Key Takeaways

- Leadership transition to Julie Kim in 2026 aligns with potential drug launches, enhancing future revenue and investor sentiment.

- Growth in Launch Products and late-stage pipeline developments underscore strong sales potential and earnings boost.

- Transition management risks, accounting issues, competitive pressures, and potential underinvestment in R&D could destabilize revenues and impact Takeda's future growth trajectory.

Catalysts

About Takeda Pharmaceutical- Engages in the research, development, manufacture, marketing, and out-licensing of pharmaceutical products in Japan and internationally.

- Takeda's CEO succession plan, including the upcoming leadership transition to Julie Kim in 2026, aligns with potential drug launches starting in the second half of 2026, which could drive future revenue growth and improve investor sentiment.

- The momentum in Takeda's Growth and Launch Products, which showed a 14.6% growth at constant exchange rates (CER) year-to-date, suggests strong future sales that may continue to offset other revenue declines, thus supporting overall revenue growth.

- The late-stage pipeline with three significant Phase III data readouts expected in 2025 is a major focus, potentially leading to new product launches that could substantially boost future earnings.

- Takeda's operational efficiency program has already delivered margin improvements. Continued implementation is expected to yield further operational savings, helping to enhance net margins.

- The share buyback program of up to ¥100 billion, reflecting confidence in long-term cash flow generation, may support earnings per share (EPS) growth and shareholder value.

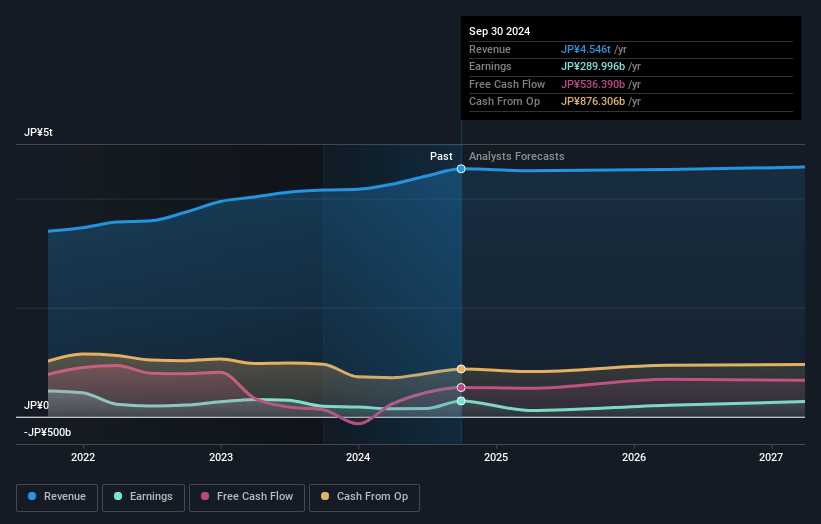

Takeda Pharmaceutical Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Takeda Pharmaceutical's revenue will grow by 1.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.5% today to 6.5% in 3 years time.

- Analysts expect earnings to reach ¥306.2 billion (and earnings per share of ¥196.92) by about March 2028, up from ¥208.1 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ¥395.8 billion in earnings, and the most bearish expecting ¥97.0 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 30.0x on those 2028 earnings, down from 34.4x today. This future PE is greater than the current PE for the JP Pharmaceuticals industry at 16.2x.

- Analysts expect the number of shares outstanding to grow by 1.03% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 4.59%, as per the Simply Wall St company report.

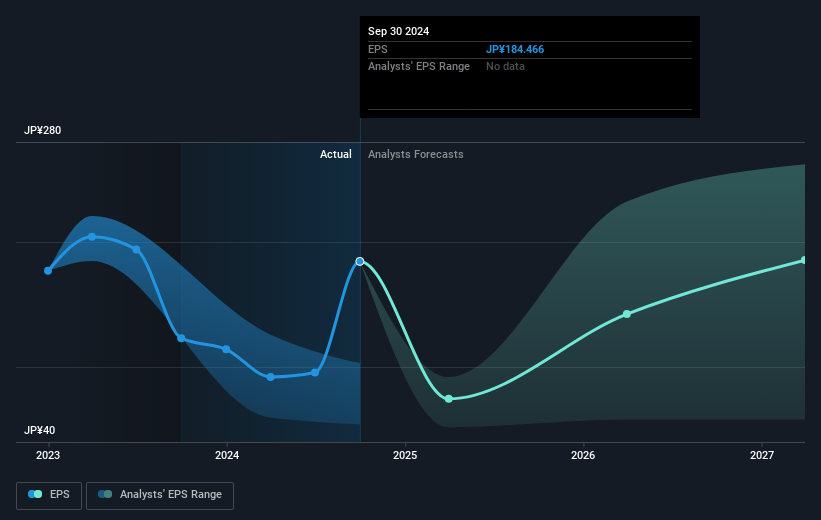

Takeda Pharmaceutical Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The impending management change, with Christophe Weber retiring and Julie Kim succeeding him, introduces execution risk during the transition period, which could impact strategic continuity and potentially affect revenues and operational stability.

- Accounting issues, such as the negative impact on cost of goods sold (COGS) from the yen-denominated inventory valuation adjustment, might affect net margins and future earnings unpredictability.

- The potential impact of the U.S. Inflation Reduction Act (IRA), which could include Entyvio in Medicare pricing negotiations by 2028, could affect the net pricing landscape, impacting future revenues negatively.

- Increased activity in the development of Entyvio biosimilars, particularly from players like Alvotech and Teva, poses a competitive threat and introduces uncertainty regarding the timing of biosimilar entry, which could disrupt revenue streams sooner than anticipated.

- The transition of programs and the move of R&D trial costs to other expenses, coupled with the slower-than-expected R&D spending, could signal underinvestment in future pipeline development, impacting long-term revenue growth if innovation lags.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ¥4930.833 for Takeda Pharmaceutical based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥5800.0, and the most bearish reporting a price target of just ¥4200.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ¥4724.5 billion, earnings will come to ¥306.2 billion, and it would be trading on a PE ratio of 30.0x, assuming you use a discount rate of 4.6%.

- Given the current share price of ¥4538.0, the analyst price target of ¥4930.83 is 8.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.