Key Takeaways

- Pipeline project completions and city gas distribution expansion could boost gas transmission volumes, revenue growth, and market share.

- Long-term LNG contracts and operational expansions could stabilize procurement costs and enhance profitability in petrochemicals.

- Exceptional income from SEFE Marketing inflates earnings, while decreased natural gas transmission and tariff issues could impact future revenue and profit stability.

Catalysts

About GAIL (India)- Operates as a natural gas processing and distribution company in India and internationally.

- GAIL's completion of key pipeline projects in the next financial years, such as the Mumbai-Nagpur-Jharsuguda and Srikakulam-Angul pipelines, is expected to increase gas transmission volumes, driving higher revenue growth.

- The company plans to significantly expand its city gas distribution (CGD) network by adding new CNG stations and DPNG connections over the next two years, which could lead to increased revenue and improved market share in the CGD segment, supporting overall earnings growth.

- Tying up additional long-term LNG contracts at favorable rates will likely stabilize GAIL's gas procurement costs, reducing margin volatility in gas trading and potentially enhancing net margins.

- The commencement of operations at new petrochemical facilities and securing propane for the PDHPP plant should lead to augmented polymer production, contributing to higher revenues and improved profitability in the petrochemical segment.

- GAIL's collaboration with international oil and gas companies, like YPF in Argentina, for exploration and production could secure future hydrocarbon and LNG supplies for India, implying longer-term revenue and earnings growth potential due to diversified and reliable sourcing.

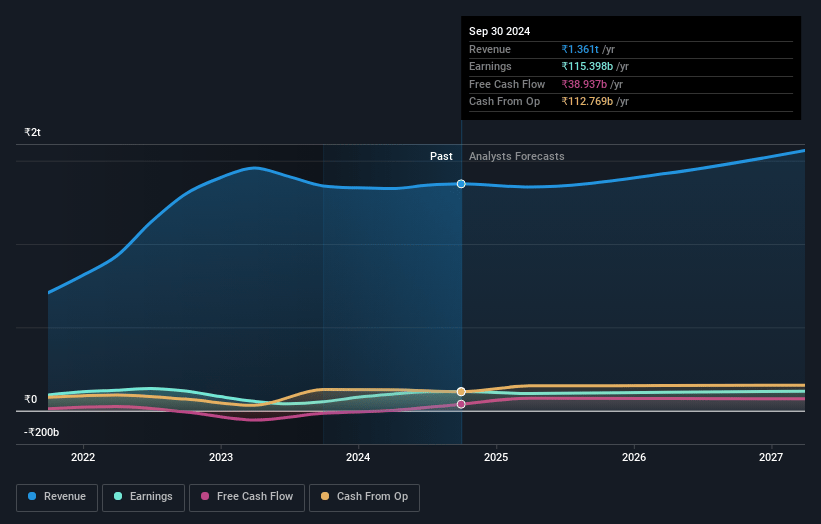

GAIL (India) Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming GAIL (India)'s revenue will grow by 4.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 9.0% today to 6.4% in 3 years time.

- Analysts expect earnings to reach ₹100.5 billion (and earnings per share of ₹15.63) by about May 2028, down from ₹124.3 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹146.7 billion in earnings, and the most bearish expecting ₹79.3 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 19.9x on those 2028 earnings, up from 10.0x today. This future PE is greater than the current PE for the GB Gas Utilities industry at 19.6x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.53%, as per the Simply Wall St company report.

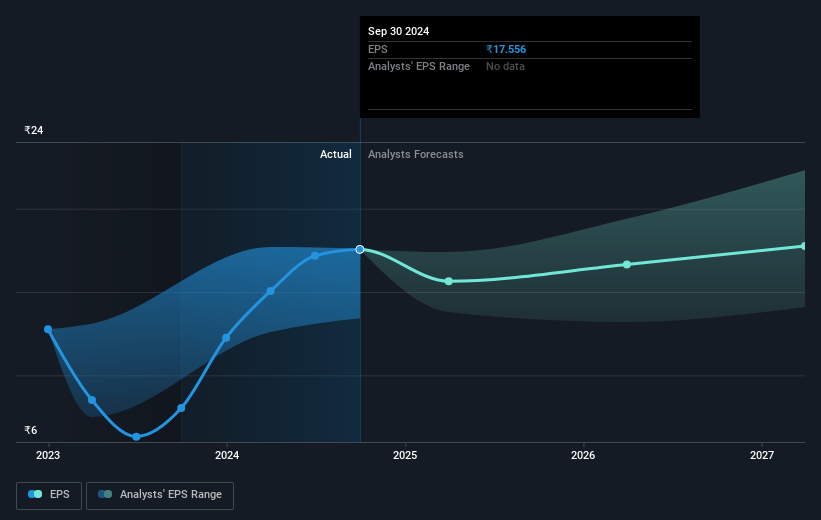

GAIL (India) Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The exceptional income received from SEFE Marketing and Trading Singapore as a settlement could create an overestimating effect on current earnings and may not be sustainable, potentially causing an overvaluation risk and impacting future revenue consistency.

- The decrease in natural gas transmission volume due to reduced offtake by the power segment and other shippers highlights a potential risk in demand stability, which could affect future revenue and profit margins.

- The cut in APM gas allocation for LPG production poses a risk to LPG production levels in the near term, potentially impacting revenue and net earnings from this segment.

- The noted volatility in trading EBIT due to factors such as falling crude prices and mismatches in contract terms introduces uncertainty and could impact earnings stability and profit margins if these trends continue.

- The ongoing tariff revisions and challenges in the regulatory environment, such as those related to the PNGRB's approval processes, could result in unexpected adjustments that may impact future revenue streams and net earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹213.871 for GAIL (India) based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹270.0, and the most bearish reporting a price target of just ₹155.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹1560.7 billion, earnings will come to ₹100.5 billion, and it would be trading on a PE ratio of 19.9x, assuming you use a discount rate of 12.5%.

- Given the current share price of ₹189.09, the analyst price target of ₹213.87 is 11.6% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.