Key Takeaways

- Expansion into high-margin alloys and anticipated defense orders positions MIDHANI for significant revenue and earnings growth.

- Efficiency improvements and cost reductions are expected to sustain strong EBITDA margins.

- Declining revenue, raw material dependence, and investment risks threaten profitability, amid challenges in achieving revenue consistency and joint venture uncertainties.

Catalysts

About Mishra Dhatu Nigam- Manufactures and sells super alloys, titanium, special purpose steel, and other special metals in India and internationally.

- Mishra Dhatu Nigam (MIDHANI) has secured a record order book of ₹1,906 crores, with expectations to increase it to ₹1,700 crores in FY '25, which signals significant future revenue growth potential.

- The company is planning to invest in new alloys for aerospace and naval applications, such as Advanced Ultra-Supercritical (AUSC) alloys, which could drive higher-margin revenue streams due to their specialized nature.

- MIDHANI's successful reduction in raw material costs, particularly with nickel, improved efficiencies, and a shift toward using plant returns (scrap) are expected to sustain or increase EBITDA margins.

- The anticipated orders from ISRO and strategic defense sectors are likely to enhance revenue streams with high-value contracts, providing opportunities for improved profitability.

- Developments in titanium production facilities to meet future defense and aerospace demands could expand MIDHANI's market reach and boost earnings growth by attracting new orders in these high-demand areas.

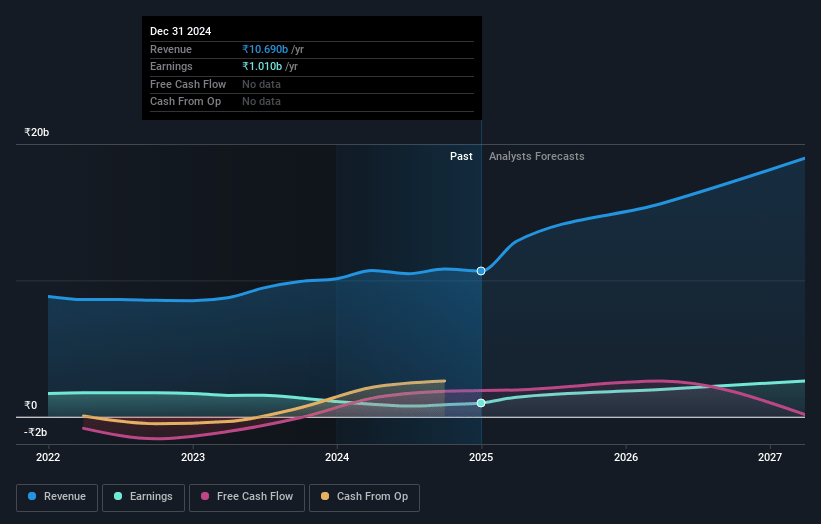

Mishra Dhatu Nigam Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Mishra Dhatu Nigam's revenue will grow by 28.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.4% today to 15.1% in 3 years time.

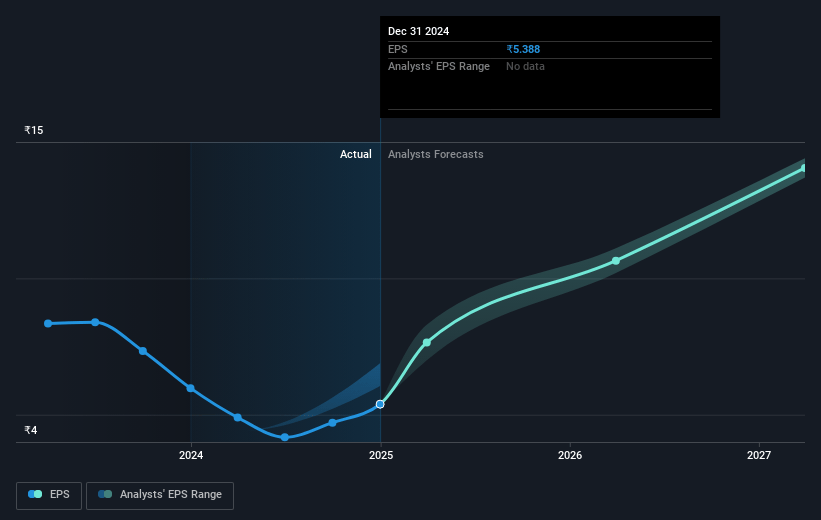

- Analysts expect earnings to reach ₹3.4 billion (and earnings per share of ₹18.2) by about May 2028, up from ₹1.0 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 33.4x on those 2028 earnings, down from 57.0x today. This future PE is greater than the current PE for the IN Metals and Mining industry at 20.9x.

- Analysts expect the number of shares outstanding to grow by 0.18% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.52%, as per the Simply Wall St company report.

Mishra Dhatu Nigam Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's revenue and Value of Production (VoP) have shown a decline compared to the previous year, indicating potential challenges in maintaining consistent revenue growth.

- MIDHANI's financial performance improvement is partly attributed to advantageous raw material price reductions, which could reverse if global market conditions change, impacting net margins.

- The reliance on foreign sources for critical raw materials like nickel presents a risk due to potential geopolitical issues or supply chain disruptions, which could affect earnings.

- The joint venture with NALCO has faced delays and lacks encouraging market data, suggesting uncertainty regarding its future viability and potential impact on revenue growth.

- The substantial future investments required, such as the proposed ₹100 crores CapEx, suggest potential risks of capital misallocation if expected returns are not realized, impacting profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹402.5 for Mishra Dhatu Nigam based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹22.5 billion, earnings will come to ₹3.4 billion, and it would be trading on a PE ratio of 33.4x, assuming you use a discount rate of 14.5%.

- Given the current share price of ₹307.0, the analyst price target of ₹402.5 is 23.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.