Key Takeaways

- Integration and optimization, including supply chain and procurement efficiencies, are expected to boost efficiency, revenue growth, and EBITDA margins, while reducing costs.

- New contracts and co-packing expansion aim to enhance revenues and profitability, contributing to stable net margins and improved cash flow.

- Exposure to macroeconomic volatility in key markets, combined with integration and execution risks, may impact profitability and growth.

Catalysts

About Newlat Food- Operates in the agri-food sector in Italy, Germany, the United Kingdom, and internationally.

- The integration of Princes into the Newlat Group presents opportunities for operational synergy. This includes aligning fiscal year ends, consolidating procurement processes, and streamlining business units, which is expected to improve efficiency and facilitate revenue growth.

- New multiyear contracts in drinks, foods, and oils are expected to drive higher sales volumes and revenues in the upcoming months. Notably, the Capri Sun contract adds a stable source of revenue to the group's portfolio.

- Expansion of the co-packing business is set to improve the revenue mix of the Drinks unit by introducing longer-term contractual revenue streams, potentially enhancing overall profitability and contributing to more stable net margins.

- The integration and optimization of the supply chain, combined with procurement efficiencies, are expected to increase EBITDA margins, particularly as renegotiated energy contracts take effect, reducing costs.

- The ongoing cross-selling initiatives and geographic expansion efforts are positioned to increase market share in new and existing markets, likely buoying top-line growth and continuing to improve cash flow generation through enhanced operational performance.

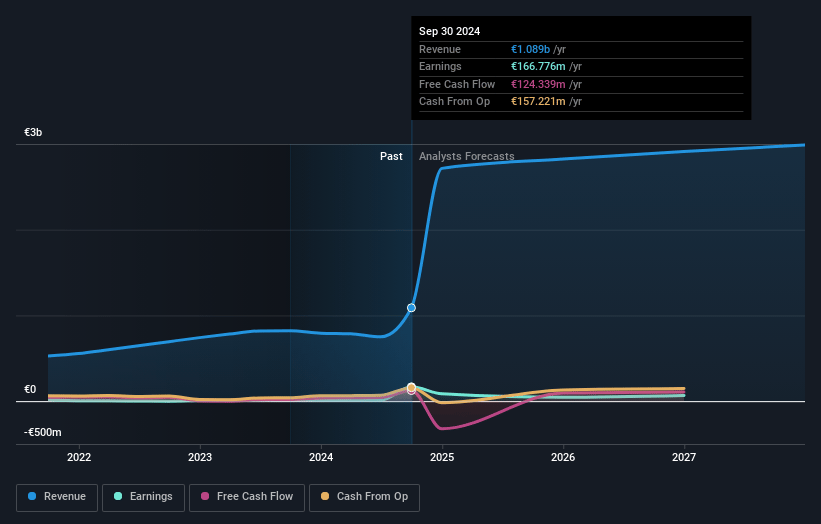

Newlat Food Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Newlat Food's revenue will grow by 39.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 15.3% today to 1.3% in 3 years time.

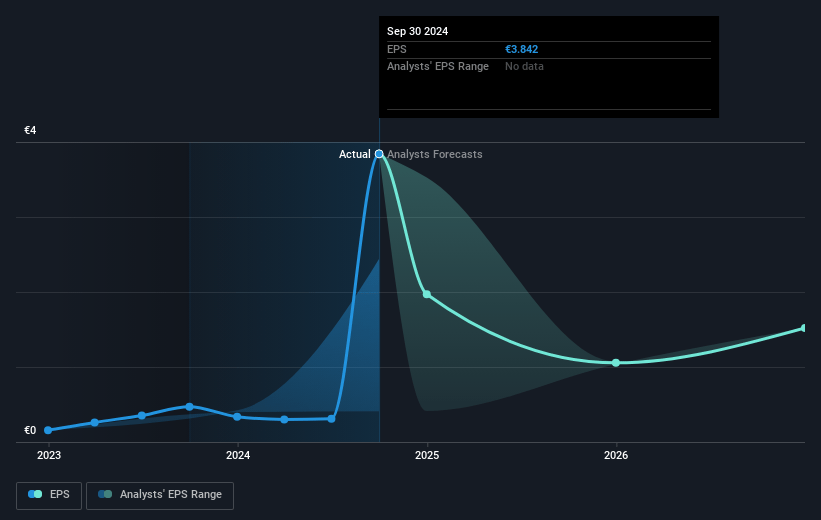

- Analysts expect earnings to reach €37.5 million (and earnings per share of €0.85) by about March 2028, down from €166.8 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 27.0x on those 2028 earnings, up from 3.1x today. This future PE is greater than the current PE for the IT Food industry at 11.8x.

- Analysts expect the number of shares outstanding to grow by 3.81% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.17%, as per the Simply Wall St company report.

Newlat Food Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Ongoing integration risks with Princes could potentially affect operational synergies and efficiencies, which may impact profitability and net margins.

- Energy and raw material cost volatility, as evident from the impact of fixed energy contracts and raw materials on Princes' margins, could affect EBITDA performance if not managed effectively.

- Deflationary pressures on selling prices across major geographies and categories could continue; while volume has shown resilience, persistent price pressures could impact overall revenue growth.

- Exposure to macroeconomic factors, especially in the U.K. market which accounts for over 50% of revenues, may present risks to revenue and earnings if the economic environment deteriorates unexpectedly.

- Execution risks related to new contracts and business expansion initiatives, such as the shift towards co-packing in the Drinks segment, may face challenges if not executed as planned, which could impact net margins and earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €15.05 for Newlat Food based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €3.0 billion, earnings will come to €37.5 million, and it would be trading on a PE ratio of 27.0x, assuming you use a discount rate of 11.2%.

- Given the current share price of €11.66, the analyst price target of €15.05 is 22.5% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives