Last Update23 Aug 25Fair value Decreased 20%

Despite Omada’s stronger-than-expected growth in members and revenue, robust gross margin gains, and improving clinical partnerships, analysts have lowered the price target from NOK44.00 to NOK35.00 due to a more cautious broader outlook.

Analyst Commentary

- Bullish analysts highlight Omada’s member and revenue growth significantly surpassing expectations, with first-quarter figures beating estimates by 6.7% and 11.5%, respectively.

- The company’s AI-powered virtual care platform is viewed as differentiated and effective in driving better engagement and health outcomes, giving Omada a distinct competitive edge in the crowded chronic-care market.

- Improved financial metrics, notably in gross margins, alongside a proven track record of clinically validated outcomes (supported by 29 peer-reviewed studies), strengthen confidence in Omada’s long-term prospects.

- Strong and expanding channel and PBM partnerships are cited as key growth levers, enhancing Omada’s ability to win new business as employers reassess chronic disease management strategies amid rising medical costs and the emergence of GLP-1 drug utilization.

- Rapid market share gains are attributed to Omada’s clinical leadership and ability to provide compelling alternatives to costly drug therapies, supporting forecasts for sustained 35%+ top-line growth and progress toward adjusted EBITDA breakeven.

Valuation Changes

Summary of Valuation Changes for Omda

- The Consensus Analyst Price Target has significantly fallen from NOK44.00 to NOK35.00.

- The Future P/E for Omda has significantly fallen from 87.38x to 52.54x.

- The Net Profit Margin for Omda has significantly risen from 2.51% to 3.28%.

Key Takeaways

- Ambitious growth and margin expectations are threatened by integration risks, compliance costs, and possible overestimation of expansion in a competitive, regulated market.

- Disruption from new technologies and constrained healthcare budgets could undermine recurring revenues and organic growth, pressuring Omda’s long-term earnings potential.

- Strong recurring revenue, disciplined M&A, and decentralized operations drive Omda’s stable growth, operational efficiency, and low-risk profile with increasing earnings and reinvestment potential.

Catalysts

About Omda- Provides software solutions for healthcare sector in Norway, Sweden, Denmark, Finland, and internationally.

- The market appears to be pricing in aggressive, sustained revenue growth assumptions based on Omda’s stated intention to double its business again via a mix of 5–10% organic growth and an additional 25–30% annual growth through M&A, which is ambitious given the potential for industry consolidation, elevated acquisition risks, and competitive pressures—placing future top-line targets at risk.

- Investor expectations for continued margin expansion (from a 22% EBITDA margin towards a 30% target in 2026), seem elevated after a recent structural reorganization and cost-cutting cycle, but rising compliance costs from tightening data privacy regulation and necessary cybersecurity investments may limit further net margin improvement over the long-term.

- There is optimism around low recurring revenue churn (under 2%) and high visibility, but the increasing adoption of generative AI and automation in healthcare could disrupt existing health IT business models, potentially threatening Omda’s legacy recurring revenue streams if adaptation is insufficient, thus putting future earnings at risk.

- Forecasts may be overlooking mounting healthcare budget constraints in developed markets, which—driven by aging populations and public sector cost pressures—could dampen both new IT contract wins and expansionary upgrades, resulting in slower organic revenue and earnings growth than currently implied in the share price.

- The current valuation likely assumes that Omda will be able to outpace intensifying competition from large multinational EHR and digital health vendors; failure to maintain pricing power and technological leadership could erode revenue growth and compress margins over time.

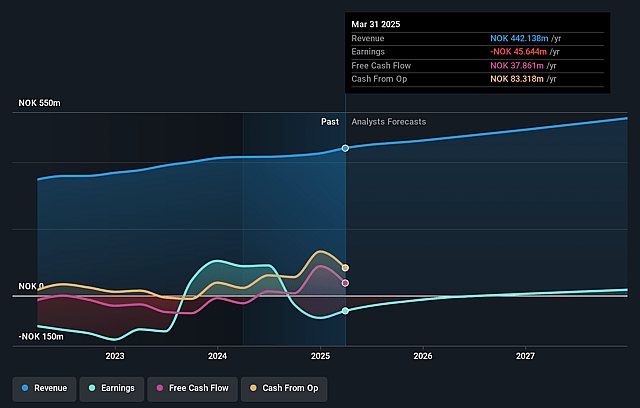

Omda Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Omda's revenue will grow by 6.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from -10.3% today to 3.3% in 3 years time.

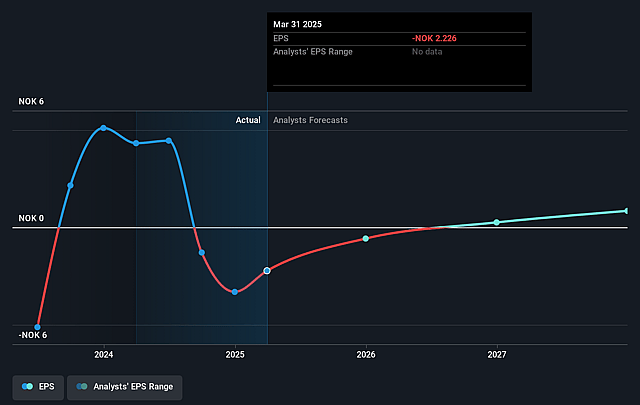

- Analysts expect earnings to reach NOK 17.7 million (and earnings per share of NOK 0.7) by about August 2028, up from NOK -45.6 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 52.6x on those 2028 earnings, up from -22.2x today. This future PE is greater than the current PE for the NO Healthcare Services industry at 35.5x.

- Analysts expect the number of shares outstanding to grow by 1.62% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.19%, as per the Simply Wall St company report.

Omda Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Omda's exceptionally high share (~90%) of recurring and semi-recurring revenue, with less than 2% customer churn and public sector-heavy customer base, suggests very strong revenue visibility and stability, which, if sustained, greatly reduces risk to long-term revenue and earnings.

- The company has demonstrated consistent profitable organic growth—15% YoY in Q1 2025—and targets continued organic growth of 5–10% per year, alongside EBITDA margins set to increase to 30% by 2026, indicating a well-executed operating model that supports expanding net margins and earnings.

- Omda’s disciplined acquisition strategy, including the successful integration of recent targets (Dermicus, Aweria, Predicare), continual process improvement (“buy, integrate, and build”), and leverage of cross-selling within complex value chains, positions it for further accelerated topline growth and diversified revenue streams via M&A.

- The transition to a fully decentralized structure has driven sustainable cost reductions, improved agility, and enabled additional scalability, resulting in both immediate and likely ongoing improvements in operational margins and cash flow.

- Management’s demonstrated focus on deleveraging (net debt/EBITDA trending below 3x), rigorous cash management, minimal near-term refinancing needs, and access to additional untapped bond capacity, all lower financial risk and create runway for reinvestment, further enhancing earnings stability and potential shareholder value.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of NOK35.0 for Omda based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be NOK539.6 million, earnings will come to NOK17.7 million, and it would be trading on a PE ratio of 52.6x, assuming you use a discount rate of 8.2%.

- Given the current share price of NOK49.4, the analyst price target of NOK35.0 is 41.1% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.