Narratives are currently in beta

Key Takeaways

- Strategic pricing and premium product innovations aim to maintain margins, tapping into trends like digital sales for enhanced revenue growth.

- Expanding distribution in rural areas and investing in health and wellbeing diversifies growth sources and strengthens market penetration.

- Rising input costs and market challenges may pressure Hindustan Unilever's margins and earnings, with potential further impact from strategic business separations.

Catalysts

About Hindustan Unilever- A fast-moving consumer good company, manufactures and sells food, home care, personal care, and refreshment products in India and internationally.

- Hindustan Unilever plans to leverage its strong market presence by launching new premium product innovations, such as TRESemme’s lamellar gloss range and Pond’s Hydra Miracle body gel lotion, which are expected to drive premiumization and increase revenue.

- The company is focusing on expanding its distribution, especially in rural areas, with initiatives like Shikhar, aiming to boost market penetration and volume growth.

- Hindustan Unilever is taking strategic pricing actions to manage commodity inflation in products like tea, aiming to maintain healthy net margins and sustain competitive pricing.

- The shift towards digital channels and e-commerce, with a growing focus on platforms like Shikhar and increased digital advertising, is expected to enhance sales growth and support higher-margin sales through premium and niche-market offerings.

- Diversification into high-growth categories such as health and wellbeing, with investments in brands like OZiva and Wellbeing Nutrition, is anticipated to drive future revenue growth and potentially higher earnings from these emerging segments.

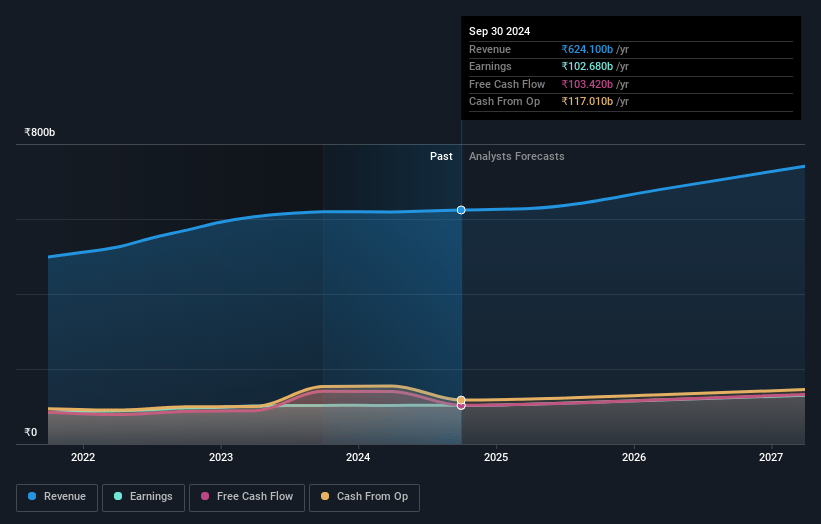

Hindustan Unilever Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Hindustan Unilever's revenue will grow by 6.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 16.5% today to 17.8% in 3 years time.

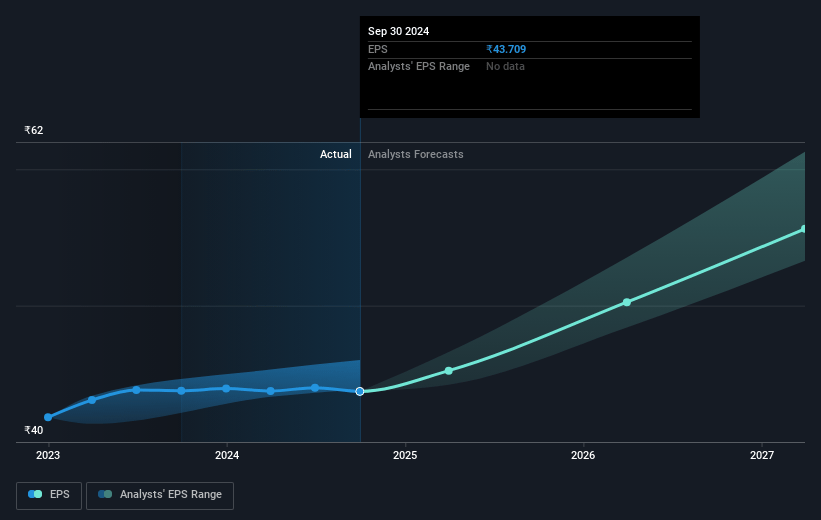

- Analysts expect earnings to reach ₹136.1 billion (and earnings per share of ₹58.32) by about November 2027, up from ₹102.7 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 71.8x on those 2027 earnings, up from 56.6x today. This future PE is greater than the current PE for the IN Personal Products industry at 28.4x.

- Analysts expect the number of shares outstanding to decline by 0.22% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.33%, as per the Simply Wall St company report.

Hindustan Unilever Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Market volume growth trajectory remained muted this quarter, with only 2% underlying sales growth, suggesting potential challenges in driving revenue growth.

- Crude palm oil and tea prices have significantly inflated, leading to increased input costs that may pressure net margins if price adjustments are not adequate or timely.

- Decline in profit after tax before exceptional items by 2% indicates vulnerabilities in net earnings, highlighting the effects of external factors like commodity inflation.

- The separation of the ice cream business, which despite being a smaller segment, may affect overall revenue and margin profiles due to the distinct nature and potential loss of synergies.

- Ongoing struggles in the Foods & Refreshment segment, particularly due to tea downgradation and muted consumption in nutrition drinks, could impact overall earnings if recovery measures are insufficiently quick or effective.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹2878.28 for Hindustan Unilever based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹3400.0, and the most bearish reporting a price target of just ₹2110.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be ₹763.1 billion, earnings will come to ₹136.1 billion, and it would be trading on a PE ratio of 71.8x, assuming you use a discount rate of 13.3%.

- Given the current share price of ₹2475.6, the analyst's price target of ₹2878.28 is 14.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives