Key Takeaways

- Strategic expansion through management and franchise deals and renovations is poised to enhance future revenue and earnings, emphasizing asset-light growth.

- The potential listing of Fleur Hotels is anticipated to reduce debt, strengthening finances and improving net margins.

- Ambitious expansion plans and renovations could strain finances and execution risks, while external market changes and cost pressures challenge long-term profitability goals.

Catalysts

About Lemon Tree Hotels- Owns and operates a chain of business and leisure hotels.

- Lemon Tree's strategic focus on expanding its management and franchise portfolio, with 13 new contracts adding 766 new rooms, suggests a future boost in revenue through asset-light growth.

- The redevelopment of the Orchid Hotel in Shillong under a PPP model, aimed to be operational within 2.5 to 3 years, is expected to benefit from capital subsidies and GST reimbursements, potentially improving net margins once operational.

- Ongoing and planned renovations of owned hotels, which will enhance ARR and occupancy, could have a more significant impact on future revenue and earnings after the completion by FY '27.

- The market demand for branded mid-market hotels in India is set to increase, which could facilitate higher occupancy rates and ARR, thus positively impacting RevPAR and overall earnings.

- The expectation of listing Fleur Hotels in the next 1.5 to 2 years, which could significantly reduce debt and strengthen balance sheets, leading to improved net margins and earnings.

Lemon Tree Hotels Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Lemon Tree Hotels's revenue will grow by 15.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 14.5% today to 25.8% in 3 years time.

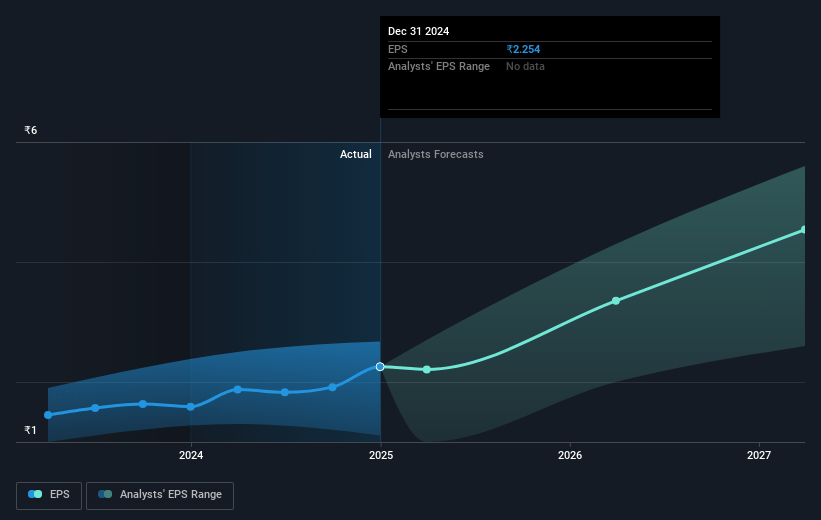

- Analysts expect earnings to reach ₹4.9 billion (and earnings per share of ₹5.71) by about May 2028, up from ₹1.8 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as ₹3.2 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 43.4x on those 2028 earnings, down from 60.6x today. This future PE is greater than the current PE for the IN Hospitality industry at 33.8x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.62%, as per the Simply Wall St company report.

Lemon Tree Hotels Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The ongoing renovations across the Lemon Tree portfolio, including a significant focus on the Keys Hotels, require substantial capital, which could impact net margins and EBITDA in the short term due to increased renovation expenses.

- The anticipated stabilization of Aurika Mumbai is projected for FY '26, suggesting current revenue and occupancy rates might take longer to reach optimal levels, affecting revenue projections for the interim period.

- The company's ambitious growth strategy of expanding to 20,000 rooms involves execution risks, including potential delays in project completions by asset owners, which could affect future revenue streams and earnings.

- Changes in market dynamics, such as the development of the Navi Mumbai Airport, could introduce competition that may temper ARR growth expectations at existing properties, impacting revenue and earnings forecasts.

- Lemon Tree's focus on achieving a 60% margin post-renovation and expansion might face challenges if input costs, particularly wages, rise faster than anticipated, which could compress net margins and affect long-term profitability targets.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹173.0 for Lemon Tree Hotels based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹210.0, and the most bearish reporting a price target of just ₹135.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹18.9 billion, earnings will come to ₹4.9 billion, and it would be trading on a PE ratio of 43.4x, assuming you use a discount rate of 15.6%.

- Given the current share price of ₹136.92, the analyst price target of ₹173.0 is 20.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.