Key Takeaways

- Improved fishery quotas and production efficiencies across regions are set to boost volumes and potentially enhance revenues and earnings.

- A robust balance sheet with strong equity and cash reserves enables strategic investments and potential acquisitions for future growth.

- Quota reductions, price fluctuations, and increased competition may strain revenue and margins across various segments, impacting overall profitability and earnings.

Catalysts

About Austevoll Seafood- A seafood company, engages in the production of salmon and trout, white fish, and pelagic in Norway, the European Union, the United Kingdom, Eastern Europe, Africa, North America, Asia, and South America.

- The significant improvement in fishery quotas in Peru, with a 300% increase in total quota compared to 2023, sets the stage for higher production volumes of fishmeal and fish oil in 2025. This is expected to positively impact revenues, as increased supply can lead to greater sales even if prices are pressured.

- The ongoing positive biological development in Lerøy, such as the higher biomass and improved farming technologies, can enhance salmon production efficiency, reducing costs and potentially improving net margins and earnings as volumes are expected to rise in 2025.

- Expansion in Chile, which has experienced significant growth in fishery volumes of horse mackerel and mackerel, is poised for continued strong utilization of both fishing vessels and processing plants, benefiting revenue and earnings due to high catch volumes and efficient production.

- Increased activity in direct human consumption production in the North Atlantic and ongoing improvements in market demand suggest a positive outlook for revenue growth in the food segment, driven by higher volumes and better market pricing.

- The strong balance sheet with an equity ratio of 53% and substantial cash reserves positions Austevoll Seafood for strategic investments and potential acquisitions, enabling future growth and increased earnings potential.

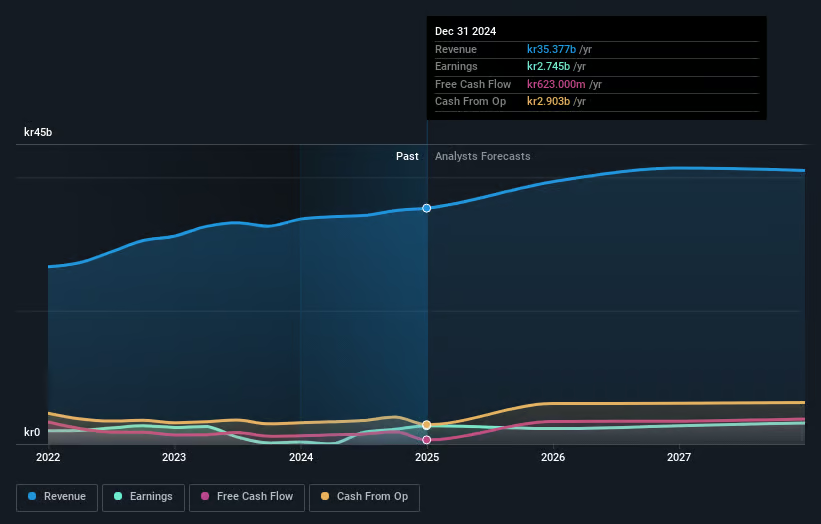

Austevoll Seafood Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Austevoll Seafood's revenue will grow by 4.5% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 7.8% today to 7.5% in 3 years time.

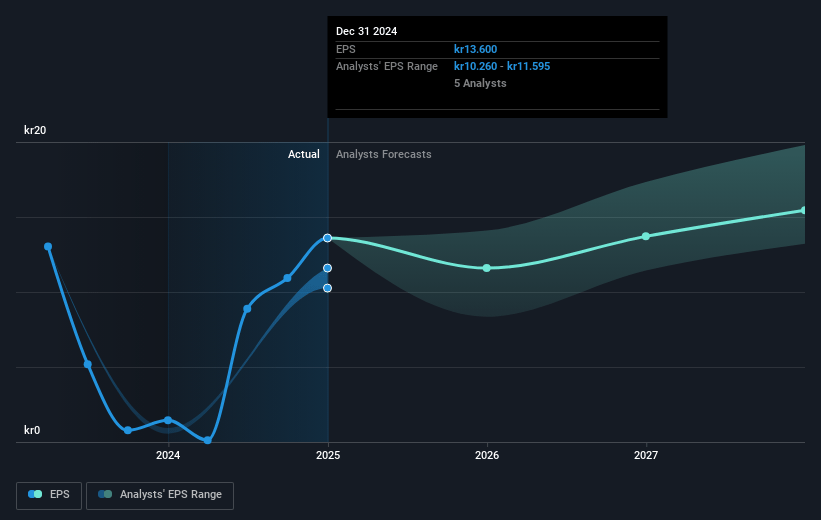

- Analysts expect earnings to reach NOK 3.0 billion (and earnings per share of NOK 15.36) by about May 2028, up from NOK 2.7 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting NOK3.8 billion in earnings, and the most bearish expecting NOK2.5 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 9.4x on those 2028 earnings, up from 7.2x today. This future PE is lower than the current PE for the GB Food industry at 20.8x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.94%, as per the Simply Wall St company report.

Austevoll Seafood Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Reduced quotas and increased competition, particularly in the North Atlantic, could lead to lower volumes, putting pressure on revenue and potentially squeezing margins.

- Lower fishmeal and fish oil prices due to increased production in Peru might reduce the profitability of these segments, impacting net margins.

- The ongoing allocation discussions related to fishing quotas in Chile may lead to unfavorable outcomes, possibly affecting future catch volumes and subsequently, earnings.

- Challenges in the wild catch segment, driven by quota reductions and higher land-based costs, could strain financial performance, affecting net margins in those areas.

- Fluctuating salmon spot prices and associated costs in Norway could lead to variability in profit margins, influencing overall earnings from the farming segment.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of NOK120.167 for Austevoll Seafood based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be NOK40.4 billion, earnings will come to NOK3.0 billion, and it would be trading on a PE ratio of 9.4x, assuming you use a discount rate of 5.9%.

- Given the current share price of NOK97.4, the analyst price target of NOK120.17 is 18.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.