Key Takeaways

- Strategic IKEA partnership and enhanced production capacity may boost revenue and margins by leveraging global retail presence and best practices.

- Diversifying into personal care and expanding retail footprint could increase revenue through growing online market and improved brand visibility.

- Stove Kraft faces challenges with declining demand, margin pressures from heavy discounting, and potential volatility in revenue due to shifts in product lines.

Catalysts

About Stove Kraft- Manufactures and trades in kitchen and home appliances in India and internationally.

- Stove Kraft's strategic partnership with IKEA to develop and supply cookware products represents a significant growth opportunity by leveraging IKEA's global retail presence, expected to impact revenue positively when it begins in FY '26.

- The dedicated 1.8 lakh square feet manufacturing facility for the IKEA partnership aims to enhance production capabilities, which may improve operational efficiencies and gross margins by aligning with global best practices.

- The cast iron foundry, fully commercialized with potential capacity expansion from 2.2 million to 4.4 million pieces per annum, could drive revenue growth and product diversification, catering to evolving consumer needs with high-quality cast iron products.

- Expansion into personal care products via e-commerce, including hair dryers and trimmers, diversifies Stove Kraft's portfolio and taps into a growing online market, potentially increasing revenue and offering higher-margin products.

- The ongoing retail expansion, with increased Pigeon brand stores and strategic marketing, strengthens brand visibility and channel mix diversity, facilitating long-term revenue growth and potentially stabilizing or improving net margins.

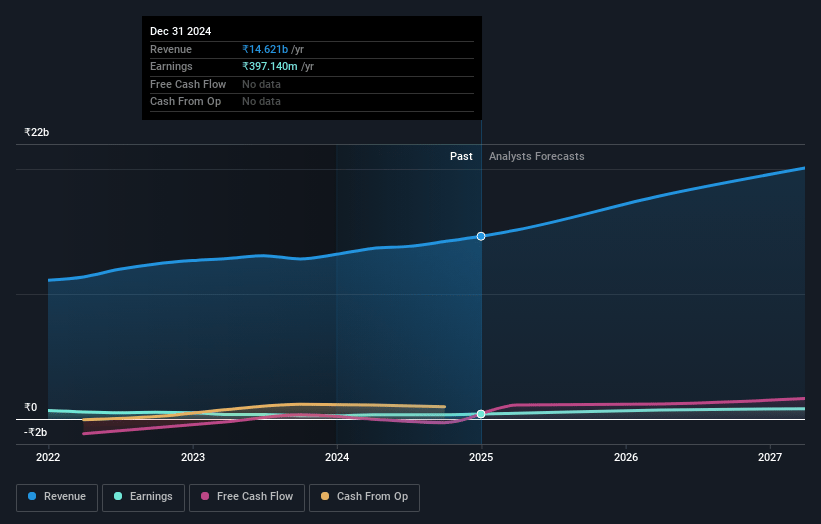

Stove Kraft Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Stove Kraft's revenue will grow by 15.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.7% today to 4.7% in 3 years time.

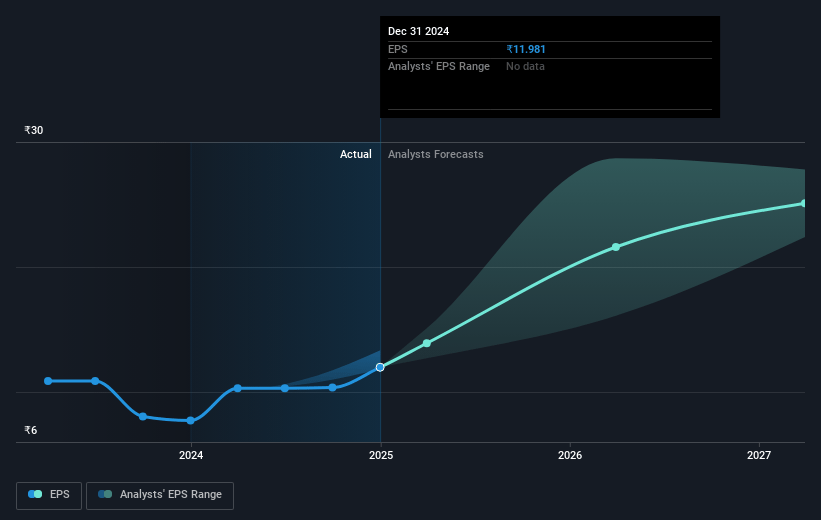

- Analysts expect earnings to reach ₹1.1 billion (and earnings per share of ₹32.05) by about May 2028, up from ₹397.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 52.4x on those 2028 earnings, up from 50.7x today. This future PE is greater than the current PE for the IN Consumer Durables industry at 42.9x.

- Analysts expect the number of shares outstanding to grow by 0.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.66%, as per the Simply Wall St company report.

Stove Kraft Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Stove Kraft acknowledges a relatively softer demand and consumer sentiment, with anticipated shortfalls in year-end revenue targets, which could impact revenue growth expectations.

- Concerns about a slight decline in gross margins due to extensive customer offers and discounts during December and January, which might affect overall net margins.

- Indications of pressure on achieving historical growth rates and EBITDA margins, with potential misses on the previously guided 11% EBITDA margin for FY '25, raising concerns regarding earnings projections.

- The shift in exports from PTFE to ceramic coatings caused temporary volume corrections, indicating potential volatility in revenue from changes in product lines or market preferences.

- Incremental costs such as increased interest and depreciation due to retail expansion may weigh on net earnings despite attempts to maintain operational efficiency.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹1085.0 for Stove Kraft based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹1200.0, and the most bearish reporting a price target of just ₹970.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹22.3 billion, earnings will come to ₹1.1 billion, and it would be trading on a PE ratio of 52.4x, assuming you use a discount rate of 15.7%.

- Given the current share price of ₹608.65, the analyst price target of ₹1085.0 is 43.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.