Key Takeaways

- Strategic offshore wind investments and acquisition strategies aim to capture market recovery and enhance long-term equity returns and renewable portfolio growth.

- Operational optimizations and cost control in key assets position Equinor for sustained revenue growth and increased earnings amidst high energy prices.

- Inflationary pressures, unhedged gas price exposure, and costly renewable investments may constrain Equinor's capital efficiency, net margins, and short-term shareholder returns.

Catalysts

About Equinor- An energy company, engages in the exploration, production, transportation, refining, and marketing of petroleum and other forms of energy in Norway and internationally.

- The strategic countercyclical investment in Orsted is aimed at leveraging the current challenges in the offshore wind industry, which Equinor believes will yield value as the market recovers, potentially enhancing revenue and long-term returns on equity.

- Continued operational optimizations at the Johan Sverdrup field, including improved water management and drilling of new wells, are expected to extend the plateau production period, directly impacting revenues positively and sustaining cash flow.

- Equinor's acquisition strategy in offshore wind energy reflects a focus on securing competitive returns with lower CapEx compared to organic development, likely improving long-term earnings and augmenting the renewable portfolio.

- The ongoing development and planned derisking of major projects like Empire Wind and Dogger Bank, along with Europe’s increasing LNG demand, position Equinor to capitalize on high energy prices, expectedly boosting operating income and net margins.

- Cost control measures amidst inflation and strategic operational efficiencies, alongside plans to extend production plateau for key assets, suggest a potential upward trajectory in earnings and margins, as execution risks decrease over time.

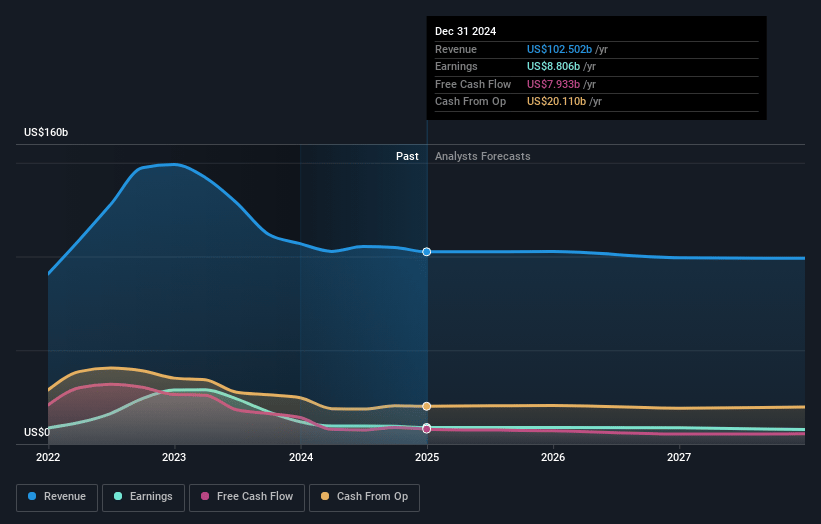

Equinor Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Equinor's revenue will decrease by 1.8% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 8.6% today to 7.8% in 3 years time.

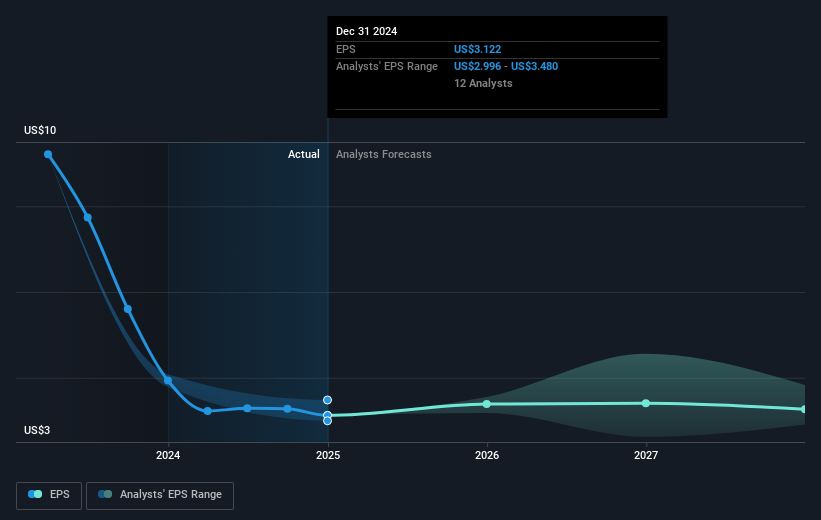

- Analysts expect earnings to reach $7.5 billion (and earnings per share of $3.22) by about May 2028, down from $8.8 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $8.4 billion in earnings, and the most bearish expecting $6.7 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 9.7x on those 2028 earnings, up from 7.1x today. This future PE is greater than the current PE for the GB Oil and Gas industry at 4.4x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Equinor Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The high cost of acquiring seabed leases and inflationary pressures in the renewables sector could constrain Equinor's capital efficiency and impact its net margins and earnings.

- The decision not to hedge gas prices leaves Equinor fully exposed to potential volatility and price declines in the European gas market, which could affect its revenue and earnings.

- The investment in Orsted, despite being seen as a long-term value opportunity, currently generates no cash flow and might not contribute to immediate financial returns, impacting short-term revenue.

- Delays and political uncertainties around projects like Rosebank, combined with potential legal and tax issues, could increase operational risks and ultimately affect Equinor's future revenues.

- Although Equinor pursues growth in renewable and low-carbon sectors, the potential lack of immediate cash dividends from investments such as Orsted may impact overall shareholder returns and net margins in the short term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of NOK283.071 for Equinor based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of NOK392.41, and the most bearish reporting a price target of just NOK210.22.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $97.0 billion, earnings will come to $7.5 billion, and it would be trading on a PE ratio of 9.7x, assuming you use a discount rate of 7.1%.

- Given the current share price of NOK237.9, the analyst price target of NOK283.07 is 16.0% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.