Key Takeaways

- Demerging the western wear business could unlock value and drive growth, positively affecting future earnings.

- Strategic focus on premiumization and cost control is expected to expand EBITDA margins, enhancing profitability.

- Subdued consumption and strategic changes, including store closures and brand demergers, could impact revenue growth, profitability, and operational stability in the short term.

Catalysts

About Aditya Birla Fashion and Retail- Designs, manufactures, distributes, and retails fashion apparel and accessories in India and internationally.

- The demerger of the western wear brands business into a separate entity, Aditya Birla Lifestyle Brands Limited (ABLBL), is expected to be completed soon. This strategic move could unlock value and drive growth, positively impacting future earnings.

- The successful equity capital raise of USD 490 million to make the company debt-free and support growth initiatives indicates strong financial positioning. This could significantly improve net margins and earnings.

- The company's strategic focus on premiumization, channel mix optimization, and cost control is expected to continue driving EBITDA margin expansion, positively impacting profitability.

- Aggressive expansion plans, including opening 300+ new stores across the portfolio and accelerating expansion in emerging segments, could enhance revenue growth.

- The consolidation and optimization of retail networks, including strategic exits and store closures, are expected to improve overall profitability by focusing on higher-margin opportunities, ultimately boosting net margins.

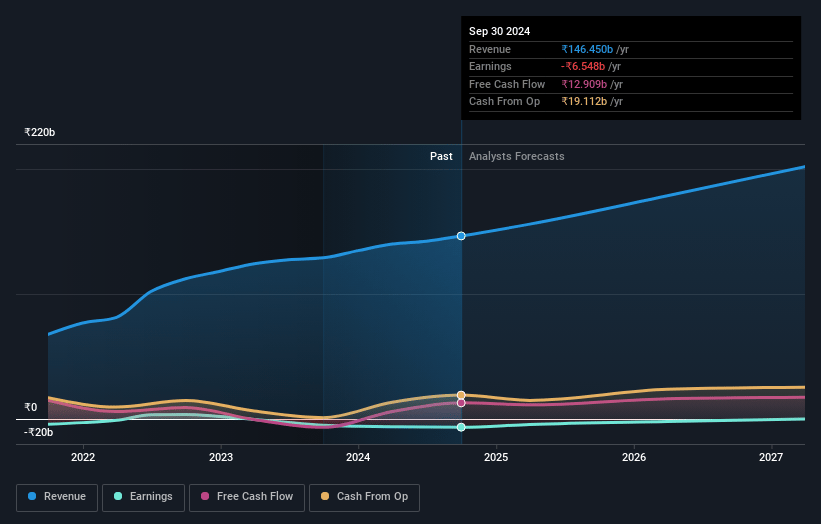

Aditya Birla Fashion and Retail Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Aditya Birla Fashion and Retail's revenue will grow by 11.9% annually over the next 3 years.

- Analysts are not forecasting that Aditya Birla Fashion and Retail will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Aditya Birla Fashion and Retail's profit margin will increase from -4.2% to the average IN Specialty Retail industry of 3.4% in 3 years.

- If Aditya Birla Fashion and Retail's profit margin were to converge on the industry average, you could expect earnings to reach ₹7.1 billion (and earnings per share of ₹5.27) by about April 2028, up from ₹-6.3 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 82.5x on those 2028 earnings, up from -49.3x today. This future PE is greater than the current PE for the IN Specialty Retail industry at 35.5x.

- Analysts expect the number of shares outstanding to grow by 5.8% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.58%, as per the Simply Wall St company report.

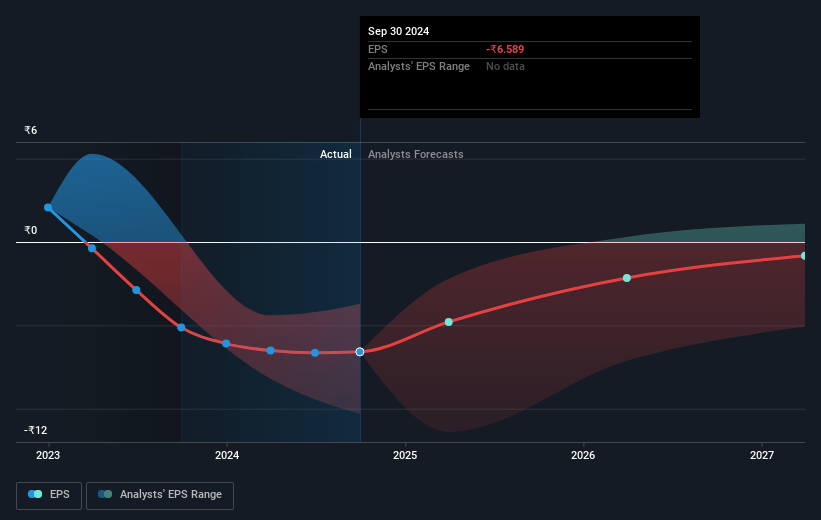

Aditya Birla Fashion and Retail Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The overall consumption environment remains subdued, with inconsistent footfalls outside of the festive and wedding season, potentially impacting revenue and earnings growth.

- The demerger of the western wear brands into a separate entity and ongoing restructuring may lead to short-term operational disruptions and may affect the net margins.

- Closure of underperforming stores, especially in smaller markets, may limit growth potential and lead to immediate reductions in revenue from those locations.

- The ongoing distribution rationalization for TCNS, including degrowth in wholesale and e-commerce channels, could have adverse impacts on revenue and profitability if not managed carefully.

- Style Up and other emerging segments, while showing potential, require significant capital investment to become profitable, affecting current cash flow and potentially delaying improvements to net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹281.591 for Aditya Birla Fashion and Retail based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹346.0, and the most bearish reporting a price target of just ₹230.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹207.0 billion, earnings will come to ₹7.1 billion, and it would be trading on a PE ratio of 82.5x, assuming you use a discount rate of 15.6%.

- Given the current share price of ₹272.9, the analyst price target of ₹281.59 is 3.1% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.