Key Takeaways

- Favorable FDI changes and increased healthcare coverage for gig workers boost revenue potential through expanded services and partnerships.

- AI-driven fraud detection and strategic acquisitions reduce costs and enhance revenue and earnings growth.

- Reliance on management estimates, competitive pressures, and technological investments introduces uncertainty and risk, potentially affecting profitability and market share.

Catalysts

About Medi Assist Healthcare Services- Provides third party administration services in India and internationally.

- Elevated FDI limits to 100% and simplification of FDI conditions in India's health insurance sector are likely to provide a solid foundation for international integration, potentially enhancing Medi Assist's revenue via expanded service offerings and partnerships.

- The Indian government's initiative to provide healthcare to gig workers as part of PM Jan Arogya Yojana is expected to increase insurance penetration and demand, potentially driving revenue growth for companies like Medi Assist that administer these plans.

- Technological advancements by Medi Assist, such as using AI and machine learning for fraud detection (e.g., MAven fraud detection engine), could significantly reduce costs and improve net margins, bolstering overall earnings.

- Medi Assist's strategic acquisitions, such as the Paramount TPA, subject to regulatory approval, may provide synergies and expand their premium under management, directly impacting revenue growth positively.

- Focus on enhancing customer experience, minimizing discharge lead times, and maintaining medical inflation below 5%, could improve client retention and attract new insurers to their platform, resulting in sustained revenue and profitability growth.

