Key Takeaways

- Integration of UGB and focus on operational upgrades promise growth, though challenges and initial costs could strain capital and margins.

- Efforts in digitization and ESG are key for future growth, but high competition and investment costs might impact short-term profitability.

- Burgan Bank's strategic acquisitions, digital enhancements, and strong asset quality support growth, efficiency, and revenue resilience through complementary models and robust market presence.

Catalysts

About Burgan Bank K.P.S.C- Provides various banking products and services in Kuwait and internationally.

- The acquisition of UGB and its complimentary business model with Kamco is seen as a growth opportunity in high-growth sectors such as Islamic financing and investments. This could lead to significant cross-selling and upselling opportunities, potentially driving revenue growth, but there is uncertainty about the integration and realization of synergies and the capital impact.

- The major investment in the overhaul and upgrade of Burgan’s core banking system with TCS is aimed at enhancing operational efficiencies and launching new products faster. However, the implementation challenges and costs may pressure net margins initially before any long-term efficiency gains are realized.

- The digitization efforts, including the Turkish digital platform ON by BBT, are expected to continue driving customer acquisition, deposit growth, and loan volumes. Yet, the market competition and cost of maintaining cutting-edge digital infrastructure may compress net margins and affect overall earnings.

- The focus on diversifying corporate income through enhanced fee-based revenue streams and cross-selling may increase non-interest income, but it stands against headwinds of higher operating costs, especially staff expenses and IT investment, impacting net margins.

- Sustainability initiatives and ESG commitments, although improving governance and potentially opening up new avenues for sustainable financing, will likely require upfront investments that could weigh on short-term profitability and compress net margins before delivering potential longer-term earnings benefits.

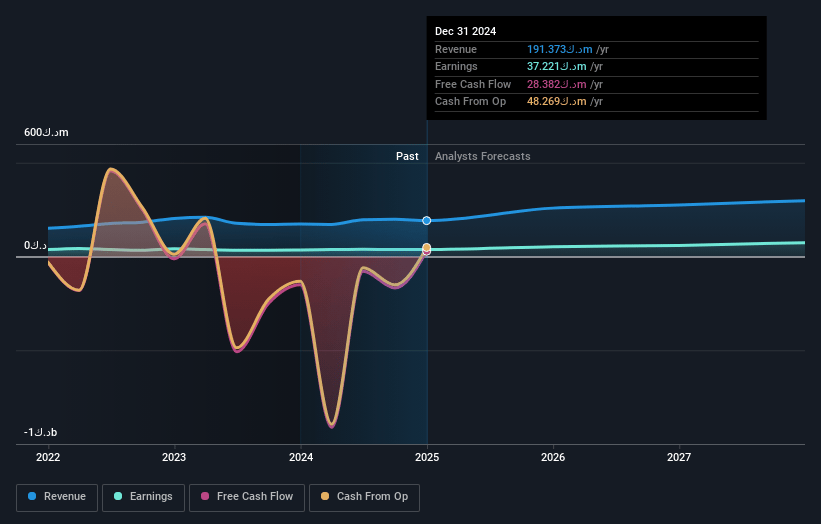

Burgan Bank K.P.S.C Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Burgan Bank K.P.S.C's revenue will grow by 15.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 19.4% today to 24.8% in 3 years time.

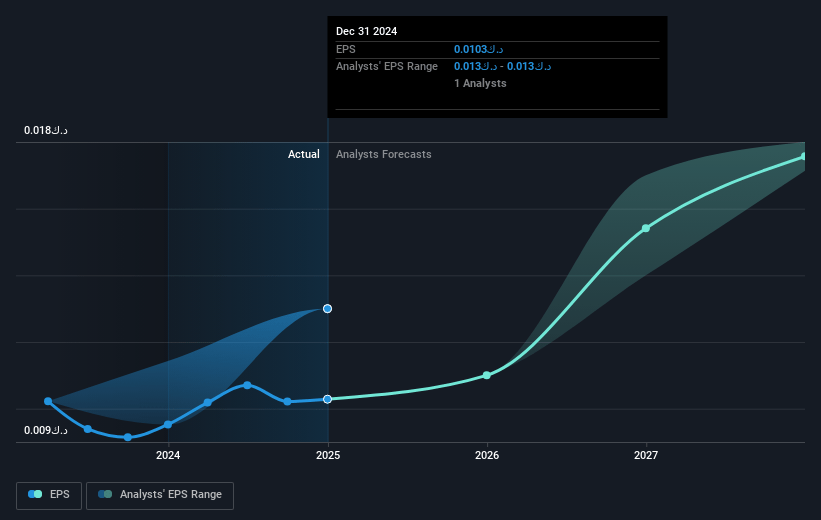

- Analysts expect earnings to reach KWD 74.0 million (and earnings per share of KWD 0.02) by about March 2028, up from KWD 37.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.2x on those 2028 earnings, down from 23.3x today. This future PE is lower than the current PE for the KW Banks industry at 20.6x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 22.12%, as per the Simply Wall St company report.

Burgan Bank K.P.S.C Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Burgan Bank's strategic acquisition of UGB positions it for growth in Islamic financing and investment sectors, potentially increasing revenue through complementary business models and cross-selling with Kamco.

- Enhanced digitalization efforts, like the overhaul of the core banking system by TCS, could improve operational efficiency and customer experience, potentially boosting earnings and margins.

- Improved asset quality and low cost of credit indicate potential for sustained financial health, potentially enhancing net margins.

- The growth in asset base and strong liquidity position, with significant buffers above regulatory requirements, supports continued expansion and revenue generation.

- High customer satisfaction scores and increased deposit and loan volumes suggest a strong market presence, likely contributing to revenue resilience.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of KWD0.204 for Burgan Bank K.P.S.C based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be KWD298.0 million, earnings will come to KWD74.0 million, and it would be trading on a PE ratio of 18.2x, assuming you use a discount rate of 22.1%.

- Given the current share price of KWD0.24, the analyst price target of KWD0.2 is 17.5% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.