Key Takeaways

- Significant investments in port operations and long routes may improve net margins by optimizing logistics efficiencies but could overinflate revenue expectations.

- Volatile geopolitical conditions, particularly around Ukraine, may disrupt revenue streams and raise concerns about long-term sustainability of current earnings.

- Diversification and strategic infrastructure investments are driving TTS's strong revenue growth and profitability, enhancing its financial stability and future growth potential.

Catalysts

About TTS (Transport Trade Services)- Provides freight forwarding services in Romania.

- TTS is projecting new flows of goods and multi-annual projects that are expected to drive future growth, potentially inflating revenue expectations as these initiatives develop over the next few years.

- The significant investments in port operations and the reactivation of long routes to markets like Germany and Austria could lead investors to anticipate improved net margins by optimizing logistics efficiencies.

- Temporary reduction in CapEx could create a perception of improved short-term earnings as future required expenditures are deferred, although this may not be sustainable long-term.

- The volatile geopolitical environment, particularly related to Ukraine, suggests an unstable revenue stream, with market distortions affecting commodities like grains and steel, potentially leading to the belief that current earnings might not be replicable.

- While diversifying service offerings, TTS faces potential operational oversupply and market fragmentation challenges, which could impact long-term pricing power and lead investors to overestimate the company's future revenue potential.

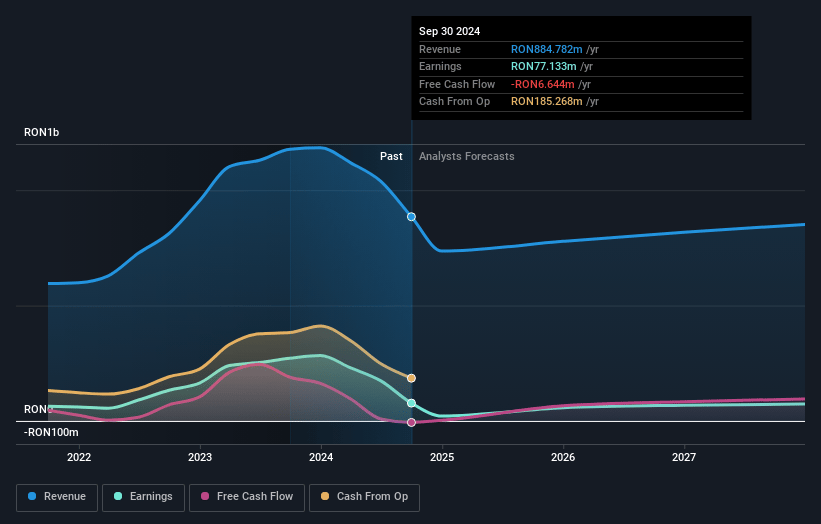

TTS (Transport Trade Services) Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming TTS (Transport Trade Services)'s revenue will decrease by -1.6% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 8.7% today to 8.5% in 3 years time.

- Analysts expect earnings to reach RON 71.7 million (and earnings per share of RON 1.58) by about January 2028, down from RON 77.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 3.9x on those 2028 earnings, down from 11.5x today. This future PE is lower than the current PE for the RO Shipping industry at 8.3x.

- Analysts expect the number of shares outstanding to decline by 36.78% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.58%, as per the Simply Wall St company report.

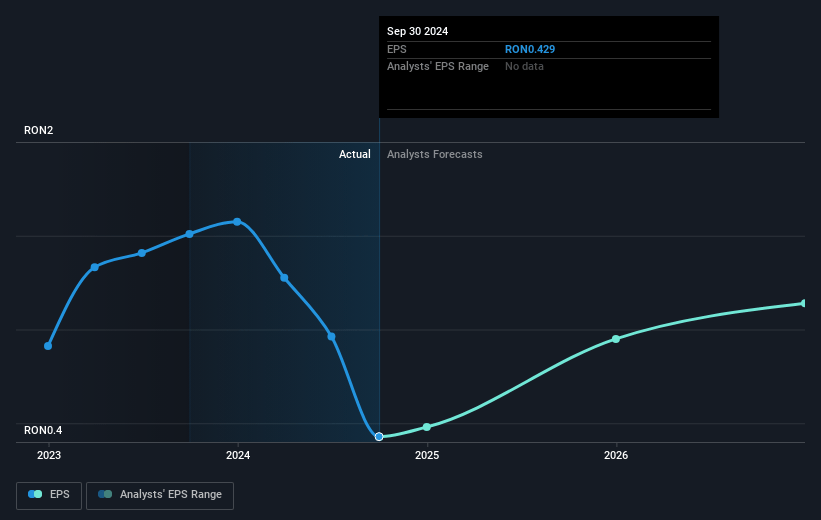

TTS (Transport Trade Services) Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- TTS experienced significant revenue growth compared to 2021, with 9-month revenues in 2023 nearly equaling the solid financial year of 2021. This indicates a strong revenue perspective overall.

- Profitability at the TTS level has almost doubled compared to the period prior to the Ukraine war, with a very good profit rate of 14.1%, suggesting potential stability or improvement in net margins.

- The company has a solid balance sheet, with a substantial increase in net assets and low exposure to loans, suggesting a strong financial position that could cushion against potential risks.

- TTS has been diversifying its operations by covering more market segments and developing new projects, which can lead to increased revenue and mitigate risks from downturns in specific markets.

- Investments in infrastructure like ports and terminals, along with strategic projects, could enhance long-term earnings and position TTS for future growth amid new economic or geopolitical conditions.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of RON4.37 for TTS (Transport Trade Services) based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be RON842.8 million, earnings will come to RON71.7 million, and it would be trading on a PE ratio of 3.9x, assuming you use a discount rate of 12.6%.

- Given the current share price of RON4.95, the analyst's price target of RON4.37 is 13.3% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.