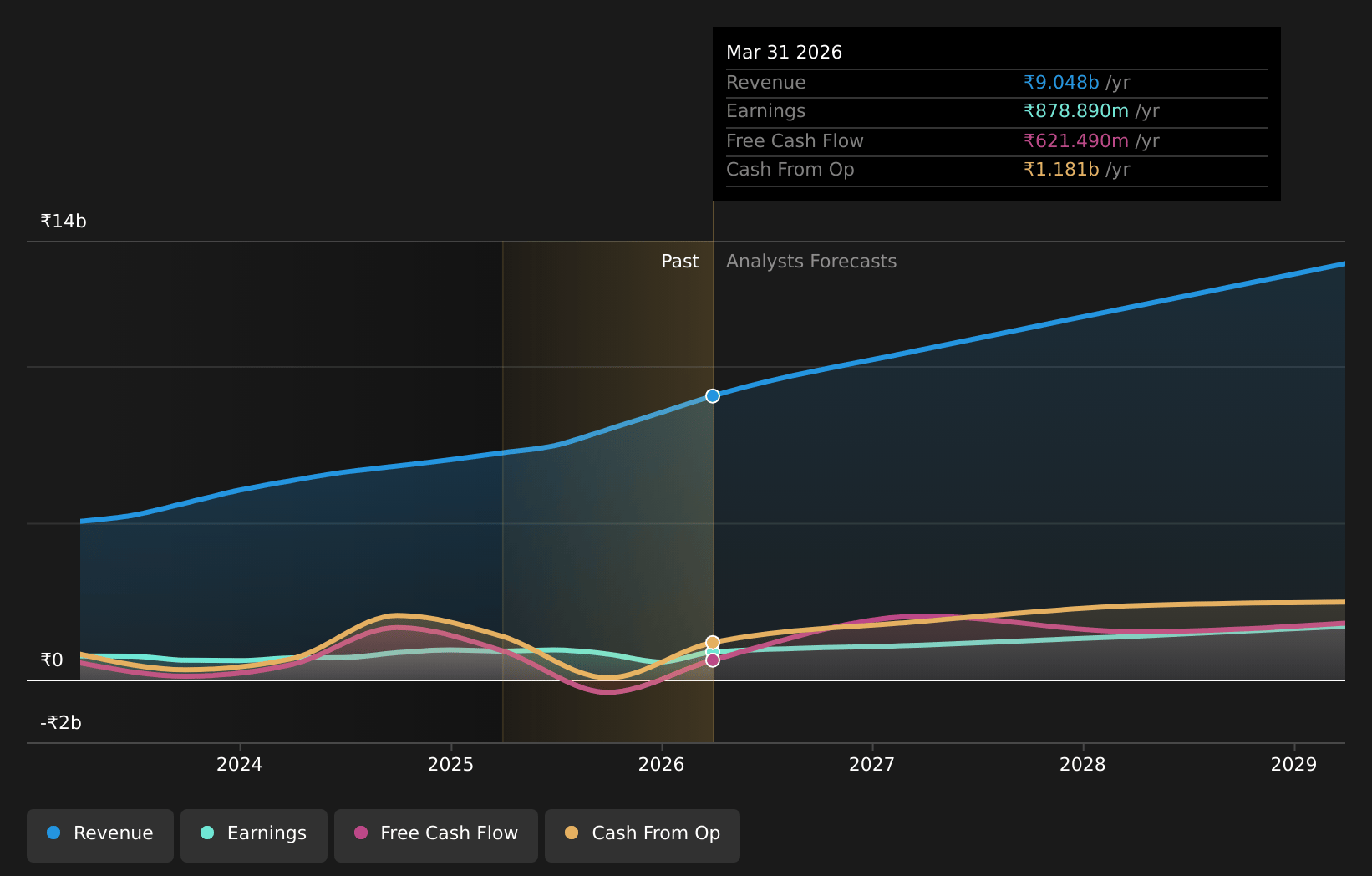

Medi Assist Healthcare Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Medi Assist Healthcare Services's revenue will grow by 24.8% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 13.5% today to 11.2% in 3 years time.

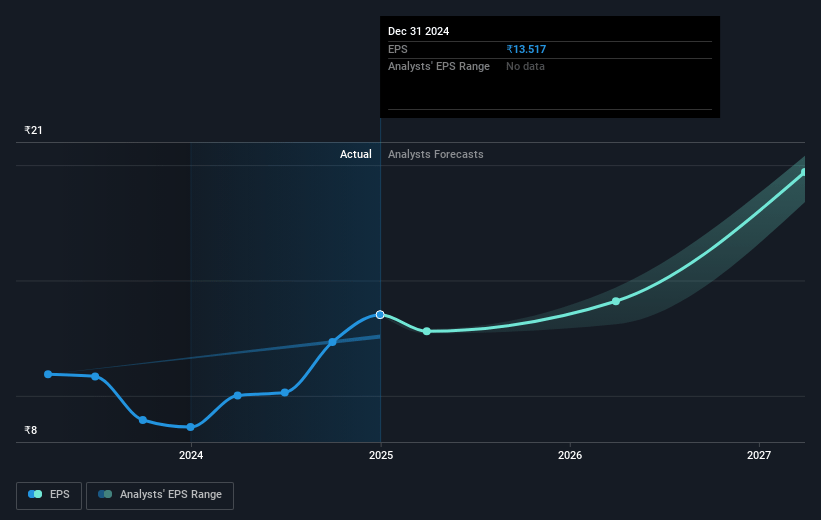

- Analysts expect earnings to reach ₹1.5 billion (and earnings per share of ₹21.67) by about April 2028, up from ₹947.4 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 45.3x on those 2028 earnings, up from 33.4x today. This future PE is greater than the current PE for the IN Healthcare industry at 39.2x.

- Analysts expect the number of shares outstanding to grow by 0.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.53%, as per the Simply Wall St company report.

Medi Assist Healthcare Services Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The reported financials are unaudited and based on management estimates, which adds a level of uncertainty and risk to their reliability. This could potentially impact the accuracy of reported earnings and profitability.

- The company highlights substantial focus on group and retail health insurance segments, but this exposes them to market dynamics like competitive pricing pressures and regulatory changes, which could affect revenue growth.

- There is significant reliance on technology investments to drive business processes, including fraud detection, which, if delayed or ineffective, may not deliver expected operational efficiencies, impacting profit margins.

- Medi Assist's financial results are influenced by claims processing volumes, suggesting sensitivity to external factors like claim inflation rates and government policy shifts, which could impact net margins.

- Increased TPA competition or insurers bringing more business in-house could erode market share, resulting in pressure on revenue and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹693.333 for Medi Assist Healthcare Services based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹13.6 billion, earnings will come to ₹1.5 billion, and it would be trading on a PE ratio of 45.3x, assuming you use a discount rate of 12.5%.

- Given the current share price of ₹448.6, the analyst price target of ₹693.33 is 35.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.