Key Takeaways

- Expansion in high-demand logistics areas and strong retail lease spreads are expected to boost future revenue and improve earnings.

- Strong balance sheet with low leverage and high credit rating allows favorable refinancing, supporting growth and improved net margins.

- Economic uncertainties and market volatility could hinder revenue growth and margins, with potential impacts from land scarcity, consumer spending, and partnership risks.

Catalysts

About Fibra Danhos- We are a Mexican trust constituted, primarily, to develop, own, lease, operate, and acquire iconic and premier-quality real estate assets in Mexico.

- Expansion of the industrial real estate portfolio, with new projects like Cuautitlán II, Palomas, and a third JV project, is expected to increase future revenue as they are located in high-demand logistics areas.

- Improved occupancy rates and successful renewals with key clients in the office sector, including 50,000 square meters recently renegotiated, should stabilize and potentially increase rental income, positively impacting net margins.

- Retail properties are showing strong demand with lease spreads above inflation, especially over a 10% increase, which is expected to boost revenue and improve earnings going forward.

- The joint venture with a nonrelated partner and potential further deals in industrial projects could enhance earnings through shared resources and management fees while minimizing risks.

- A strong balance sheet with 12.2% leverage and a AAA Fitch rating enables the company to secure better refinancing terms and invest further in growth projects, thereby having a positive effect on future net margins and earnings.

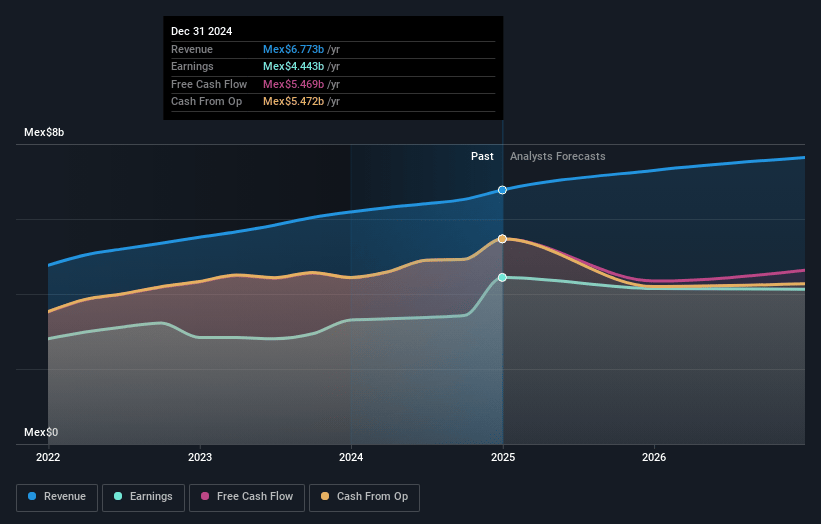

Fibra Danhos Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Fibra Danhos's revenue will grow by 7.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 64.6% today to 57.2% in 3 years time.

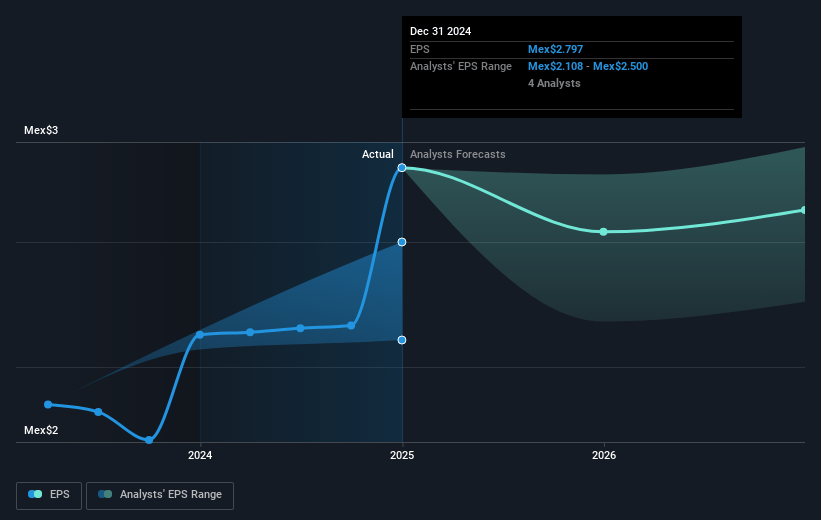

- Analysts expect earnings to reach MX$5.0 billion (and earnings per share of MX$2.95) by about July 2028, up from MX$4.5 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting MX$5.6 billion in earnings, and the most bearish expecting MX$4.1 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.7x on those 2028 earnings, up from 8.8x today. This future PE is greater than the current PE for the MX REITs industry at 8.0x.

- Analysts expect the number of shares outstanding to grow by 1.16% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.17%, as per the Simply Wall St company report.

Fibra Danhos Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Potential land scarcity and infrastructure challenges could impact future industrial development projects, affecting revenue growth opportunities.

- Economic uncertainties, both globally and within Mexico, might lead to reduced consumer spending, impacting sales in Fibra Danhos' retail properties and thus affecting revenue.

- The ability to secure favorable leasing terms in a potentially volatile market might impact margins, particularly if new lease agreements do not match previous contract rates.

- Dependence on industrial portfolio expansion for growth carries risks; any downturn in the industrial real estate market could pressure earnings and margins.

- The use of joint ventures introduces partnership risks, where misaligned goals or execution issues could impact the financial outcomes of industrial projects, affecting revenues and returns.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of MX$25.725 for Fibra Danhos based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of MX$30.6, and the most bearish reporting a price target of just MX$22.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be MX$8.7 billion, earnings will come to MX$5.0 billion, and it would be trading on a PE ratio of 12.7x, assuming you use a discount rate of 14.2%.

- Given the current share price of MX$24.75, the analyst price target of MX$25.72 is 3.8% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.