Key Takeaways

- Strategic partnerships with industrial leaders and successful large-scale projects could significantly expand market reach and drive substantial revenue growth for HydrogenPro.

- Planned cost-saving measures and supply chain optimizations aim to improve operational efficiency, enhancing net margins and earnings potential.

- Geopolitical tensions and market competition threaten HydrogenPro's revenue, while operating losses and uncertain project timelines challenge investor confidence and financial stability.

Catalysts

About HydrogenPro- Engages in designing and delivering green hydrogen technology and systems in Norway, Europe, the United States, and the Asia Pacific.

- The commissioning of the new electrode line in Denmark and full-scale testing of Stack 1 with ANDRITZ are expected to significantly enhance technology efficiency and product offerings, potentially boosting future revenue opportunities.

- Strategic partnerships with major industrial partners like LONGi, ANDRITZ, and Mitsubishi are expected to enhance supply chain optimization and expand HydrogenPro’s market reach, potentially improving revenue growth and net margins.

- The successful delivery of large-scale projects like SALCOS and ACES, combined with HydrogenPro’s solid track record, positions the company to benefit from increasing market demands, which could drive substantial revenue growth.

- The cost-saving measures planned for 2025, such as downsizing and optimizing the supply chain in Tianjin, are intended to improve operational efficiency, positively impacting net margins and earnings.

- The formation of partnerships facilitating a full scope offering, including EPC services, enhances project bankability and potentially increases customer acquisition, thus positively affecting future revenue and leading to higher earnings growth.

HydrogenPro Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming HydrogenPro's revenue will grow by 155.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from -100.2% today to 4.4% in 3 years time.

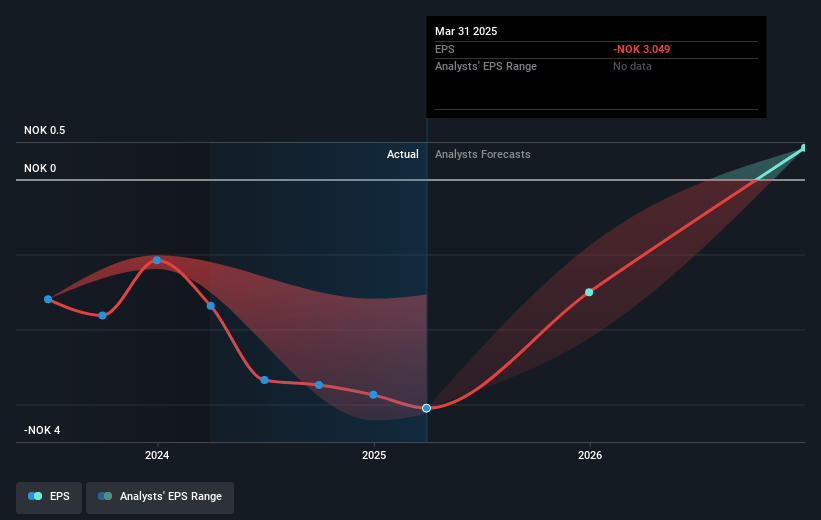

- Analysts expect earnings to reach NOK 144.3 million (and earnings per share of NOK 0.85) by about May 2028, up from NOK -196.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 25.7x on those 2028 earnings, up from -1.6x today. This future PE is greater than the current PE for the NO Machinery industry at 15.8x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.03%, as per the Simply Wall St company report.

HydrogenPro Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The geopolitical uncertainties and unpredictability, such as geopolitical tensions, the market being slower than expected, and increased competition from Chinese OEMs, could negatively impact HydrogenPro's revenue projections and market share.

- The company is currently operating at a net loss, with an EBITDA of minus NOK 44 million and a net loss of NOK 38 million in the fourth quarter, which could affect investor confidence in the company's profitability in the near term.

- There are cost-saving measures being implemented due to the slow market, including downsizing in Europe and reducing activity in Tianjin, which could impact production capacity and revenue generation in the short term.

- The liquidity position of HydrogenPro may be at risk if there are any delays in receiving the remaining NOK 70 million from LONGi, which is contingent upon approval by Chinese authorities, potentially affecting cash flow and financial stability.

- There is uncertainty regarding the final investment decisions and development timelines for several projects in the pipeline, such as DG Fuels, which could impact future revenue and earnings realizations.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of NOK29.993 for HydrogenPro based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of NOK49.96, and the most bearish reporting a price target of just NOK10.02.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be NOK3.2 billion, earnings will come to NOK144.3 million, and it would be trading on a PE ratio of 25.7x, assuming you use a discount rate of 7.0%.

- Given the current share price of NOK3.84, the analyst price target of NOK29.99 is 87.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.