Key Takeaways

- Strategic focus on defense, energy, and medtech sectors positions Freemelt to capitalize on expected growth driven by geopolitical instability and technological advancements.

- Unique technology and strategic collaborations with industry leaders and academia may bolster revenue growth through reduced costs and increased market demand.

- Reliance on few high-value sales in emerging tech makes Freemelt vulnerable to industry shifts, affecting revenue, margins, and long-term profitability.

Catalysts

About Freemelt Holding- Through its subsidiaries, engages in the metal 3D-printing business primarily in Europe and North America.

- Freemelt has a strategic focus on defense, energy, and medtech sectors, all of which are expected to see substantial growth due to geopolitical instability and technological advancements. This focus is likely to drive future revenue increases for the company.

- The company is leveraging its unique Electron Beam Powder Bed Fusion technology that reduces production cycle times, which could lead to a reduction in cost per part and improved net margins as production scales up.

- Freemelt's strategy to engage with academia and research institutes is setting the groundwork for future industrial sales, creating a pipeline of trained professionals and potential customers, eventually bolstering revenue growth.

- The growing interest in additive manufacturing from defense sectors, motivated by geopolitical instability, signals potential for faster lead times to market and increased demand, which could result in higher earnings.

- Freemelt is seeing an increase in new paid customer projects and strategic collaborations, such as with Saab Dynamics and UKAEA, signaling strong industry validation and supporting expectations of revenue growth from industrial applications.

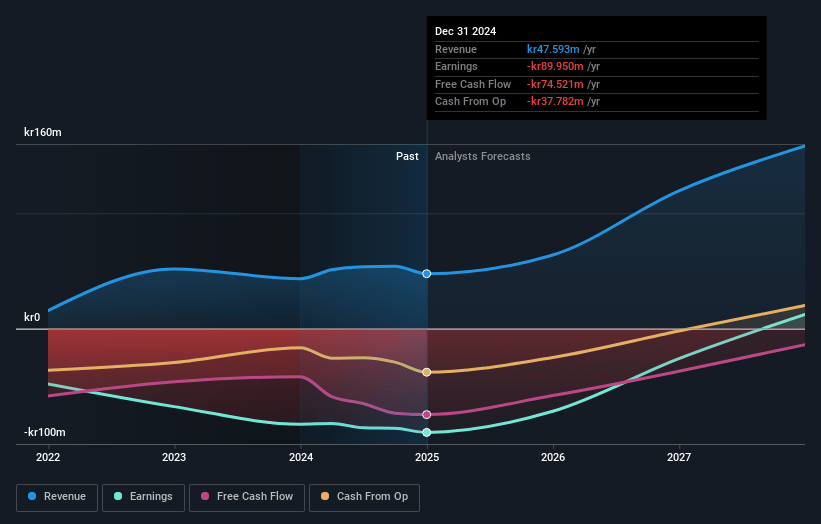

Freemelt Holding Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Freemelt Holding's revenue will grow by 49.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from -189.0% today to 7.8% in 3 years time.

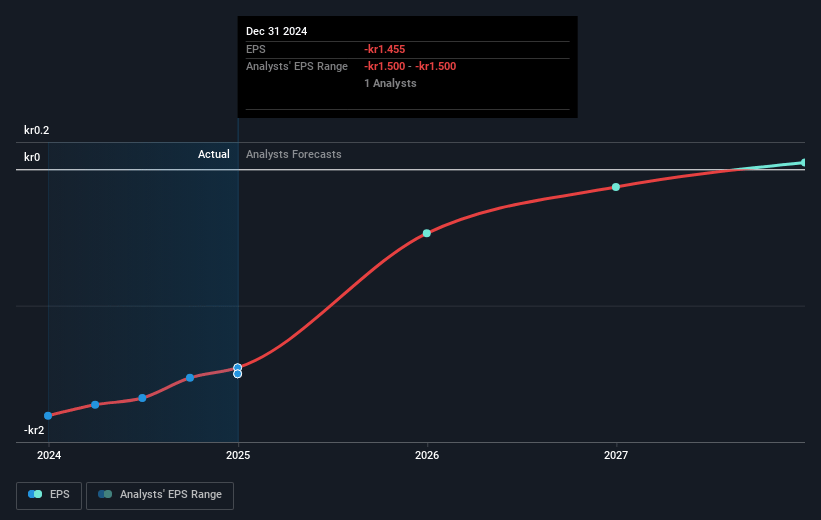

- Analysts expect earnings to reach SEK 12.3 million (and earnings per share of SEK 0.05) by about May 2028, up from SEK -90.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 22.9x on those 2028 earnings, up from -0.8x today. This future PE is greater than the current PE for the SE Machinery industry at 21.5x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.59%, as per the Simply Wall St company report.

Freemelt Holding Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Freemelt's reliance on selling a limited number of high-value machines in industrial segments like defense, energy, and medtech means its revenue is highly dependent on a few orders, making it susceptible to fluctuations if any of these industries slow down or cancel orders. This impacts revenue stability.

- The company's profitability appears to be contingent on expanding its installed base to increase aftermarket services, a segment that is currently small but related to the growing installed base. Delays in machine sales could thus significantly affect net margins and earnings.

- Freemelt's market is largely emerging technologies and speculative investments, such as fusion energy and defense applications, which may take longer to realize profits, affecting both earnings and cash flow.

- The necessity of large, sustained investment in R&D and market education to expand the adoption of additive manufacturing could continue to impact short-term profitability and cash flow.

- The geopolitical instability could potentially provide short-term sales boosts; however, it also poses risks that could slow long-term projects and investments, thereby affecting future earnings and revenue.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK2.85 for Freemelt Holding based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK4.0, and the most bearish reporting a price target of just SEK1.7.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK158.4 million, earnings will come to SEK12.3 million, and it would be trading on a PE ratio of 22.9x, assuming you use a discount rate of 5.6%.

- Given the current share price of SEK0.98, the analyst price target of SEK2.85 is 65.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.