Key Takeaways

- Upgrading manufacturing and using digital tools will enhance efficiency and product quality, boosting revenue and net margins via cost savings.

- Expanding e-commerce and strategic cost reductions are expected to increase revenue, improve free cash flow, and enhance profitability and operating profit.

- Economic challenges in Argentina and increased competition are straining Grupo Rotoplas' profitability, while new investments elevate costs and financial risks.

Catalysts

About Grupo Rotoplas. de- Manufactures, purchases, sells, and installs plastic containers and accessories for water storage, conduction, and improvement solutions in Mexico, Argentina, the United States and internationally.

- The modernization of manufacturing processes in Mexico, specifically the upgrade to the Tinaco production, is expected to lead to increased operational efficiency and improved product quality, potentially boosting revenue and improving net margins through cost savings.

- The migration to Google Cloud and the deployment of advanced digital analytics and AI tools are anticipated to enhance operational efficiency and support business growth without proportionate increases in resources, likely improving earnings and net margins by reducing costs.

- The launch and expansion of B2B and B2B2C e-commerce platforms in Mexico presents a new channel for revenue growth by reaching more distributors and end-users, potentially increasing overall revenue and improving earnings.

- Strategic cost reduction measures, including a reduction in workforce and the focus on optimizing expenses and investments, are expected to enhance free cash flow and improve operating profit, positively impacting net margins and earnings.

- The continued growth of the bebbia service and other services, which are gaining traction despite initial negative EBITDA margins, is expected to contribute increasingly to total revenue and is positioned to improve profitability over time as efficiency and scale are achieved.

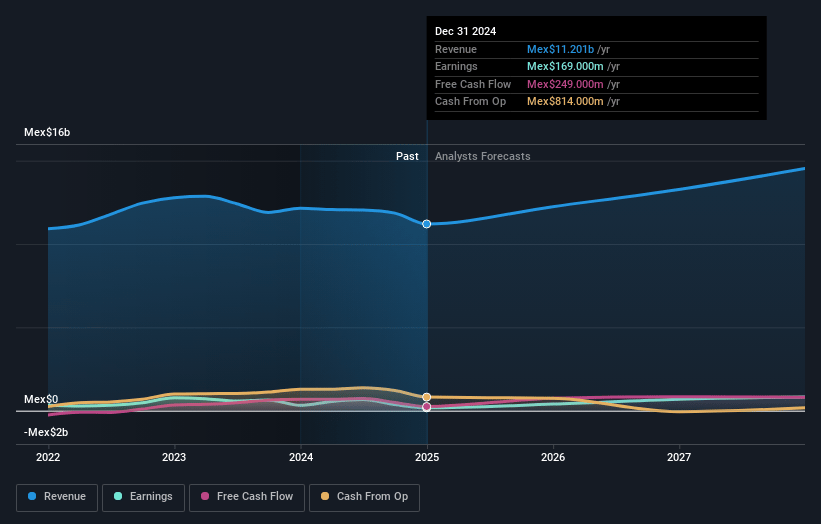

Grupo Rotoplas. de Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Grupo Rotoplas. de's revenue will grow by 8.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.5% today to 5.0% in 3 years time.

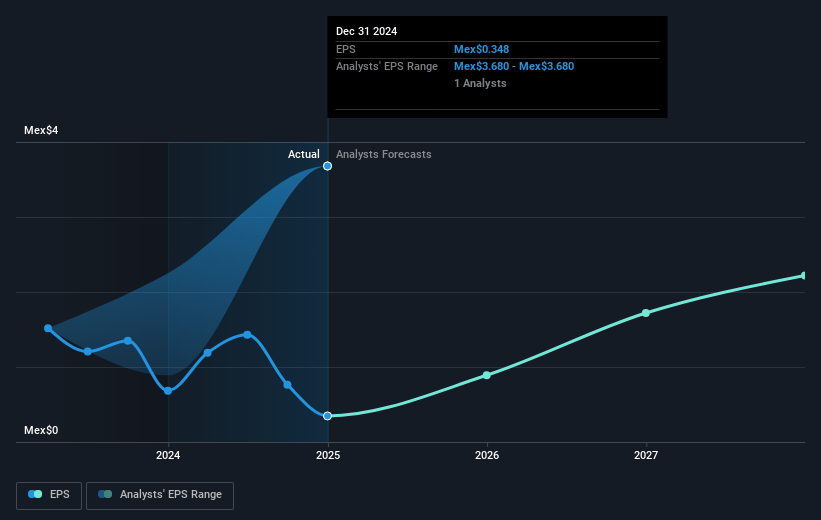

- Analysts expect earnings to reach MX$713.0 million (and earnings per share of MX$1.8) by about April 2028, up from MX$169.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting MX$874 million in earnings, and the most bearish expecting MX$552 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 39.1x on those 2028 earnings, up from 29.7x today. This future PE is lower than the current PE for the MX Building industry at 165.4x.

- Analysts expect the number of shares outstanding to decline by 0.11% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 18.65%, as per the Simply Wall St company report.

Grupo Rotoplas. de Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The ongoing economic recession in Argentina has severely impacted Grupo Rotoplas' sales and profitability, leading to a 46% decline in net income for the year, which poses continued risks to revenue and earnings if the economy does not recover as expected.

- The company's significant capital and organizational investments into new projects have increased expenses, which, along with the need to manage high operational costs, may pressure net margins until these initiatives begin yielding returns.

- The restructuring to reduce costs, including a 4% reduction in workforce, indicates financial strain and highlights potential risks to operations and employee morale, which could ultimately impact efficiency and profitability.

- Grupo Rotoplas is facing increased competition and added pressures on EBITDA margins in its Services division, which remains unprofitable and could continue to negatively affect overall earnings if not successfully managed.

- Uncertainty in the construction sector in Argentina, combined with higher inventories and receivables tying up cash, could lead to financial instability and increase the risk of write-offs affecting cash flow and working capital.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of MX$34.725 for Grupo Rotoplas. de based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of MX$44.0, and the most bearish reporting a price target of just MX$24.8.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be MX$14.3 billion, earnings will come to MX$713.0 million, and it would be trading on a PE ratio of 39.1x, assuming you use a discount rate of 18.6%.

- Given the current share price of MX$10.38, the analyst price target of MX$34.72 is 70.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.