Key Takeaways

- Strategic expansion in retail and investment in AIoT solutions could bolster revenue and solidify market leadership in new sectors.

- Industry consolidation and ATM rate adjustments present opportunities for market share gains, potentially boosting revenue and margins.

- Delays in order execution and flat year-on-year revenue suggest potential growth challenges, with increased tech spend pressuring margins amidst industry disruptions.

Catalysts

About CMS Info Systems- Operates as a cash management company in India.

- CMS Info Systems is strategically expanding its retail segment, which has grown 15% year-to-date. This focus on retail can enhance revenues as the company regains market leadership in this sector.

- The company's investment in technology, specifically in AIoT remote monitoring solutions, marks its entry into non-BFSI sectors, potentially expanding its service and revenue base.

- The company’s emphasis on outsourcing contracts and project execution, notably the anticipated completion of 60% of the current order book by Q4, is expected to drive significant services revenue growth in FY '26, positively impacting revenue and earnings.

- The consolidation trends in the industry, coupled with instability at key competitors, offer CMS opportunities to gain market share, potentially boosting both revenue and margin profile as customers shift to stronger players.

- The expected increase in ATM interchange rates and the potential outsourcing of in-house ATMs by large PSU banks represent potential catalysts for growth in the cash logistics sector, which could enhance revenue and margins in the mid-term.

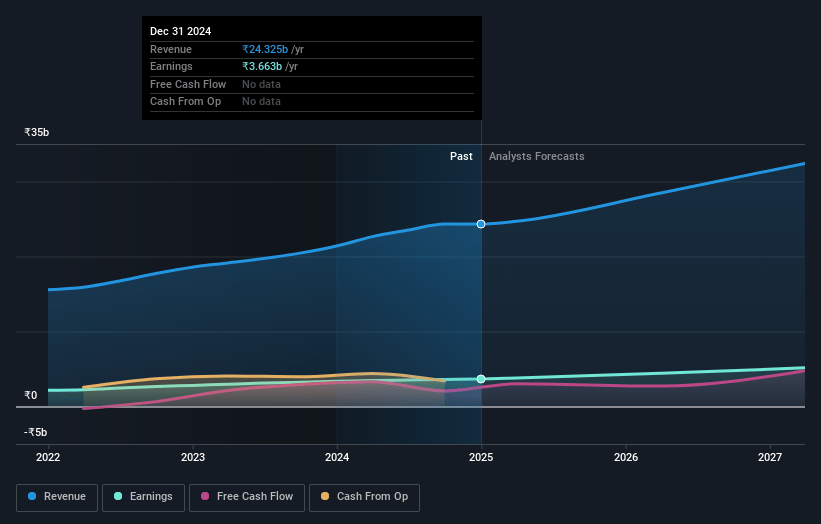

CMS Info Systems Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming CMS Info Systems's revenue will grow by 13.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 15.1% today to 16.1% in 3 years time.

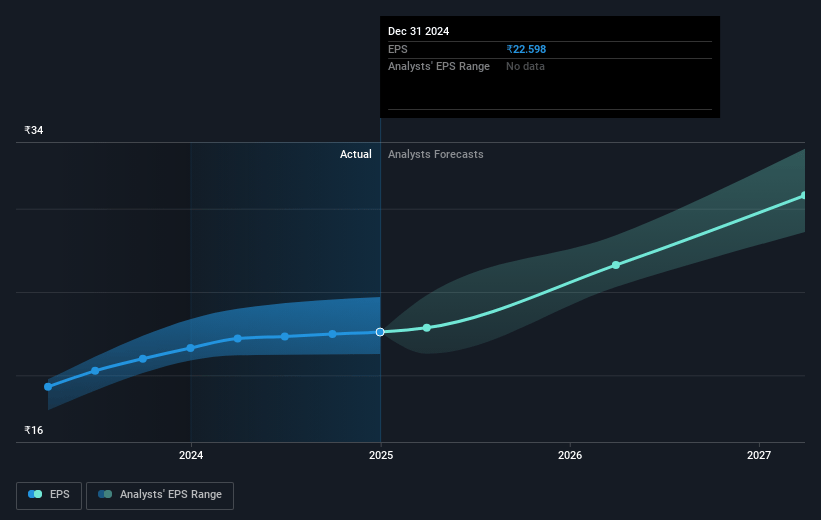

- Analysts expect earnings to reach ₹5.8 billion (and earnings per share of ₹34.08) by about May 2028, up from ₹3.7 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 24.7x on those 2028 earnings, up from 19.8x today. This future PE is greater than the current PE for the IN Commercial Services industry at 21.7x.

- Analysts expect the number of shares outstanding to grow by 0.8% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.08%, as per the Simply Wall St company report.

CMS Info Systems Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- CMS Info Systems experienced a slip in revenue from unexpected delays in large order book execution, leading to ₹150 crores lower revenue in FY '25. This delay in converting order wins to revenue impacts earnings and cash flow.

- The Managed Services and Technology Solutions business saw a decline of around 10% due to lower banking automation revenue, signaling potential instability in recurring revenues or demand in this segment, affecting overall net margins.

- Industry disruption, caused by issues at a key competitor, is creating operational distractions that might delay CMS Info Systems' order book execution and customer onboarding, affecting short-term revenue growth.

- Despite a 10% revenue growth reported, the company's total revenue on a year-on-year basis was flat, indicating a possible stagnation in revenue streams that could influence future growth expectations and investor confidence.

- CMS Info Systems has increased its tech spends marginally from 1% to 1.5% of revenue, which may pressure net margins if expected gains in efficiency and margin profile do not materialize quickly enough.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹584.5 for CMS Info Systems based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹35.6 billion, earnings will come to ₹5.8 billion, and it would be trading on a PE ratio of 24.7x, assuming you use a discount rate of 13.1%.

- Given the current share price of ₹441.55, the analyst price target of ₹584.5 is 24.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.