Key Takeaways

- EU GMP certification could enable Orchid Pharma's European market expansion and boost future revenue.

- Investments in Orchid AMS targeting antimicrobial resistance are expected to enhance future profitability.

- Market realignment, pricing pressures, and regulatory uncertainties could hinder Orchid Pharma's revenue growth and strain future earnings.

Catalysts

About Orchid Pharma- A pharmaceutical company, engages in the development, manufacture, and marketing of active pharmaceutical ingredients, bulk actives, finished dosage formulations, and nutraceuticals in India.

- The successful EU GMP audit and certification is a significant milestone, which could enable Orchid Pharma to expand its presence in European markets and boost future revenue.

- The launch of Exblifep (Cefepime and Enmetazobactam) has shown promising early adoption trends globally, with potential for exponential future revenue growth.

- The company’s significant investments in the Orchid AMS division aim to tackle antimicrobial resistance and are expected to enhance profitability in the future as it gains traction.

- The advancement of the 7ACA project, crucial for strengthening API capabilities, is expected to bring cost synergies upon completion, positively impacting net margins.

- The potential U.S. partnership for Enmetazobactam could unlock significant market opportunities and drive earnings growth once finalized.

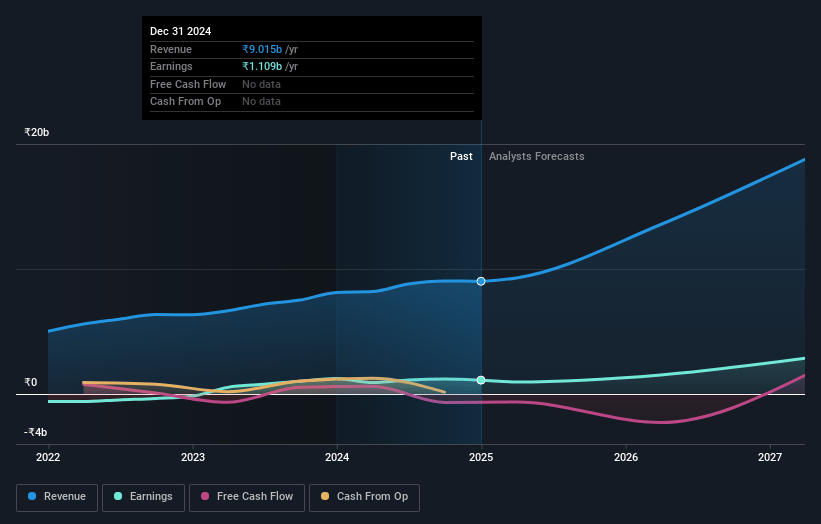

Orchid Pharma Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Orchid Pharma's revenue will grow by 37.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.3% today to 16.1% in 3 years time.

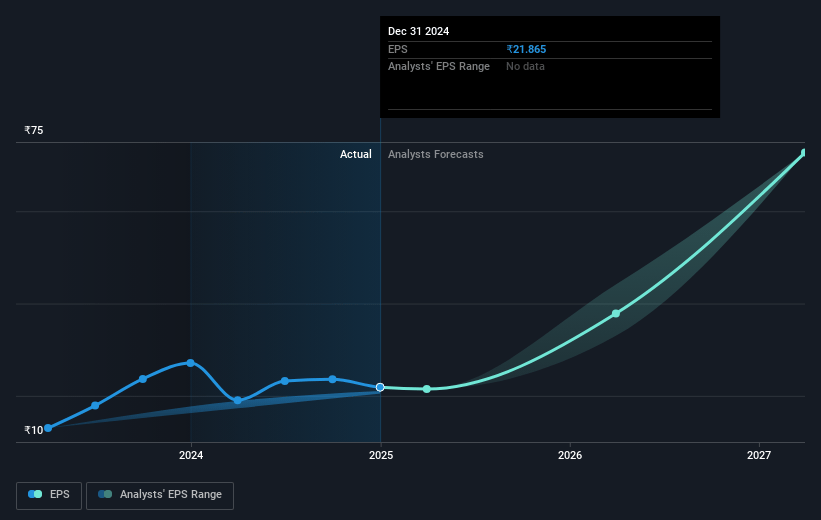

- Analysts expect earnings to reach ₹3.8 billion (and earnings per share of ₹68.69) by about April 2028, up from ₹1.1 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 28.2x on those 2028 earnings, down from 35.5x today. This future PE is greater than the current PE for the IN Pharmaceuticals industry at 27.9x.

- Analysts expect the number of shares outstanding to decline by 0.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.53%, as per the Simply Wall St company report.

Orchid Pharma Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The market is undergoing a realignment between demand and supply, which presents challenges that could mute total sales numbers despite a volume increase, affecting revenue growth.

- Price corrections in key products have impacted the top line, and continuous pressure on pricing due to volatility and competition from Chinese manufacturers could affect net margins.

- There are concerns regarding the progress and execution of the 7ACA project, with potential delays and regulatory uncertainties surrounding government support and antidumping measures, which could strain future earnings.

- The AMS division is currently an EBITDA drag due to ongoing investment in building the team and interactions with medical communities, impacting short-term profitability.

- Uncertainty in the U.S. market launch for partnerships and regulatory issues like the delay in finalizing a partner in the U.S. for a new product might lead to lost time and opportunity, affecting future earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹1502.667 for Orchid Pharma based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹1843.0, and the most bearish reporting a price target of just ₹1095.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹23.6 billion, earnings will come to ₹3.8 billion, and it would be trading on a PE ratio of 28.2x, assuming you use a discount rate of 12.5%.

- Given the current share price of ₹775.9, the analyst price target of ₹1502.67 is 48.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.