Key Takeaways

- Growth in high-performance products and effective cost control are expected to significantly boost operating profit and margins.

- Emphasis on sustainable innovation and strategic housing market operations aims to increase future earnings and investor interest.

- Weaker market conditions and declines in key sectors pose risks to revenue and profit margins, affecting sales forecasts and overall profitability.

Catalysts

About Sekisui Chemical- Engages in the housing, urban infrastructure and environmental products, high performance plastics, and medical businesses.

- Sekisui Chemical expects significant growth in its high-performance products (HPP) segment driven by advanced semiconductors and improved selling prices, which is likely to positively impact revenue and operating profit.

- The company is anticipating an operating profit increase due to effective cost control measures, including fixed cost reductions, and benefit from foreign exchange, which should enhance net margins.

- Sekisui's reinvestment plan for mass production of perovskite solar cells indicates a shift towards sustainable growth and innovation, promising future earnings potential.

- With an emphasis on high-margin orders in urban housing markets and a robust sales strategy in the housing business, Sekisui anticipates growth in sales value and operating profit, which could improve overall earnings.

- The planned dividend increase underscores confidence in cash flow and profitability, potentially leading to higher earnings per share and attracting investor interest.

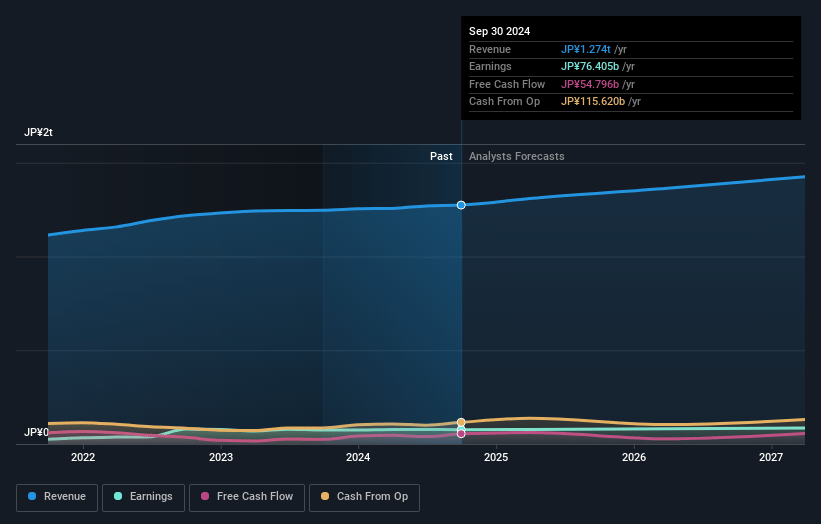

Sekisui Chemical Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Sekisui Chemical's revenue will grow by 4.5% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 6.8% today to 6.2% in 3 years time.

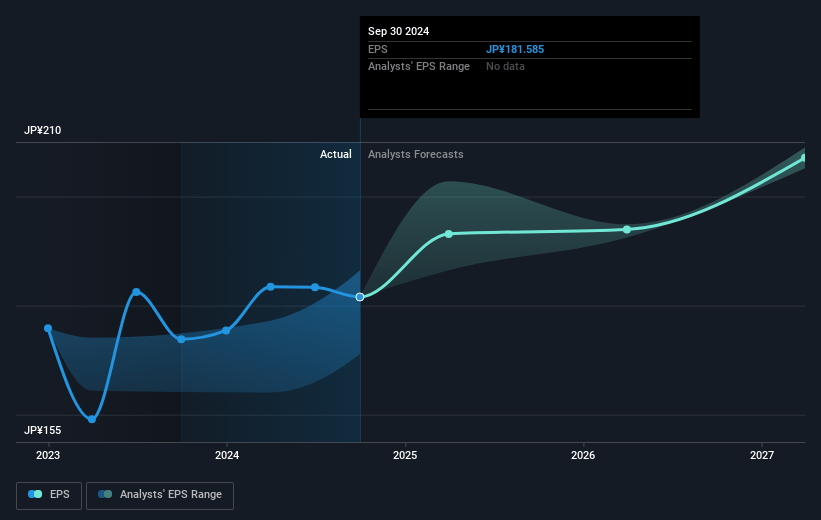

- Analysts expect earnings to reach ¥91.8 billion (and earnings per share of ¥221.24) by about March 2028, up from ¥88.0 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 13.9x on those 2028 earnings, up from 12.5x today. This future PE is greater than the current PE for the JP Industrials industry at 12.8x.

- Analysts expect the number of shares outstanding to decline by 0.91% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.39%, as per the Simply Wall St company report.

Sekisui Chemical Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Weaker-than-expected market conditions, particularly in the sluggish housing and nonresidential markets in Japan, present a risk to achieving projected sales growth, potentially impacting revenue and net margins negatively.

- Decline in demand for diagnostics in key overseas markets such as China and delays in sales expansion in Europe and North America could adversely affect revenue and lead to a potential revision in earnings forecasts for the medical business.

- Sluggish auto production volumes and weaker-than-anticipated smartphone shipments in Q4 pose threats to revenue projections, particularly affecting segments reliant on these industries.

- Exposure to currency fluctuations and a weaker yen against the dollar can impact profit margins and lead to variability in reported earnings if not effectively hedged.

- Struggles in the mobility field, especially due to China's market conditions affecting demand for head-up displays, could lead to underperformance in the segment's revenue, impacting overall profitability predictions.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ¥2687.5 for Sekisui Chemical based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥3280.0, and the most bearish reporting a price target of just ¥2370.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ¥1469.5 billion, earnings will come to ¥91.8 billion, and it would be trading on a PE ratio of 13.9x, assuming you use a discount rate of 5.4%.

- Given the current share price of ¥2644.5, the analyst price target of ¥2687.5 is 1.6% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.