Key Takeaways

- Protective import measures and increased solar sector demand are set to boost soda ash revenue, supporting stable or improved pricing.

- Diversifying projects, including vacuum salt and bromine, aim to enhance product mix and margins, potentially strengthening future revenue and earnings.

- Competitive pressure from cheaper imports and uncertain import pricing could impact revenue growth, with strategic projects offering future potential amidst current capacity constraints.

Catalysts

About GHCL- Manufactures and sells inorganic chemicals in India and internationally.

- The imposition of a Minimum Import Price (MIP) on soda ash is expected to protect domestic producers from cheaper imports, potentially leading to stable or improved pricing and supporting revenue growth.

- Increased allocation towards the solar power sector in the Union Budget '25-'26 is projected to boost domestic demand for soda ash, which is used in manufacturing solar glass, potentially leading to higher volumes and revenue.

- Strategic projects, including a greenfield project and a new salt field in Gujarat, are underway and expected to be completed within three years, ultimately diversifying the product mix and potentially enhancing future revenue streams.

- The commissioning of vacuum salt and bromine projects by 2026 is anticipated to diversify the product offerings and contribute to higher earnings, due to the higher margins associated with these products.

- The company's ongoing focus on operational efficiency and cost optimization is expected to sustain or improve net margins, even amid pricing pressures in the soda ash market.

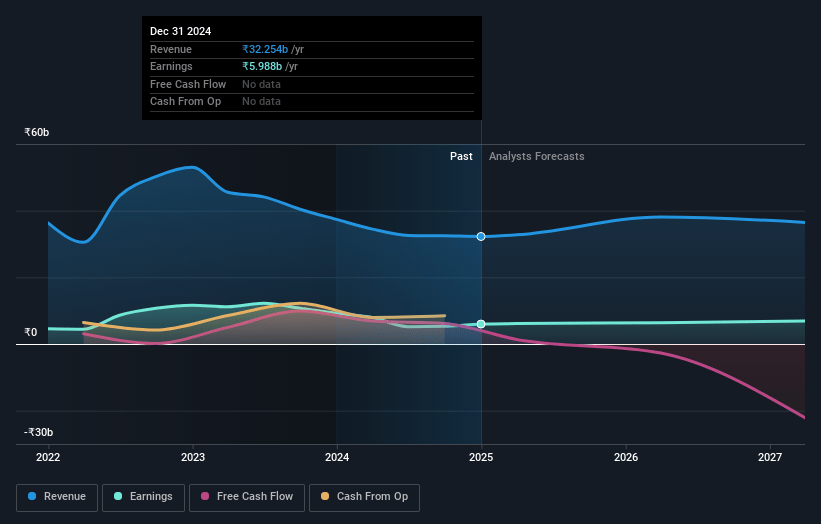

GHCL Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming GHCL's revenue will grow by 6.9% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 18.6% today to 18.2% in 3 years time.

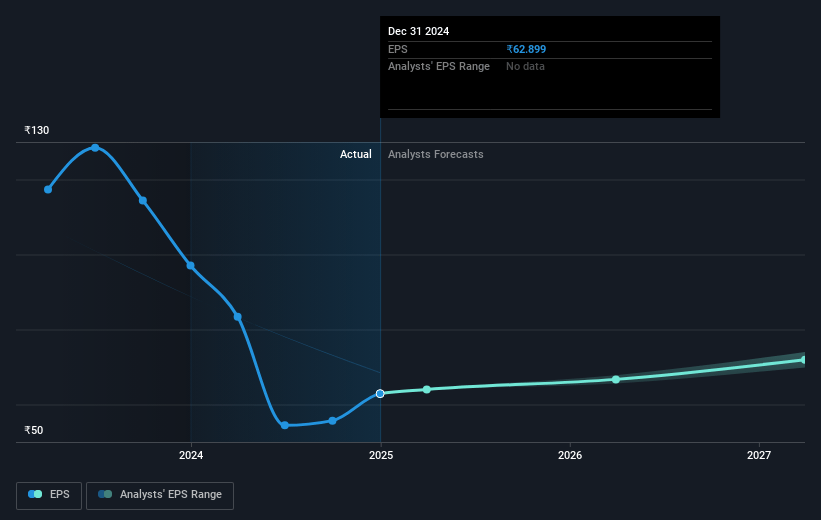

- Analysts expect earnings to reach ₹7.2 billion (and earnings per share of ₹74.79) by about March 2028, up from ₹6.0 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.2x on those 2028 earnings, up from 10.1x today. This future PE is lower than the current PE for the IN Chemicals industry at 24.2x.

- Analysts expect the number of shares outstanding to grow by 1.57% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.56%, as per the Simply Wall St company report.

GHCL Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Increased cheaper imports into India have impacted operating revenues, creating competitive pressure and affecting margin sustainability. This can negatively impact revenue and profitability.

- There is uncertainty around how the Minimum Import Price (MIP) will affect the volume and pricing of soda ash imports. Potential supply chain disruptions or short-term benefits might not substantially improve prices, thus impacting expected revenue growth.

- The Western economy is experiencing suppressed demand due to adverse business sentiments, which could result in reduced global sales, and indirectly impact revenue, especially if price recovery is delayed.

- Strategic growth initiatives like new projects are expected to bear fruit in the next few years; until then, current capacity constraints and limited volume growth may restrict earnings growth.

- The improvement in margins due to cost efficiencies may not sustain indefinitely owing to market volatility. Shooting other income that contributed to recent EBITDA improvements may not be replicable in subsequent quarters, affecting future earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹820.0 for GHCL based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹39.4 billion, earnings will come to ₹7.2 billion, and it would be trading on a PE ratio of 17.2x, assuming you use a discount rate of 14.6%.

- Given the current share price of ₹630.0, the analyst price target of ₹820.0 is 23.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.