Key Takeaways

- AI-driven efficiencies and international expansion are expected to boost revenue and competitive advantages through improved margins and personalized customer retention.

- Strategic partnerships and advanced technologies promise significant earnings growth in telecommunications and cloud solutions.

- Heavy reliance on ecosystem and technological partnerships poses risks to profitability and financial stability amidst uncertain mobile segment profitability and underlying financial pressures.

Catalysts

About Rakuten Group- Provides services in e-commerce, fintech, digital content, and communications to various users in Japan and internationally.

- Rakuten Mobile is achieving rapid growth in subscribers, expected to drive the growth of the entire Rakuten ecosystem, contributing significantly to future revenue increases through cross-selling of Rakuten services to mobile users.

- AI-driven operational efficiencies, targeting a 31% reduction in customer support costs, are anticipated to improve net margins by boosting profitability across Rakuten's operational segments.

- Expansion into international markets and the collection of rich data from over a billion members worldwide are expected to enhance revenue streams and provide competitive advantages in personalization and customer retention.

- The adoption of advanced telecommunication technologies and strategic partnerships are set to improve Rakuten Mobile's network quality, expected to increase subscriber ARPU (Average Revenue Per User) and drive future revenue growth.

- Rakuten Symphony's strategic partnerships and technology offerings in private cloud solutions could boost earnings substantially as more global companies look to adopt efficient and innovative telecommunications technology, enhancing Rakuten Group's earnings growth.

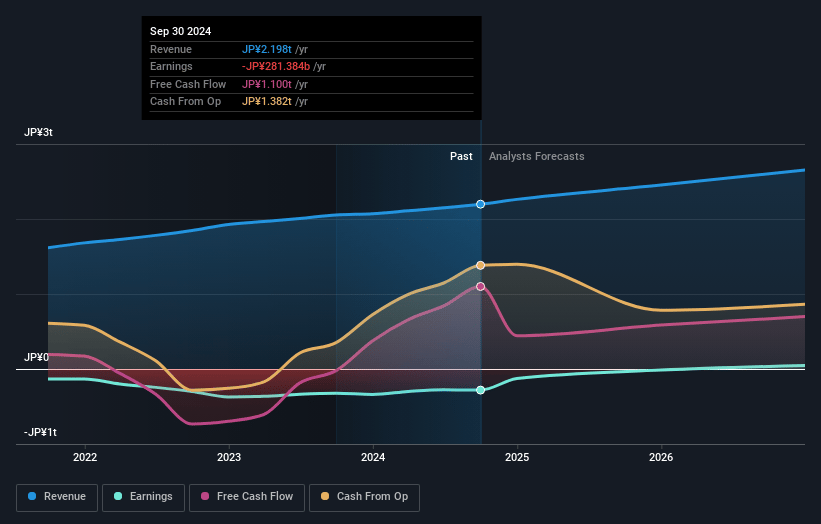

Rakuten Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Rakuten Group's revenue will grow by 8.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from -7.1% today to 3.3% in 3 years time.

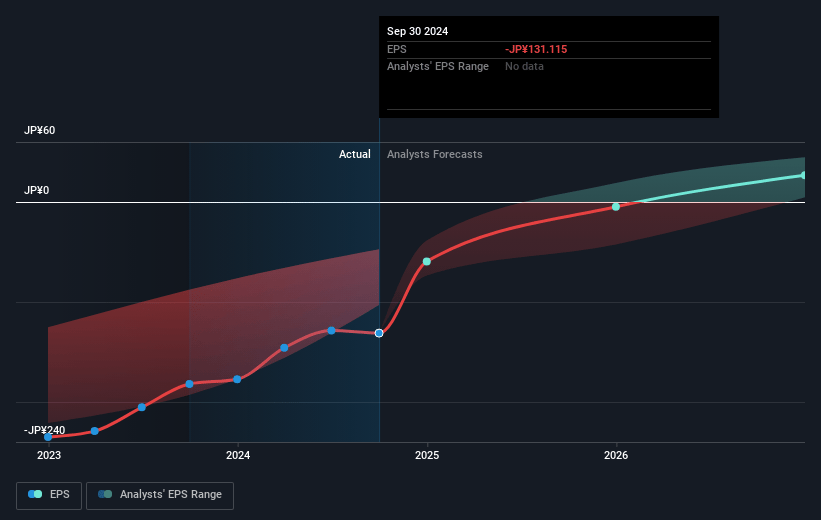

- Analysts expect earnings to reach ¥94.8 billion (and earnings per share of ¥44.0) by about May 2028, up from ¥-162.4 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ¥151.1 billion in earnings, and the most bearish expecting ¥49.5 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 30.8x on those 2028 earnings, up from -11.1x today. This future PE is greater than the current PE for the JP Multiline Retail industry at 18.4x.

- Analysts expect the number of shares outstanding to grow by 0.52% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.91%, as per the Simply Wall St company report.

Rakuten Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The Rakuten Mobile segment's profitability is still uncertain, with the expectation of monthly EBITDA profitability by 2025, which could impact overall earnings if this target is not met.

- The company relies heavily on its ecosystem, and any decline in user interaction or subscription numbers could negatively affect revenues and margins across the group's services.

- Financial flexibility is currently maintained through self-funding and sales and leaseback arrangements, but any challenges in maintaining this could impact the net debt levels and financial stability.

- Recent refinances and financial strategies, like strategic capital alliances and sales of assets, indicate potential underlying financial pressures, which could affect the company’s ability to sustain long-term profitability.

- The strategic reliance on technological partnerships and AI integration poses execution risk; failure to realize anticipated efficiencies could affect operational costs and net margins negatively.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ¥977.769 for Rakuten Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥1200.0, and the most bearish reporting a price target of just ¥510.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ¥2887.6 billion, earnings will come to ¥94.8 billion, and it would be trading on a PE ratio of 30.8x, assuming you use a discount rate of 10.9%.

- Given the current share price of ¥839.5, the analyst price target of ¥977.77 is 14.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.