Key Takeaways

- Strong growth in new segments and eco-friendly innovations could drive significant revenue and margin expansion for Fineotex.

- Strategic expansions and financial position enable pursuit of acquisitions, enhancing potential for sustainable earnings growth.

- Political instability in Bangladesh, muted FMCG demand, and execution risks in new sectors hinder Fineotex Chemical's growth and profit margins.

Catalysts

About Fineotex Chemical- Engages in manufactures and sells textile chemicals, and auxiliary and specialty chemicals in India.

- Fineotex is poised to benefit from strong growth in its new segments, oil and gas, and water treatment, which are seeing increased demand and a robust order pipeline. This is expected to contribute positively to future revenue growth.

- The launch of AquaStrike Premium, a biotechnology-based mosquito control product, opens up significant market opportunities due to its eco-friendly nature and applicability in water preservation, which could lead to increased revenues.

- Expansion in upstream activities and eco-friendly solutions in the oil and gas sector, like water-based drilling fluid, will likely enhance revenue streams and possibly increase net margins due to higher demand for specialty chemicals.

- The upcoming new manufacturing plant, expected to become operational in Q2 FY '26, will increase production capacity, supporting revenue growth and potentially improving operational efficiencies, which can lead to better net margins.

- Sufficient earmarked funds and a positive credit rating outlook position Fineotex well to pursue strategic acquisitions and expansions, which can result in substantial revenue gains and sustainable earnings growth.

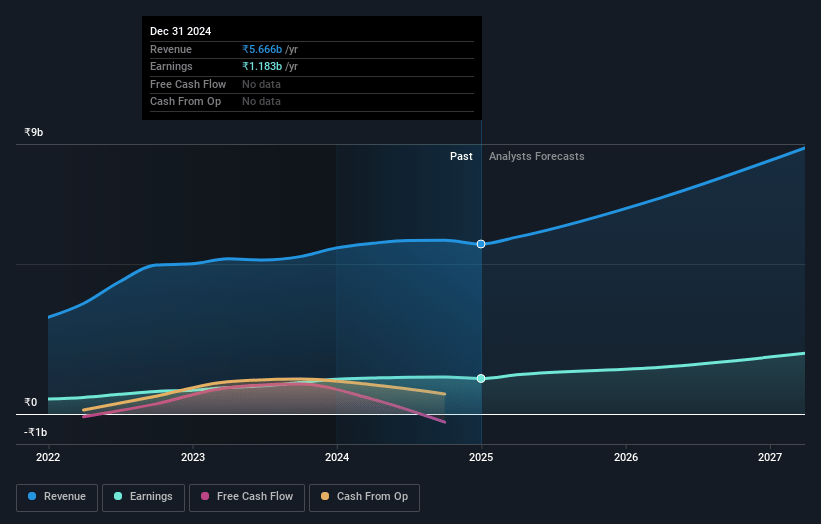

Fineotex Chemical Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Fineotex Chemical's revenue will grow by 21.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 20.9% today to 23.1% in 3 years time.

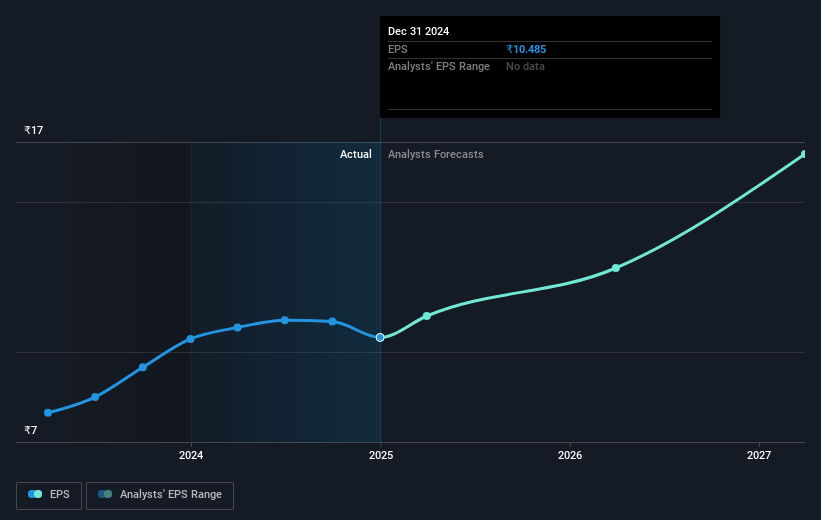

- Analysts expect earnings to reach ₹2.4 billion (and earnings per share of ₹18.86) by about May 2028, up from ₹1.2 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 27.8x on those 2028 earnings, up from 23.0x today. This future PE is greater than the current PE for the IN Chemicals industry at 25.1x.

- Analysts expect the number of shares outstanding to grow by 2.67% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.37%, as per the Simply Wall St company report.

Fineotex Chemical Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Political and social turmoil in Bangladesh has led to a decrease in exports, reducing revenue from an important textile market.

- Muted demand in the FMCG sector has also impacted revenue growth, affecting overall sales despite gains in other segments.

- The shift in product mix and order postponements, such as those from Bangladesh, have led to a modest decline in quarterly total income by 8.5%, potentially lowering net margins.

- The reliance on government approvals and NGO partnerships for the AquaStrike Premium product introduces regulatory and partnership risks, which could delay revenue generation from this new product line.

- While the expansion into oil and gas sectors and the development of new products is promising, it comes with significant execution risks, as these industries have high entry barriers and any missteps could negatively affect earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹366.0 for Fineotex Chemical based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹10.2 billion, earnings will come to ₹2.4 billion, and it would be trading on a PE ratio of 27.8x, assuming you use a discount rate of 13.4%.

- Given the current share price of ₹237.69, the analyst price target of ₹366.0 is 35.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.