Key Takeaways

- Leadership changes and strategic positioning in growing markets like e-commerce aim to boost long-term revenue and modernize customer engagement.

- Focus on OpEx-based deals and product innovation could improve revenue predictability, market reach, and gross margins despite economic challenges.

- Macroeconomic challenges, uncertain project deliveries, and potential U.S. tariffs pose revenue and margin risks, while a shift to OpEx deals may affect cash flow stability.

Catalysts

About AutoStore Holdings- A robotic and software technology company, provides warehouse automation solutions in Norway, Germany, rest of Europe, the United States, Asia, and internationally.

- AutoStore's leadership change with the appointment of Keith White as Chief Commercial Officer, who brings extensive experience in transforming business strategies within tech giants, aims to drive market awareness and modernize customer engagement, potentially enhancing revenue growth.

- The company is strategically positioned in an underpenetrated market with expected growth driven by secular trends like e-commerce adoption and warehouse automation, which could boost long-term revenue.

- AutoStore's development of OpEx-based deals presents a new revenue stream that could improve the predictability and stability of future cash flows and revenues.

- The company's solid pipeline and market share gains amidst a challenging macroeconomic environment suggest promising potential for future revenue growth once market conditions stabilize.

- Investment in product innovation, with upcoming software and hardware announcements, supports an expansion of AutoStore's market reach, which could positively impact future revenue and gross margins.

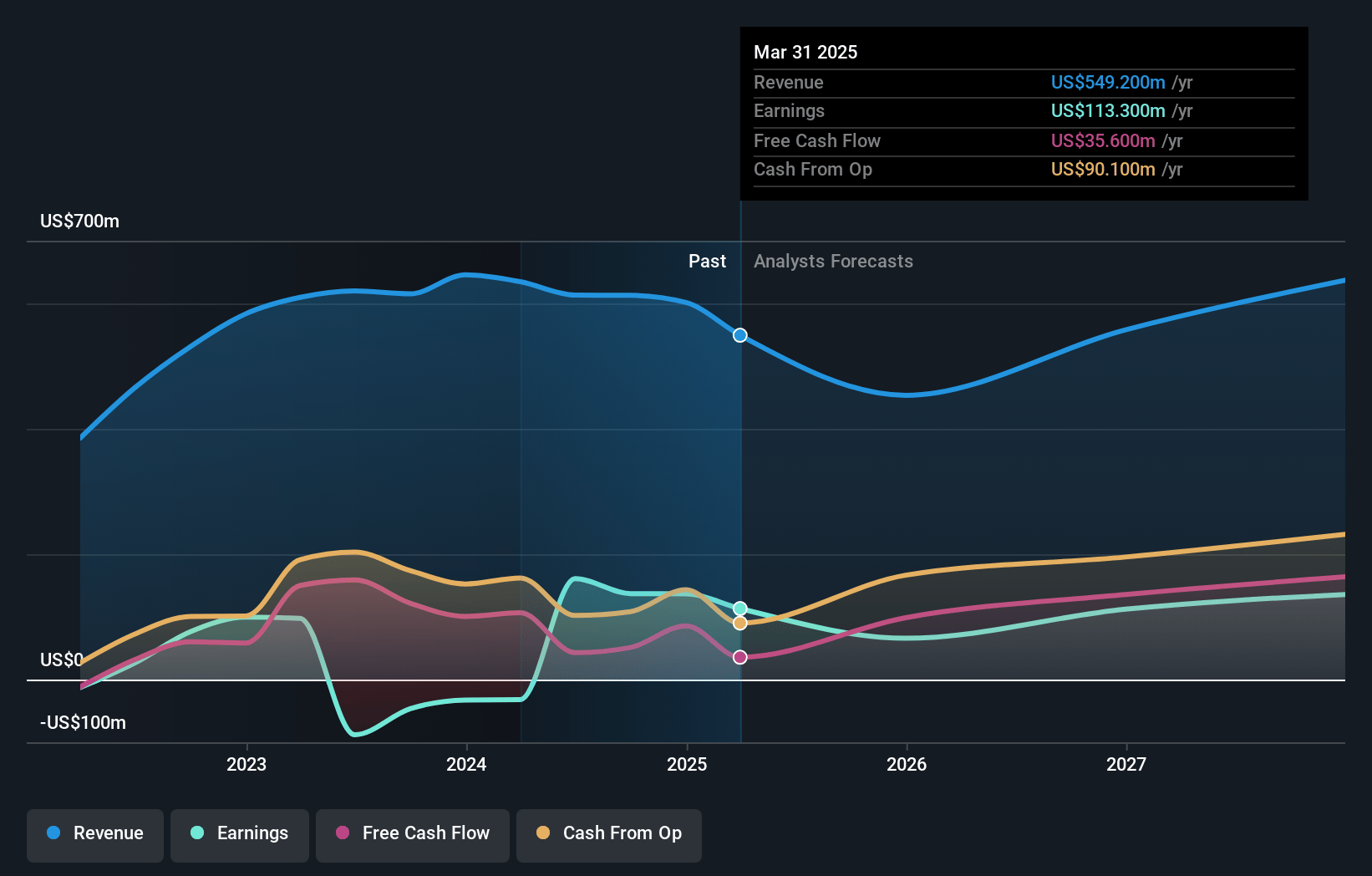

AutoStore Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming AutoStore Holdings's revenue will grow by 7.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 22.7% today to 24.3% in 3 years time.

