Key Takeaways

- Surya Roshni's innovation in lighting and consumer durables seeks revenue growth via premium products and operational efficiency enhancements.

- Expansion into international markets aims to boost exports and reduce domestic market risk, ensuring stable revenue streams.

- The company faces revenue challenges due to declining HR coil prices, industry-wide pressures, tariff policies, and necessary expansions, threatening margins and profitability.

Catalysts

About Surya Roshni- Manufactures and markets steel pipes and tubes, lighting products, fans, home appliances, and PVC pipes in India.

- Surya Roshni's focus on product innovation and premiumization, particularly within the Lighting & Consumer Durables segment, is expected to drive significant revenue growth and improve net margins through enhanced product offerings and operational efficiencies.

- Investment in a new domestic wire business unit and backward integration in the Lighting division is anticipated to bolster revenue and enhance EBITDA margins by optimizing production processes and reducing dependency on external suppliers.

- The expansion of Surya Roshni's steel plant capabilities, including the introduction of Direct Forming Technology and new spiral and cold rolling plants, is expected to increase overall volumes and improve EBITDA per ton, positively impacting earnings.

- Surya Roshni's strategic efforts to expand market reach in international markets such as the Middle East, Saudi Arabia, Europe, and Canada are likely to boost export revenues and mitigate risks from domestic market fluctuations, providing a stable revenue stream.

- The planned increase in capital expenditure to expand capacity and enhance production technologies in both Lighting and Steel segments is projected to support long-term revenue growth and profitability by meeting rising demand in high-value product sectors.

Surya Roshni Future Earnings and Revenue Growth

Assumptions

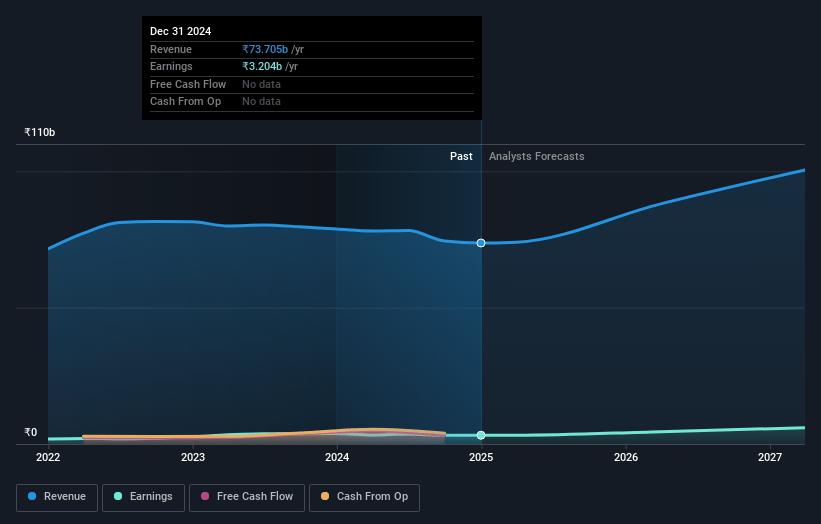

How have these above catalysts been quantified?- Analysts are assuming Surya Roshni's revenue will grow by 14.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.3% today to 6.5% in 3 years time.

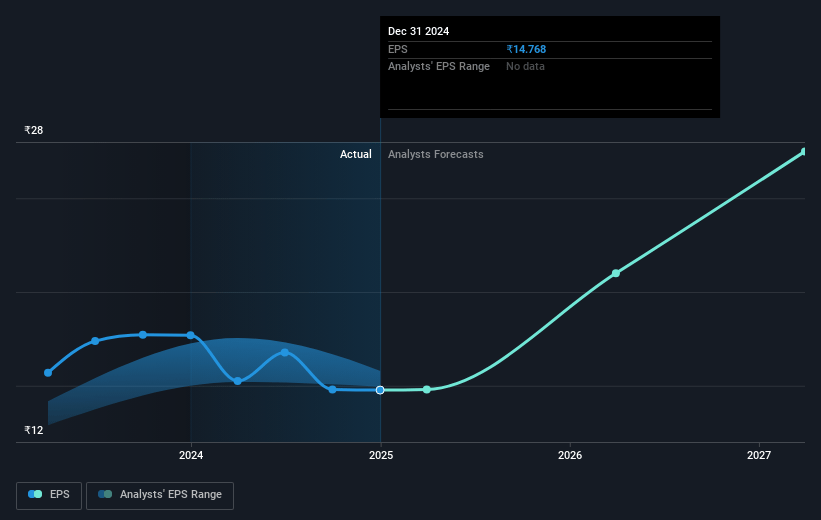

- Analysts expect earnings to reach ₹7.3 billion (and earnings per share of ₹33.71) by about March 2028, up from ₹3.2 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 13.8x on those 2028 earnings, down from 16.6x today. This future PE is lower than the current PE for the IN Metals and Mining industry at 19.8x.

- Analysts expect the number of shares outstanding to grow by 0.33% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.43%, as per the Simply Wall St company report.

Surya Roshni Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's revenue witnessed a marginal decline of 4% due to an 18% year-on-year decrease in HR coil prices, which could negatively impact future revenue trajectories.

- The Steel Pipes and Strips segment experienced an 8% year-on-year revenue decline and a decrease in EBITDA per ton, indicating challenges in maintaining pricing power and stable earnings.

- Despite growth in Lighting & Consumer Durables, industry-wide challenges such as price erosion in the LED segment pose a risk to sustaining net margins and profitability.

- Export sales in the Steel Pipes segment remained unchanged due to global trade uncertainties and U.S. tariff policies, which could stifle international revenue growth opportunities.

- The necessity of substantial expansions and CapEx investment to maintain growth in certain business segments introduces financial risks that could strain earnings if not carefully managed.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹307.0 for Surya Roshni based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹111.9 billion, earnings will come to ₹7.3 billion, and it would be trading on a PE ratio of 13.8x, assuming you use a discount rate of 14.4%.

- Given the current share price of ₹244.48, the analyst price target of ₹307.0 is 20.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.