growth.

Munters Group Future Earnings and Revenue Growth

Assumptions

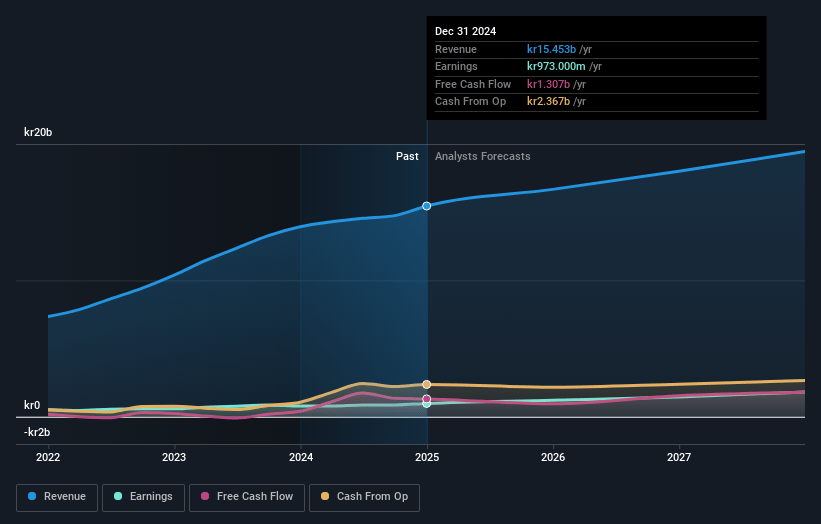

How have these above catalysts been quantified?- Analysts are assuming Munters Group's revenue will grow by 2.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.9% today to 10.3% in 3 years time.

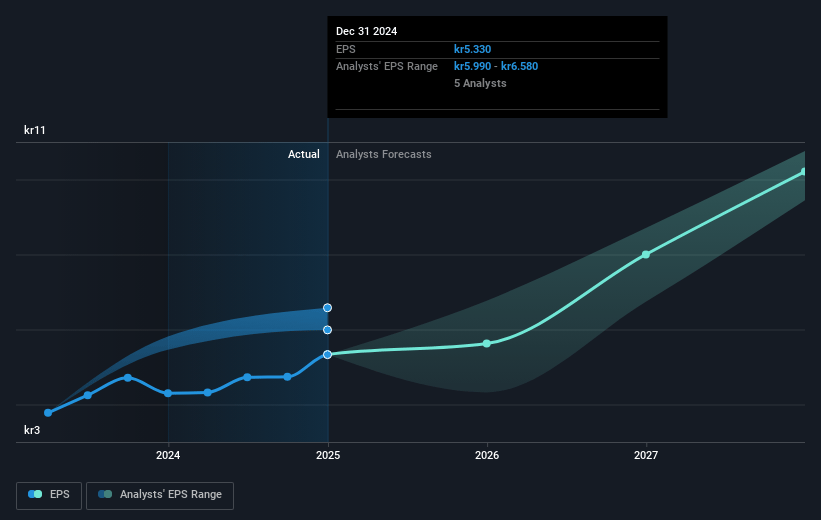

- Analysts expect earnings to reach SEK 1.8 billion (and earnings per share of SEK 8.28) by about May 2028, up from SEK 942.0 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as SEK1.4 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.5x on those 2028 earnings, down from 24.0x today. This future PE is greater than the current PE for the GB Building industry at 21.3x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.87%, as per the Simply Wall St company report.

Munters Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The decline in AirTech, particularly in battery and service sales in the Americas, suggests weakened demand in these segments that could negatively impact future revenues and margins.

- The effect of running two facilities in the U.S. has increased costs for AirTech, and while temporary, it does impact short-term net margins until resolved.

- The company's leverage has increased, causing a higher debt ratio than desired, which might limit future financial flexibility affecting earnings and cash flow.

- Weaker margins due to higher mix of controllers over software in FoodTech could lead to lower profitability, impacting net margins if this trend continues.

- Continued geopolitical uncertainties, trade wars, and tariffs pose risks to regional markets and could disrupt production strategies, potentially affecting revenues and earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK172.8 for Munters Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK220.0, and the most bearish reporting a price target of just SEK125.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK17.4 billion, earnings will come to SEK1.8 billion, and it would be trading on a PE ratio of 21.5x, assuming you use a discount rate of 6.9%.

- Given the current share price of SEK123.9, the analyst price target of SEK172.8 is 28.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.