Key Takeaways

- Focus on value offerings, product innovations, and expanded day parts aims to boost customer frequency and profit margins.

- Accelerated store expansion and digital kiosk rollouts are expected to improve accessibility and operational efficiency, sustaining revenue growth.

- Negative same-store sales growth and margin pressures signify challenges in revenue sustainability and competitiveness in the QSR market.

Catalysts

About Sapphire Foods India- Owns and operates restaurants.

- The company's strategy to focus on value offers and core product innovations in KFC, combined with expanded day parts like late night and lunch, is expected to drive increases in customer frequency and broaden the consumer base, potentially boosting future revenue and profit margins.

- Accelerated store expansion, with plans to open 70-80 new KFC stores annually, along with rolling out digital kiosks for operational efficiency, is likely to enhance accessibility and customer experience, supporting sustained revenue growth and potentially improving earnings.

- Enhanced focus on the core variety menu offerings and strategic marketing campaigns like the Taste the Epic campaign for KFC are expected to re-engage infrequent and non-trial customers, potentially increasing frequency and size of transactions, impacting revenue positively.

- Improvements in operational excellence, such as maintaining high ratings on delivery platforms and implementing a dynamic kitchen planning tool, are set to increase product availability and reduce wastage, which can improve operational margins and net earnings.

- Strengthening performance in international markets like Sri Lanka, with strong double-digit SSSG and plans for new store openings, offers potential for significant revenue growth, contributing positively to consolidated earnings.

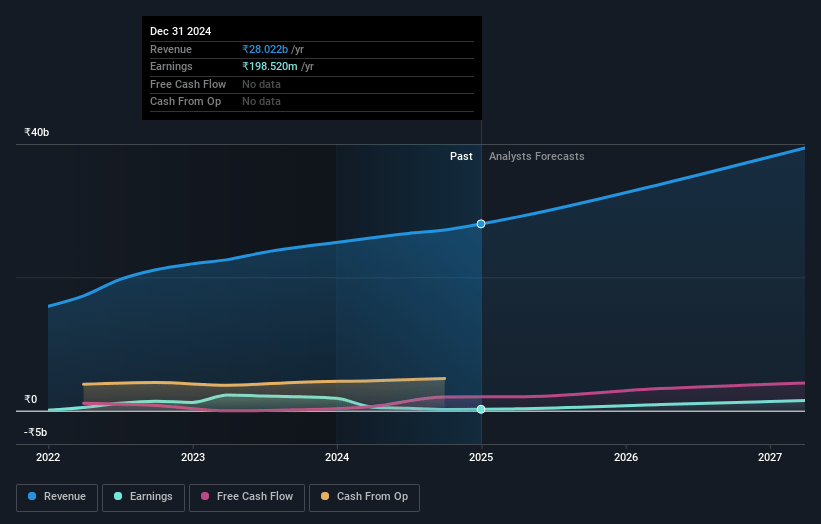

Sapphire Foods India Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Sapphire Foods India's revenue will grow by 14.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.7% today to 4.3% in 3 years time.

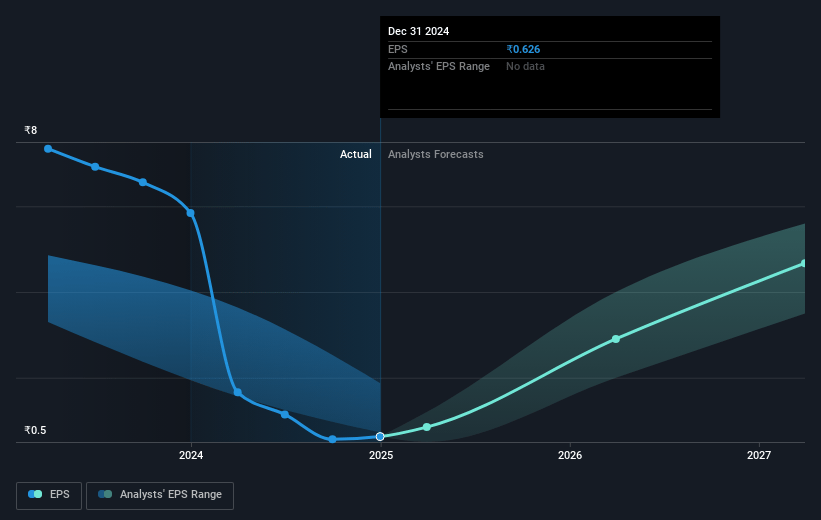

- Analysts expect earnings to reach ₹1.8 billion (and earnings per share of ₹7.69) by about March 2028, up from ₹198.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹2.1 billion in earnings, and the most bearish expecting ₹1.1 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 107.2x on those 2028 earnings, down from 493.7x today. This future PE is greater than the current PE for the IN Hospitality industry at 32.6x.

- Analysts expect the number of shares outstanding to grow by 1.69% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.29%, as per the Simply Wall St company report.

Sapphire Foods India Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The negative same-store sales growth (SSSG) for KFC, despite an improved trajectory, indicates ongoing challenges in consumer demand that could affect future revenue growth.

- Restaurant EBITDA margins are under pressure, with a noted drop in KFC margins, highlighting potential challenges in cost management and profitability.

- The closure of stores in the Maldives suggests potential difficulties in certain markets, presenting a risk of revenue loss and indicating challenges in maintaining consistent growth across all locations.

- The reliance on base effects to improve SSSG might provide only temporary relief, masking underlying challenges in achieving genuine sales growth, which can impact the sustainability of revenues.

- Competitive pressures in the QSR market could intensify with new entrants or improved offerings from existing competitors, impacting Sapphire Foods' market share and future earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹370.739 for Sapphire Foods India based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹425.0, and the most bearish reporting a price target of just ₹320.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹41.8 billion, earnings will come to ₹1.8 billion, and it would be trading on a PE ratio of 107.2x, assuming you use a discount rate of 15.3%.

- Given the current share price of ₹305.4, the analyst price target of ₹370.74 is 17.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.