Narratives are currently in beta

Key Takeaways

- Increased international traffic and capacity expansions at Delhi and Hyderabad airports are expected to boost revenue and improve net margins.

- New high-margin ventures like Duty Free and effective refinancing strategies aim to enhance financial health and earnings growth.

- Regulatory uncertainties and rising finance costs strain GMR Airports' profitability, with declining margins and increased debt affecting future earnings potential.

Catalysts

About GMR Airports- Operates and develops airports in India.

- There is a notable increase in passenger traffic at GMR Airports, particularly international traffic, due to the growth in visa applications and the resurgence of travel events. This is expected to boost future revenues.

- The expected traffic increase and upcoming tariff revisions at Delhi Airport could help improve net margins, given the scale and capacity expansions that are now complete.

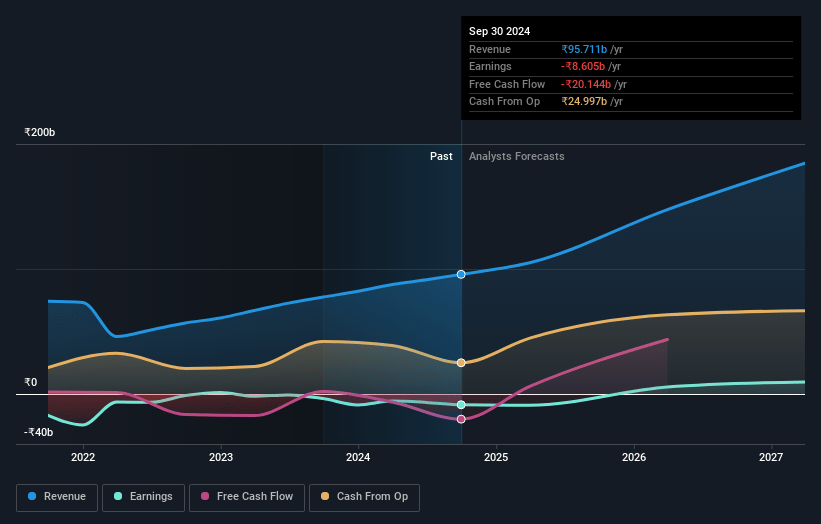

- Significant capital expansions have been completed at Delhi and Hyderabad airports, allowing passenger capacity to increase substantially. The expectation is that these expansions will lead to revenue growth and improved earnings over time as higher capacity is monetized.

- GMR Airports has entered into new business areas such as Duty Free at Delhi Airport, with operations expected to commence in July 2025. This new income stream has the potential to increase earnings due to its high-margin nature.

- The refinancing strategies and repayment plans are expected to lower interest costs over time, directly impacting net margins and leading to better overall financial health and future EPS growth.

GMR Airports Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming GMR Airports's revenue will grow by 30.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from -9.0% today to 7.4% in 3 years time.

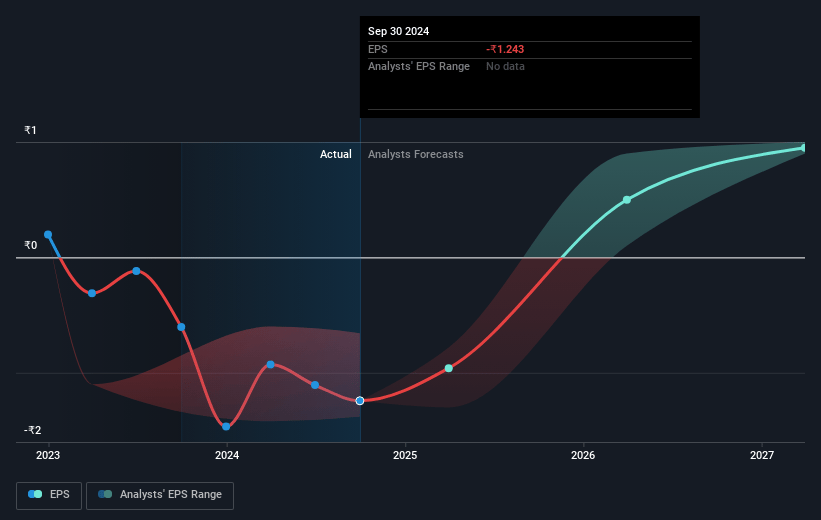

- Analysts expect earnings to reach ₹15.7 billion (and earnings per share of ₹0.95) by about December 2027, up from ₹-8.6 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 142.0x on those 2027 earnings, up from -102.1x today. This future PE is greater than the current PE for the IN Infrastructure industry at 9.0x.

- Analysts expect the number of shares outstanding to grow by 16.13% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 16.91%, as per the Simply Wall St company report.

GMR Airports Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- GMR Airports reported a loss from continuing operations of ₹4.3 billion due to higher finance costs and depreciation post the expansion of Delhi and Hyderabad airports. This could adversely impact net margins.

- Consolidated net debt increased to ₹287 billion, reflecting rising borrowing costs for projects like Bhogapuram and balance capital expenditures at Delhi, which could strain future earnings.

- The EBITDA margin decreased from 52% in the prior year to 49% this quarter, potentially indicating increased costs or reduced efficiency affecting profitability.

- Non-aero revenues at Hyderabad Airport were flat despite higher passenger volumes, suggesting that growth in non-aero revenue streams may not be keeping pace with expectations, potentially affecting total income.

- There are regulatory and legal uncertainties, including pending Supreme Court hearings concerning tariff benefits, which, if resolved unfavorably, could impact revenue streams and future profit projections.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹84.33 for GMR Airports based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹110.0, and the most bearish reporting a price target of just ₹69.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be ₹212.0 billion, earnings will come to ₹15.7 billion, and it would be trading on a PE ratio of 142.0x, assuming you use a discount rate of 16.9%.

- Given the current share price of ₹83.21, the analyst's price target of ₹84.33 is 1.3% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives