Key Takeaways

- Delays in transformational projects affect current earnings, but expected to contribute to future revenue growth once resolved.

- Strategic initiatives on cost reduction and operational efficiency are set to improve margins and drive future profitability.

- Ongoing shipping delays and procedural issues in the U.K. are impacting short-term revenues and squeezing profitability through increased costs and deferred projects.

Catalysts

About TVS Supply Chain Solutions- Provides integrated supply chain solutions in India.

- Delays in large, transformational projects with key customers, particularly in the UK, have temporarily impacted revenue recognition and profitability, but these projects are expected to go live and contribute to revenue by Q1 FY '26. This delay is affecting current earnings but sets the stage for future revenue growth once resolved.

- Strategic initiatives such as price adjustments in the Integrated Final Mile (IFM) business, headcount rationalization, overhead reduction, infrastructure consolidation, and increased outsourcing to India are expected to improve net margins by lowering costs and increasing operational efficiency in upcoming quarters.

- Strong business development efforts continue to yield a robust pipeline of potential deals, estimated at over ₹4,500 crores. This pipeline reflects future revenue growth potential as these deals convert into contracts and start generating revenue.

- The recent win of a 4-year contract with the UK Ministry of Defense and ongoing negotiations for a large transformational contract underscore the company's ability to secure large deals, particularly with Fortune 500 companies, which bodes well for future revenue streams.

- Tech-led innovations and operational excellence initiatives are expected to enhance service delivery and customer satisfaction, potentially leading to increased contract renewals and new business, positively impacting long-term revenue and profitability.

TVS Supply Chain Solutions Future Earnings and Revenue Growth

Assumptions

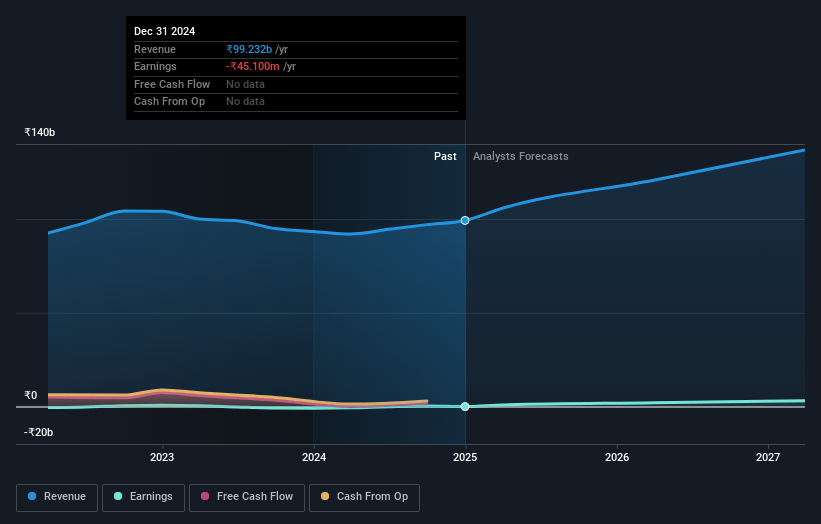

How have these above catalysts been quantified?- Analysts are assuming TVS Supply Chain Solutions's revenue will grow by 12.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from -0.0% today to 3.1% in 3 years time.

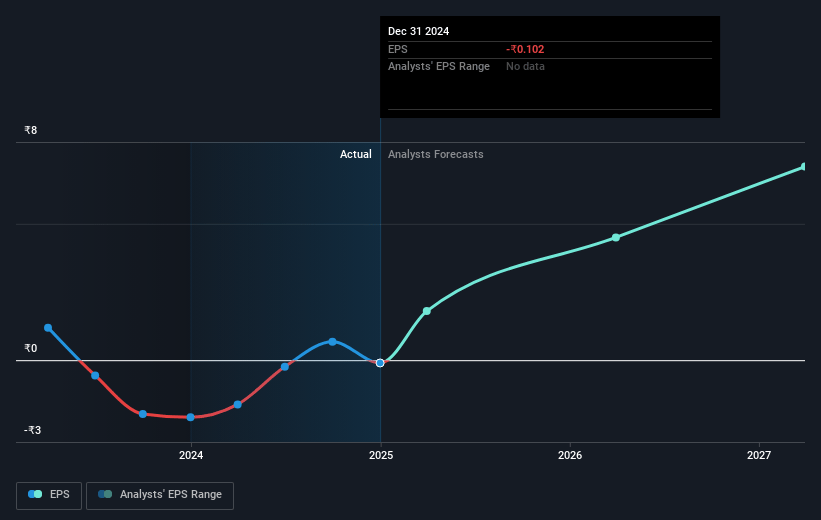

- Analysts expect earnings to reach ₹4.4 billion (and earnings per share of ₹10.0) by about May 2028, up from ₹-45.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 20.8x on those 2028 earnings, up from -1128.4x today. This future PE is lower than the current PE for the IN Logistics industry at 24.4x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.53%, as per the Simply Wall St company report.

TVS Supply Chain Solutions Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The Red Sea crisis continues to drive higher shipping costs and delays, impacting the company’s freight forwarding operations, which could pressure revenues and net margins.

- Delays in commissioning a major project in the U.K. have pushed expected revenues to Q1 FY '26, which will negatively affect short-term earnings and profitability.

- Outsourcing lower-than-expected volumes in the U.K. region has been an issue, causing an unusual revenue drop in Q3, impacting immediate revenue figures.

- Procedural delays with a key U.K. governmental contract have postponed anticipated revenue, squeezing profitability due to pre-built relevant costs.

- The freight forwarding segment has seen pressure on margins due to pass-through costs related to the Red Sea surcharge, limiting earnings potential despite revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹138.0 for TVS Supply Chain Solutions based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹141.2 billion, earnings will come to ₹4.4 billion, and it would be trading on a PE ratio of 20.8x, assuming you use a discount rate of 14.5%.

- Given the current share price of ₹115.35, the analyst price target of ₹138.0 is 16.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.