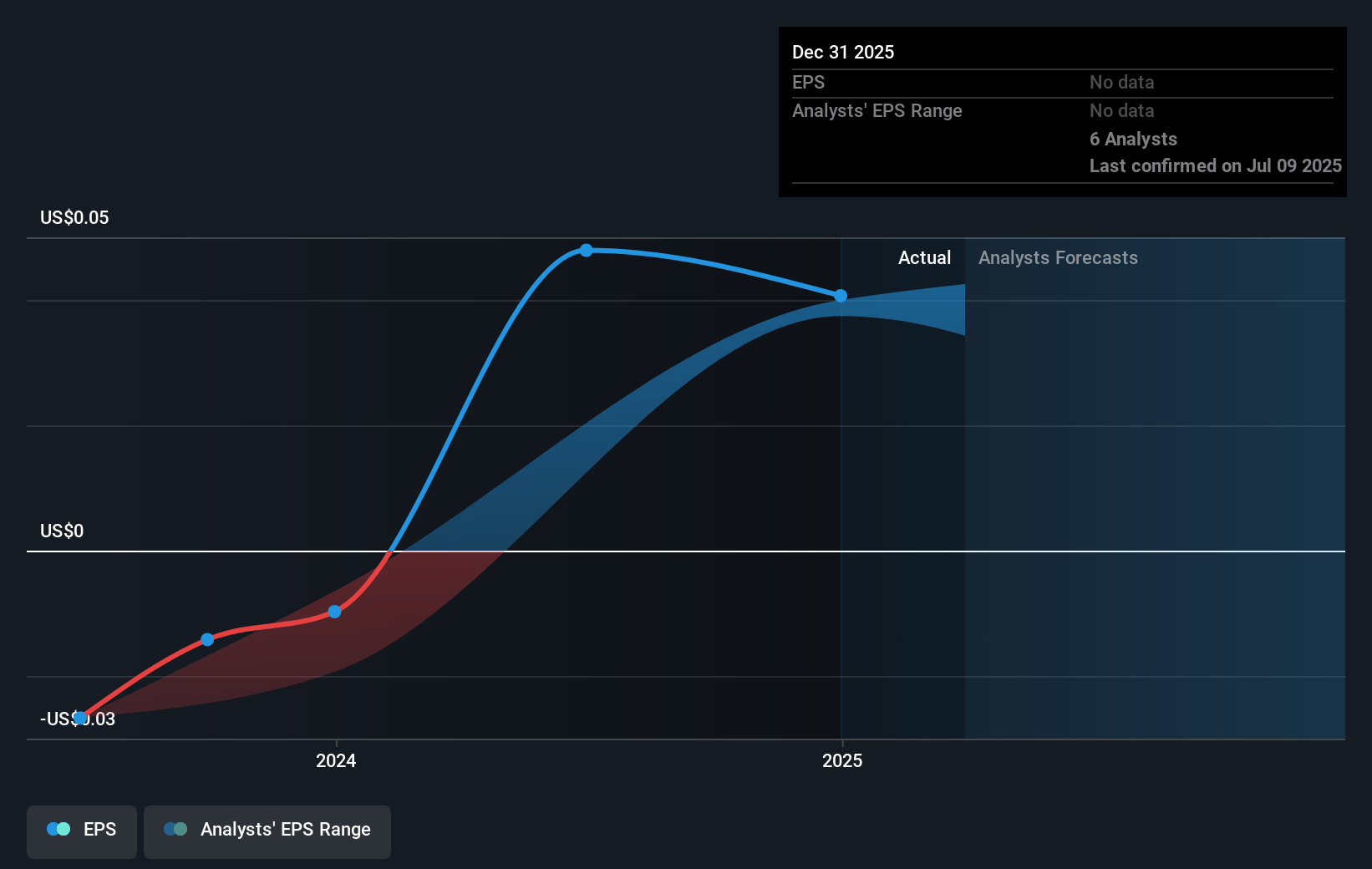

- Analysts expect earnings to reach $179.3 million (and earnings per share of $0.05) by about April 2028, up from $136.6 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $211 million in earnings, and the most bearish expecting $132.9 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 25.8x on those 2028 earnings, up from 17.9x today. This future PE is greater than the current PE for the NO Machinery industry at 17.0x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.28%, as per the Simply Wall St company report.

AutoStore Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Macroeconomic headwinds, high interest rates, and slowing e-commerce growth in 2024 led to market contraction, which could continue to impact AutoStore’s revenue growth if these conditions persist.

- Extended customer decision-making cycles in an unpredictable market environment may delay revenue recognition and challenge consistent earnings.

- Despite a strong backlog, the timing of project delivery remains unpredictable, leading to potential revenue fluctuations and lumpy cash flow.

- Uncertainties in the U.S. market, compounded by potential tariff announcements, could negatively impact revenue and margins, especially since North America accounted for 25% of revenue.

- A shift toward OpEx-based deals may increase recurring revenue but could reduce short-term revenue recognition, impacting cash flow and financial stability if not managed correctly.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of NOK11.608 for AutoStore Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of NOK14.21, and the most bearish reporting a price target of just NOK6.58.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $736.6 million, earnings will come to $179.3 million, and it would be trading on a PE ratio of 25.8x, assuming you use a discount rate of 7.3%.

- Given the current share price of NOK7.57, the analyst price target of NOK11.61 is 34.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.