Key Takeaways

- Boundary wire-free robotic mowers and professional irrigation expansion are key growth drivers, meeting evolving consumer needs and boosting market share.

- Simplified product range and tariff mitigation efforts focus on profitability, with cost-saving initiatives enhancing margins and earnings stability.

- Strategic shifts from CEO transition and market challenges in North America could hinder revenue growth amid economic uncertainties and currency fluctuations.

Catalysts

About Husqvarna- Produces and sells outdoor power products, watering products, and lawn care power equipment.

- The development of new boundary wire-free robotic mowers, including a record number of launches and strong growth for these products, is a key catalyst expected to drive revenue increases by capturing more market share and meeting changing consumer preferences.

- Expansion into the professional irrigation market in North America under the Husqvarna brand, utilizing recent acquisitions like ETwater, is expected to enhance revenue growth and potentially improve net margins by tapping into the high-demand water-preserving solutions market.

- Efforts to simplify the product range by reducing complexity and focusing on high-margin items, alongside cost-saving programs, are anticipated to improve net margins and profitability.

- Continued focus on professional product offerings across divisions is likely to drive stable revenue growth and improve earnings, as these segments are typically less seasonal and have higher margins compared to consumer products.

- Potential impacts of tariffs are being mitigated through price increases and strategic supply chain adjustments, which can help stabilize operating income and preserve earnings amidst uncertain economic conditions.

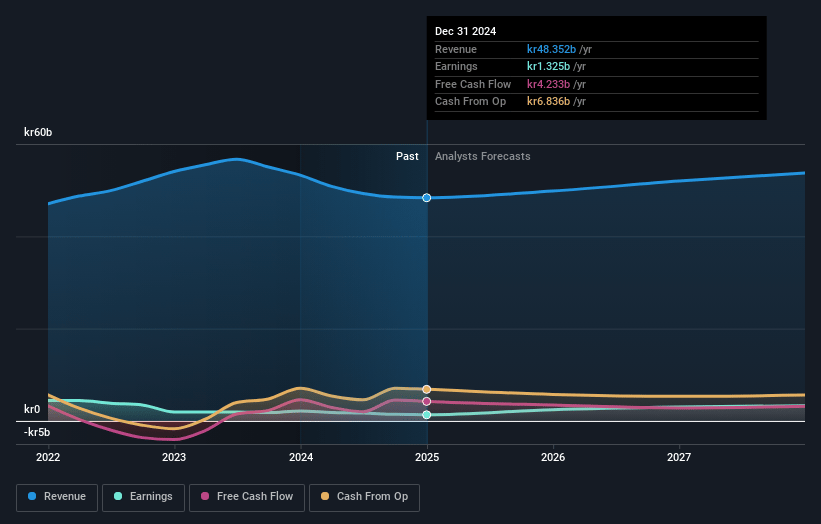

Husqvarna Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Husqvarna's revenue will grow by 2.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.0% today to 7.3% in 3 years time.

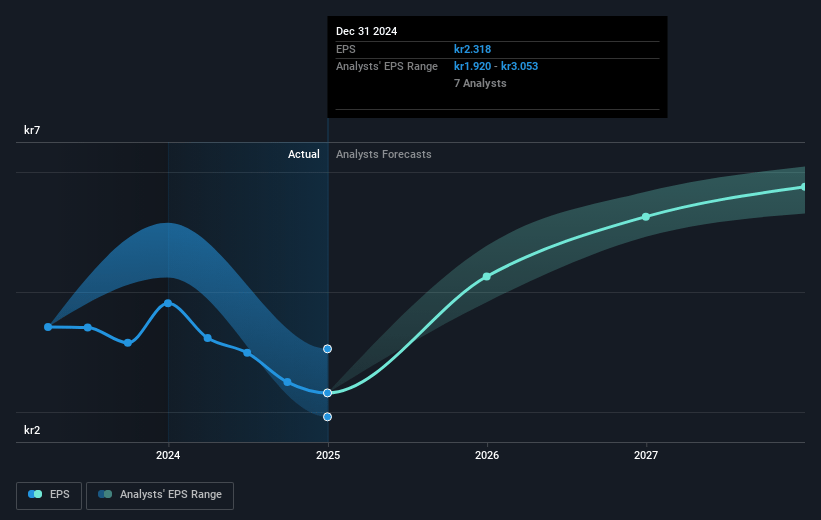

- Analysts expect earnings to reach SEK 3.8 billion (and earnings per share of SEK 5.07) by about May 2028, up from SEK 973.0 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.2x on those 2028 earnings, down from 26.5x today. This future PE is lower than the current PE for the GB Machinery industry at 21.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.0%, as per the Simply Wall St company report.

Husqvarna Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The impending CEO transition might lead to strategic shifts or instability, potentially affecting long-term growth plans and investor confidence, impacting future revenue projections.

- North America's current market challenges, evidenced by weak performance across multiple divisions, could continue to hinder sales and impair overall revenue growth in a crucial region.

- Currency fluctuations and trade tariffs are creating headwinds that decrease operating income by increasing costs or necessitating price adjustments, which could squeeze profit margins.

- Inventory levels at retail and dealer outlets are slightly on the high side, which might cause a slowdown in new product sales if demand softens, potentially impacting revenue growth.

- Sustained economic uncertainty in key markets like Germany and the U.S., including potential impacts from interest rates and geopolitical tensions, could influence consumer demand adversely, affecting sales volumes and revenue.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK61.1 for Husqvarna based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK70.0, and the most bearish reporting a price target of just SEK48.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK52.5 billion, earnings will come to SEK3.8 billion, and it would be trading on a PE ratio of 11.2x, assuming you use a discount rate of 7.0%.

- Given the current share price of SEK45.05, the analyst price target of SEK61.1 is 26.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.