Key Takeaways

- Strategic investments in new facilities enhance production efficiency and reduce mortality rates, likely improving future margins and earnings.

- Initiating refinancing processes seeks better financing terms, reducing interest expenses and enhancing net earnings potential.

- Biological incidents and loan covenant breaches have impacted Kaldvik's financial stability, while reliance on licensing approvals poses ongoing regulatory risks to future revenue.

Catalysts

About Kaldvik- Ice Fish Farm AS engages in the salmon farming business in Iceland.

- The anticipated approval of the new license in Seyðisfjörður will allow an increase in production capacity, potentially enhancing future revenue as it supports higher production volumes and reduces biological risks at sea.

- Strategic investments in new facilities and capacity, such as the new grow-out facility and improved well-boat capacity, are set to increase production efficiency and reduce mortality rates, likely improving future net margins and earnings.

- The acquisition of the Box factory and full ownership of the harvesting station in Djupivogur is expected to lower packaging costs by €3 million annually, improving net margins as Kaldvik scales operations.

- Implementation of a vaccination program against winter wounds and ISA is likely to lead to lower mortality rates, stabilizing harvest volumes and potentially boosting revenue and earnings predictability.

- Initiating refinancing processes with their syndicate loan partners is aimed at securing more favorable financing terms, which could reduce interest expenses and enhance future net earnings.

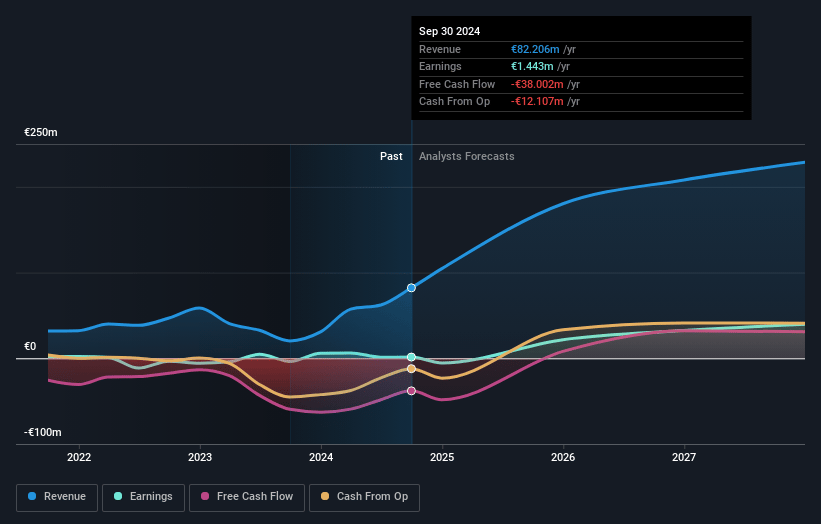

Kaldvik Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Kaldvik's revenue will grow by 33.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from -29.2% today to 16.4% in 3 years time.

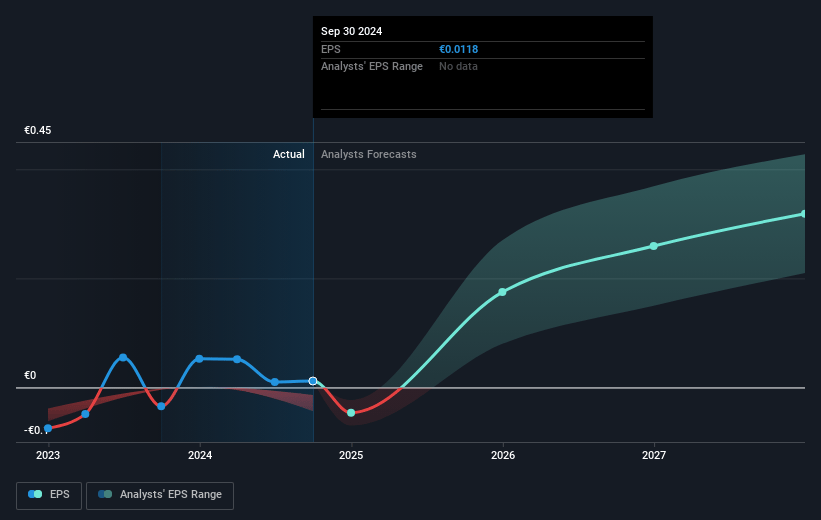

- Analysts expect earnings to reach €38.5 million (and earnings per share of €0.3) by about March 2028, up from €-28.7 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €48.7 million in earnings, and the most bearish expecting €28.3 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.0x on those 2028 earnings, up from -8.1x today. This future PE is lower than the current PE for the NO Food industry at 21.0x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.71%, as per the Simply Wall St company report.

Kaldvik Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Biological incidents and high mortality rates significantly affected Kaldvik's financial results, with a biomass write-down of €23.1 million impacting net margins and future revenue projections.

- The smolt release challenges, including a shortfall of 1.2 million smolt, led to missed output targets that could negatively influence revenue and future harvest volumes.

- The company breached certain loan covenants in Q4 and is undergoing a refinancing process, which signals potential financial instability and could impact net earnings if not resolved.

- Adverse weather conditions and insufficient well-boat capacity hindered harvesting efforts, contributing to rising operational costs and potentially affecting overall profitability.

- Continued reliance on successful licensing approvals, such as the pending 10,000-tonne license in Seyðisfjörður, introduces regulatory risk which could affect future revenue and production forecasts if not secured.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of NOK29.5 for Kaldvik based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €234.2 million, earnings will come to €38.5 million, and it would be trading on a PE ratio of 12.0x, assuming you use a discount rate of 6.7%.

- Given the current share price of NOK22.0, the analyst price target of NOK29.5 is 25.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.