Key Takeaways

- High energy consumption from the carbon capture project in Denmark may increase costs and negatively impact net margins if not offset by revenue growth.

- Potential revenue growth from new demand in rebuilding projects and increased capacity is speculative and dependent on geopolitical and economic stability.

- Strategic investments in CO2 reduction and sustainability, along with targeted M&A and innovation, position Cementir for long-term growth amid evolving market and regulatory dynamics.

Catalysts

About Cementir Holding- Manufactures and distributes grey and white cement, ready-mix concrete, aggregates, and concrete products in Nordic and Baltic, Belgium, North America, Turkiye, Egypt, and Asia Pacific.

- Cementir Holding is implementing a significant carbon capture and storage (CCS) project in Denmark, expected to operationalize by 2030. This initiative could increase operational costs due to high energy consumption, potentially impacting net margins negatively if cost increases aren't matched by revenue growth.

- There is potential for increased demand from reconstruction efforts in Syria, Gaza, and Ukraine, which could positively affect revenue growth. However, this is speculative and contingent on geopolitical developments, potentially impacting revenue forecasts if conditions don't materialize.

- The company's forecasted increase in EBITDA is partly dependent on currency stability in Türkiye and Egypt, areas comprising significant portions of Cementir's revenue. Continued currency volatility could negatively affect reported earnings.

- The new CO2 emission tax in Denmark is expected to be passed on to customers, allowing Cementir to maintain its revenue levels. However, the tax could still squeeze net margins if the price increases do not fully offset the tax cost due to market limitations.

- Cementir's plan to achieve significant revenue growth through increased capacity in Egypt and recovery in other regions could be hampered by unforeseen economic conditions or market-entry barriers, potentially impacting revenue and earnings growth if these expansions do not proceed as planned.

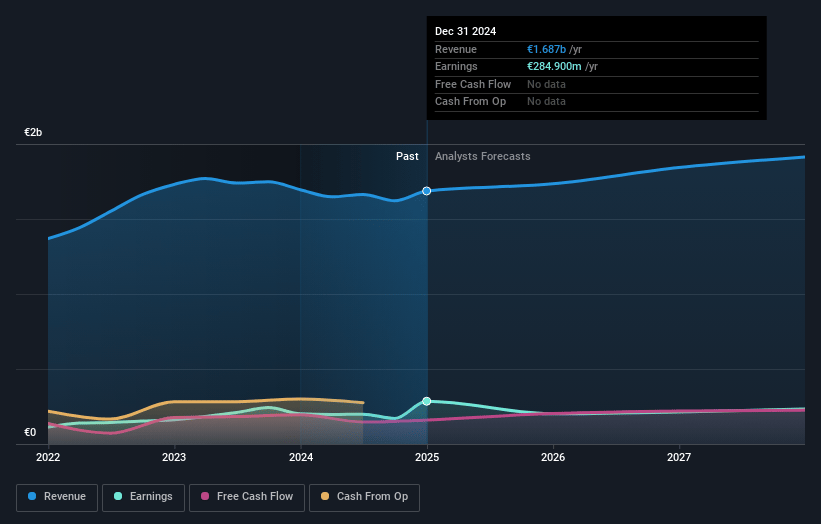

Cementir Holding Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Cementir Holding's revenue will grow by 4.3% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 16.9% today to 12.2% in 3 years time.

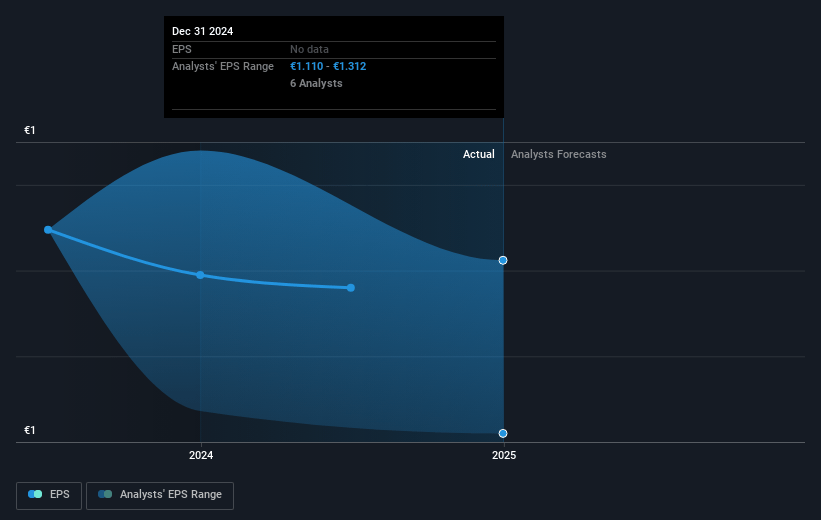

- Analysts expect earnings to reach €234.0 million (and earnings per share of €1.48) by about March 2028, down from €284.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.3x on those 2028 earnings, up from 7.2x today. This future PE is greater than the current PE for the GB Basic Materials industry at 8.2x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.07%, as per the Simply Wall St company report.

Cementir Holding Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Cementir Holding's strategic investments in aggressive CO2 reduction and sustainability projects, such as the large-scale CCS project in Denmark, could enhance the company’s market position and improve long-term revenue and margins by attracting environmentally conscious customers and potentially benefiting from regulatory incentives.

- The company's plan to grow revenue by 6-7% compounded annually through increased capacity in Egypt, recovery in Denmark and Asia Pacific, and maintaining global white cement leadership could bolster earnings and counteract potential downturns in other regions.

- Cementir's healthy financial position with significant net cash and targeted M&A opportunities may provide a buffer against market volatility and create avenues for increased revenue and profitability through strategic acquisitions.

- The company's focus on innovation, low-carbon cement, and digitization, including successful projects like FUTURECEM and D-Carb, could lead to cost efficiencies and improved net margins.

- The potential for increased exports, particularly from Turkey to neighboring regions like Syria and Iraq for reconstruction efforts, could offset domestic challenges and lead to stronger revenue performance.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €13.842 for Cementir Holding based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €1.9 billion, earnings will come to €234.0 million, and it would be trading on a PE ratio of 11.3x, assuming you use a discount rate of 7.1%.

- Given the current share price of €13.18, the analyst price target of €13.84 is 4.8% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.