Key Takeaways

- Strategic expansion in leasing and robust project pipelines in design and build promise strong revenue growth and enhanced profitability.

- Diversification across industries is poised to stabilize revenue streams and mitigate economic risks, bolstering long-term earnings stability.

I'm sorry, but it looks like the text you mentioned was not provided in the message. Could you please provide the financial narrative about EFC (I) so I can assist you with your request?

Catalysts

About EFC (I)- Engages in real estate leasing business in India.

- The new certificate of registration for EFC's Emberstone SM REIT, which is about to file an offer document, presents a promising growth avenue that could enhance revenue and boost the bottom line by generating fee-based income through management operations.

- EFC's strategic expansion of its leasing vertical, with assets under management increasing to over 2.6 million square feet and a high occupancy rate of 90%, shows the potential for continued robust rental revenue growth, thus positively influencing EBITDA.

- The impressive growth in the design and build vertical, with a strong project pipeline worth ₹92 crores, indicates potential revenue increases and enhanced margins as these projects progress to completion.

- The furniture division has a robust order pipeline and the capability to achieve high-margin business, potentially reaching around 30% EBITDA, enhancing overall profitability.

- EFC's focus on spreading its business across diverse industries like real estate, education, and healthcare is likely to stabilize and boost revenue streams, mitigating risks from economic downturns and improving long-term earnings stability.

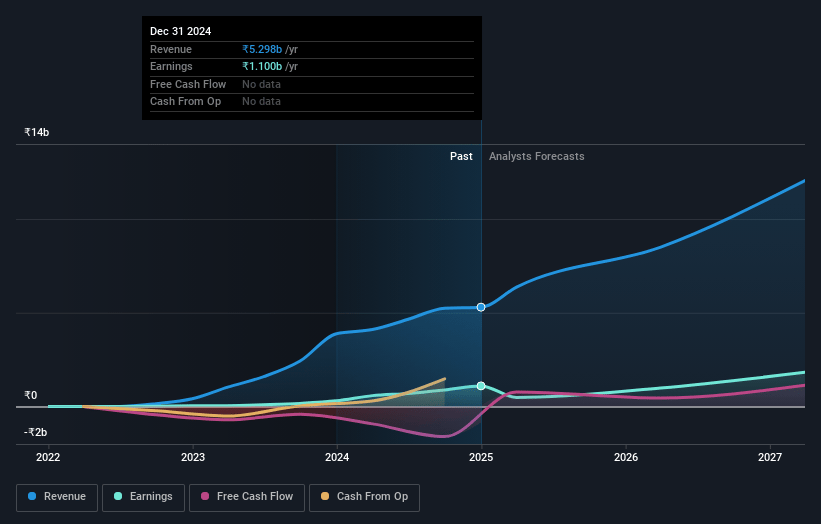

EFC (I) Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming EFC (I)'s revenue will grow by 42.0% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 20.8% today to 14.8% in 3 years time.

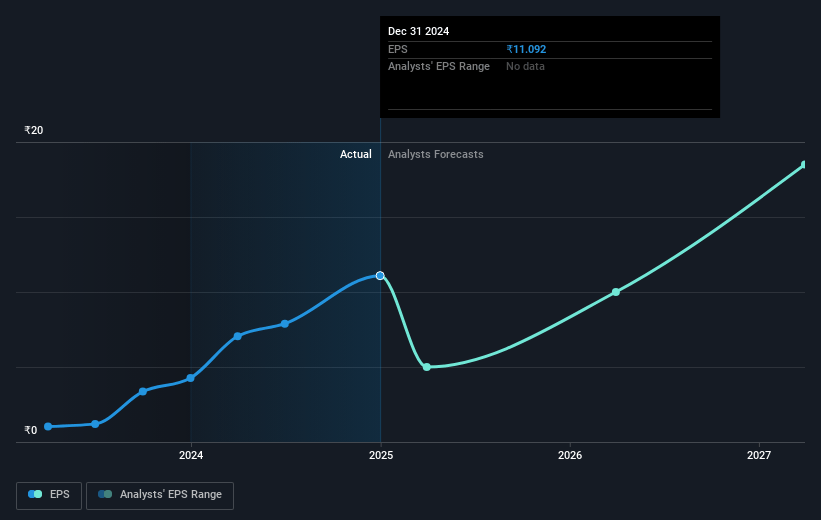

- Analysts expect earnings to reach ₹2.2 billion (and earnings per share of ₹22.72) by about May 2028, up from ₹1.1 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 19.3x on those 2028 earnings, down from 24.4x today. This future PE is lower than the current PE for the IN Retail Distributors industry at 27.4x.

- Analysts expect the number of shares outstanding to decline by 6.24% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.05%, as per the Simply Wall St company report.

EFC (I) Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- .

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹365.0 for EFC (I) based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹15.2 billion, earnings will come to ₹2.2 billion, and it would be trading on a PE ratio of 19.3x, assuming you use a discount rate of 13.1%.

- Given the current share price of ₹269.35, the analyst price target of ₹365.0 is 26.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.