Key Takeaways

- Significant investments in R&D and product launches might strain profitability if they don't lead to expected revenue gains.

- Expansion and strategic goals face challenges, which could impact net margins and future revenue growth if not effectively managed.

- Medistim's steady profits, promising geographic expansion, advanced software, strong cash flow, and strategic studies bolster its revenue, competitive edge, and future growth potential.

Catalysts

About Medistim- Develops, produces, services, leases, and distributes medical devices for cardiac and vascular surgery in the United States, Europe, Asia, and internationally.

- Medistim's significant investment in R&D and new product launches, particularly the INTUI software platform, raises operational expenses. This could impact net margins and profitability if these investments do not lead to expected revenue increases.

- Expansion efforts, especially in direct markets like China, Canada, and Sweden, involve higher operational costs. Combined with challenges in Asia Pacific, these could suppress net margins or earnings if not offset by sufficient revenue growth.

- The company's strategy to convert existing flow technology users to imaging in mature markets and penetrate lower-penetration markets might not yield the expected revenue increase. If these strategic goals are not met, it could impact future revenue streams.

- The rapid growth seen in the Americas might not be sustainable, given past fluctuations and macroeconomic uncertainties. An inability to maintain growth could potentially affect revenue and profit forecasts.

- The ongoing expenses related to clinical marketing studies and the direct market presence investment might weigh on cash flow, potentially affecting net margins and earnings if they do not translate into successful market expansion or product adoption.

Medistim Future Earnings and Revenue Growth

Assumptions

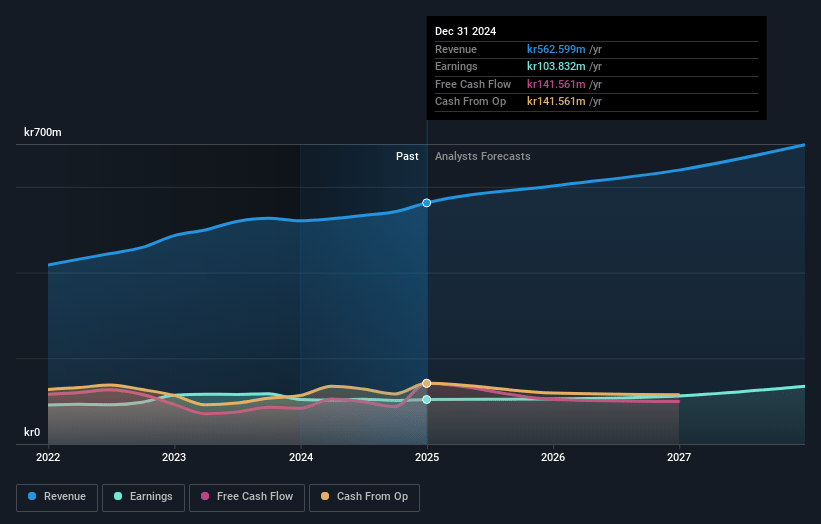

How have these above catalysts been quantified?- Analysts are assuming Medistim's revenue will grow by 7.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 18.5% today to 19.3% in 3 years time.

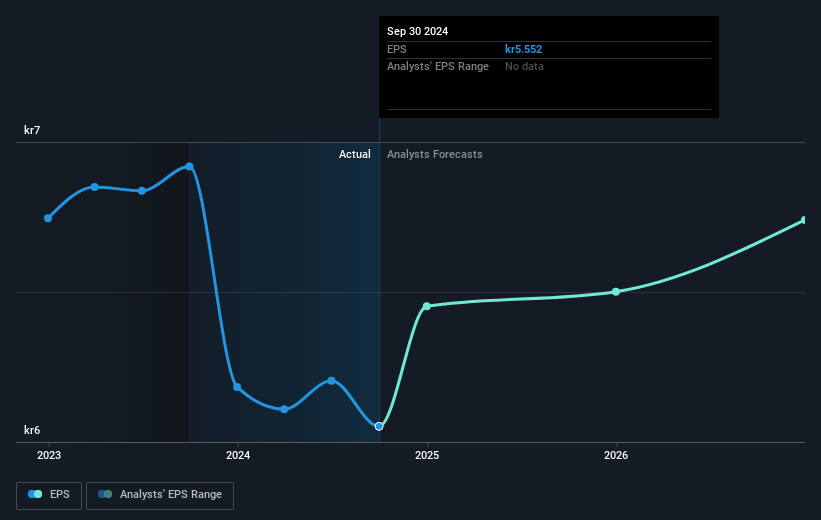

- Analysts expect earnings to reach NOK 135.0 million (and earnings per share of NOK 7.35) by about March 2028, up from NOK 103.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 27.7x on those 2028 earnings, down from 33.9x today. This future PE is greater than the current PE for the GB Medical Equipment industry at 24.9x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.49%, as per the Simply Wall St company report.

Medistim Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Medistim has consistently achieved profitable growth and has a history of delivering on its financial promises, suggesting potential revenue and earnings stability in the future.

- The company reported an all-time high in quarterly sales, with notable growth in the Americas and EMEA regions, indicating strong revenue potential and geographic diversification.

- The introduction of the INTUI software, with positive feedback from users and plans for premium pricing, could contribute to increased revenue through both direct sales and upgrade kits.

- Medistim maintains a solid cash flow position, with increased cash from operations and a strong cash balance, potentially supporting future profitability and enabling investment in growth areas.

- The launch of the PATENT study in vascular surgery, with involvement from leading experts, could enhance Medistim's competitive position and future earnings in this segment.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of NOK172.0 for Medistim based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be NOK698.1 million, earnings will come to NOK135.0 million, and it would be trading on a PE ratio of 27.7x, assuming you use a discount rate of 6.5%.

- Given the current share price of NOK192.0, the analyst price target of NOK172.0 is 11.6% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.