Key Takeaways

- Strategic growth investments and technological enhancements aim to optimize efficiencies and position the company for long-term market leadership and value creation.

- Diversification into comprehensive financial services and expansion in Tier 2 and Tier 3 cities seeks to boost revenue and market share.

- Regulatory and geopolitical challenges, coupled with increased investment expenses and rising customer acquisition costs, are straining short-term profitability and revenue growth.

Catalysts

About Angel One- Provides broking and advisory services, margin funding, loans against shares, and financial products to its clients in India.

- Implementation of F&O regulation and volatile geopolitical conditions have temporarily impacted volumes, but the company views these as temporary setbacks that will ultimately lead to a more sustainable and transparent ecosystem. This improvement in market conditions is expected to positively impact revenue in the long term.

- The company's strategic decision to stay committed to growth investments, even if it affects short-term profitability, positions them for long-term value creation and market leadership. This is likely to enhance future earnings.

- Enhancements in technology, with significant investments in advanced analytics, AI, and machine learning, are anticipated to improve client engagement and operational efficiencies. These developments could positively impact net margins by optimizing internal processes.

- Expansion into comprehensive financial service offerings beyond broking, such as credit, insurance, fixed income, wealth, and asset management, is expected to increase wallet share and diversify revenue streams, potentially boosting overall revenue.

- Leadership efforts, including high-profile branding partnerships and investment in customer acquisition, particularly in Tier 2 and Tier 3 cities, aim to sustain client trust and expand market share, which could drive higher revenue growth and, in turn, improve earnings per share in the future.

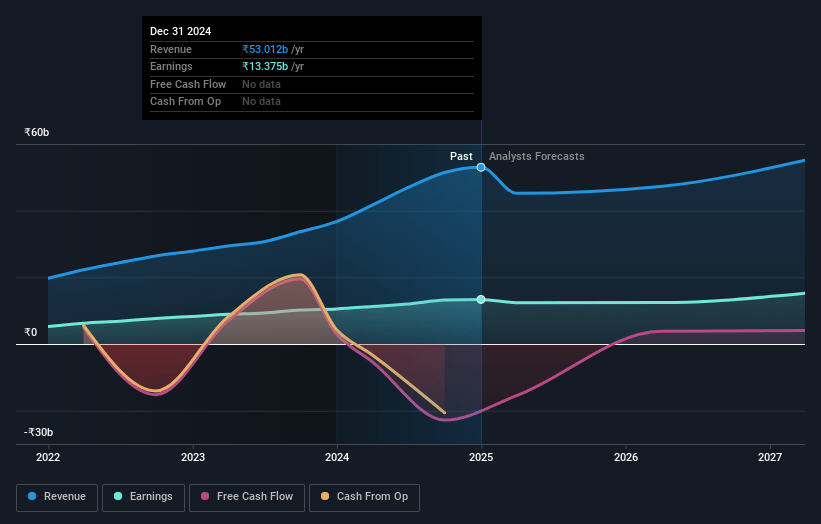

Angel One Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Angel One's revenue will grow by 4.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 23.7% today to 24.7% in 3 years time.

- Analysts expect earnings to reach ₹14.1 billion (and earnings per share of ₹156.55) by about May 2028, up from ₹11.7 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 29.9x on those 2028 earnings, up from 17.8x today. This future PE is greater than the current PE for the IN Capital Markets industry at 19.5x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.57%, as per the Simply Wall St company report.

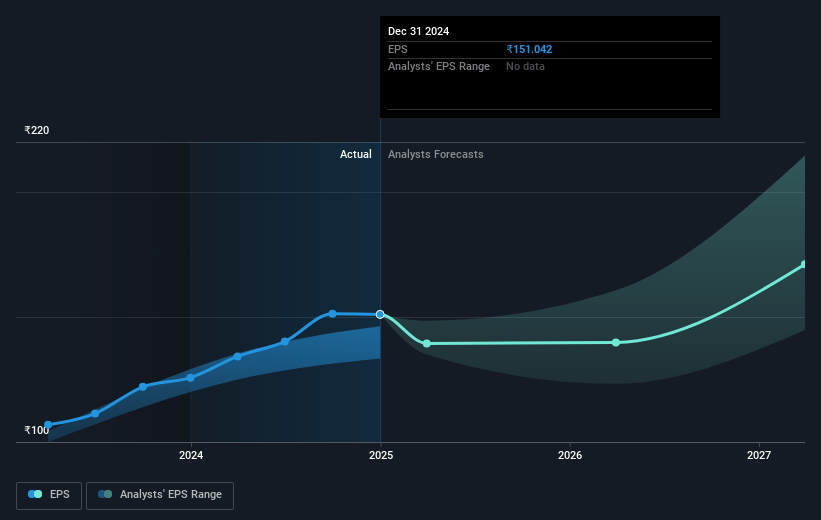

Angel One Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The implementation of F&O regulations and a volatile geopolitical backdrop have led to a decline in trading volume, reduced client participation, and muted order activity, impacting immediate revenue and profitability.

- Increased expenses from growth investments, such as branding partnerships and technology advancements, could affect short-term profitability and operating margins.

- Regulatory disruptions have led to a softened market, negatively impacting gross broking revenue and overall market buoyancy, which affects quarterly revenues.

- The new ventures in asset management and wealth management are currently incurring costs without substantial revenue contributions, affecting net margins in the short term.

- The cost of customer acquisition has increased, affecting profitability and posing a risk if customer LTV (lifetime value) does not increase proportionately with additional products and services offered.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹2556.875 for Angel One based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹2850.0, and the most bearish reporting a price target of just ₹1975.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹57.1 billion, earnings will come to ₹14.1 billion, and it would be trading on a PE ratio of 29.9x, assuming you use a discount rate of 14.6%.

- Given the current share price of ₹2312.3, the analyst price target of ₹2556.88 is 9.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.