Key Takeaways

- Strong performance in the Mavriq division, driven by organic growth and strategic acquisitions, supports promising future revenue trends.

- Effective cost management and market recovery in BPO and Tech Division enhance potential for higher net margins and expanded service demand.

- Despite strong organic growth, Moltiply faces challenges like weaker tech service performance, acquisition cost management issues, and risks from regulatory changes impacting margins.

Catalysts

About Moltiply Group- Through its subsidiaries, operates comparison platforms, and provides outsourcing services for credit processes, and asset and insurance claims management in Italy.

- The Moltiply Group is experiencing strong performance in the Mavriq division, with increased revenues driven by organic growth in insurance broking, e-commerce price comparison, and the recovery of mortgage volumes. This growth indicates a positive trend in revenue for the future.

- The consolidation of Pricewise and contributions from Switcho within the Mavriq division are expected to further enhance revenues and complement the organic growth already demonstrated.

- In the Moltiply BPO and Tech Division, organic growth surpassing expectations, particularly in the lease and claims business lines, indicates strong operational performance and potential for higher net margins due to effective cost management and higher-value contracts.

- A favorable outlook for the mortgage market, coupled with increasing interest in Moltiply's services, suggests potential revenue growth and improved earnings as the company capitalizes on market recovery and expanding service demand.

- The efficient handling of claims in the wake of recent meteorological events positions the company for potential profit margin growth as it captures market share in claims management, reflecting its capability to provide value-added services.

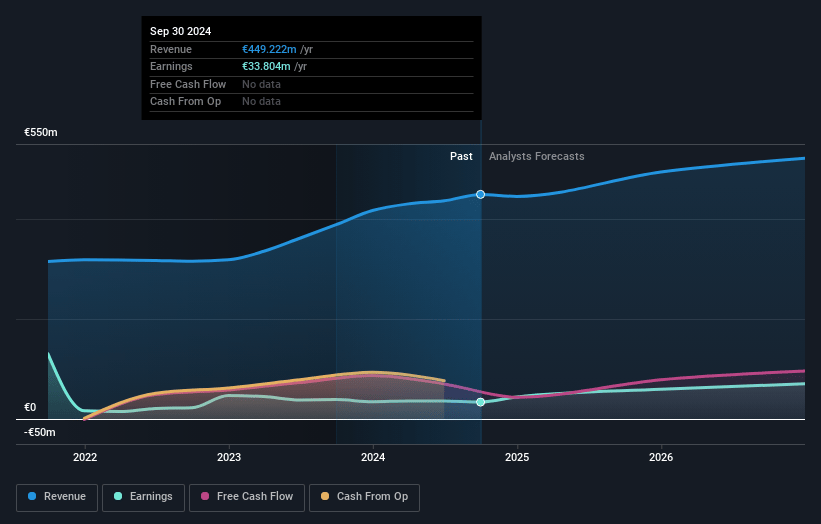

Moltiply Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Moltiply Group's revenue will grow by 7.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.5% today to 15.9% in 3 years time.

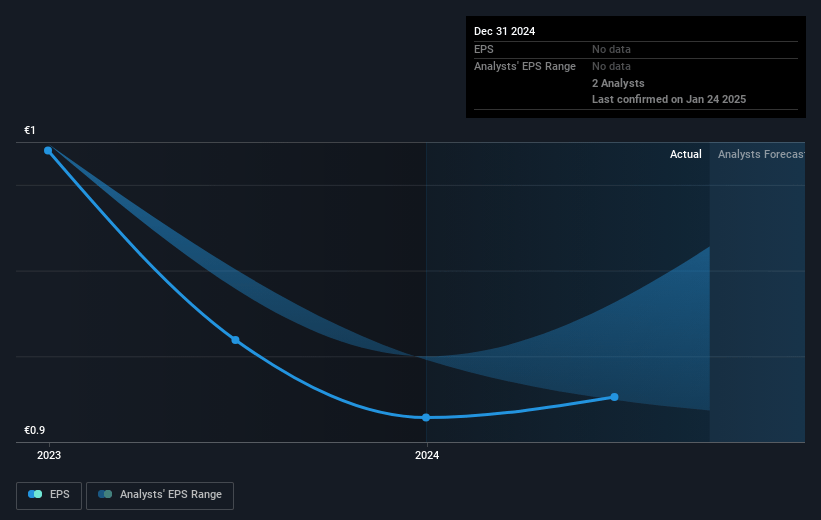

- Analysts expect earnings to reach €87.8 million (and earnings per share of €2.36) by about March 2028, up from €33.8 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 27.0x on those 2028 earnings, down from 38.6x today. This future PE is lower than the current PE for the GB Consumer Finance industry at 44.4x.

- Analysts expect the number of shares outstanding to grow by 0.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.97%, as per the Simply Wall St company report.

Moltiply Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The EBIT for the Mavriq division decreased by 7.2% in Q3 2024 due to purchase price amortization, which could indicate challenges in efficiently managing acquisition costs, potentially impacting net margins.

- The Moltiply real estate business line is experiencing contraction due to the reduction of support from Ecobonus incentive schemes, posing risks to revenue growth.

- There is uncertainty around the impact of a proposed web tax on digital businesses like Trovaprezzi, which could result in increased costs and pressure on net margins.

- Despite strong organic growth, the Moltiply business line is facing challenges, with some areas like technology services showing weaker performance, potentially affecting overall profit margins.

- The net financial position as of September 30, 2024, showed significant liabilities from acquisitions such as Pricewise, which could increase financial leverage and impact future earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €46.9 for Moltiply Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €552.7 million, earnings will come to €87.8 million, and it would be trading on a PE ratio of 27.0x, assuming you use a discount rate of 11.0%.

- Given the current share price of €34.9, the analyst price target of €46.9 is 25.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.