Key Takeaways

- Increased graphite electrode demand from new electric arc furnaces could boost HEG's revenue and market position.

- Planned diversification into electric vehicle anodes and strategic investments may enhance earnings and shareholder value through high-growth sectors and competitive advantages.

- Declining steel production, price pressures, and oversupply of Chinese electrodes threaten HEG's revenue and profit margins.

Catalysts

About HEG- Manufactures and sells graphite electrodes in India and internationally.

- HEG Limited expects an increase in demand for graphite electrodes due to the construction of new electric arc furnaces worldwide, which can positively impact future revenues as electrode consumption rises with more steel being produced through this method.

- The company's strategic investment in GrafTech, a major competitor with backward integration into needle coke production, suggests potential for financial gains if electrode prices increase, thus potentially impacting future earnings positively.

- HEG's planned anode production plant intends to capitalize on the growing demand for electric vehicle batteries, potentially increasing future revenue through diversification into high-growth segments.

- The ongoing demerger process is intended to unlock value for shareholders by separating the graphite and green technology businesses, which could positively impact future earnings per share and shareholder value.

- As the lowest-cost producer in the world, HEG could benefit from improving industry conditions and potential price increases, enhancing future net margins if electrode prices stabilize or rise due to industry capacity dynamics.

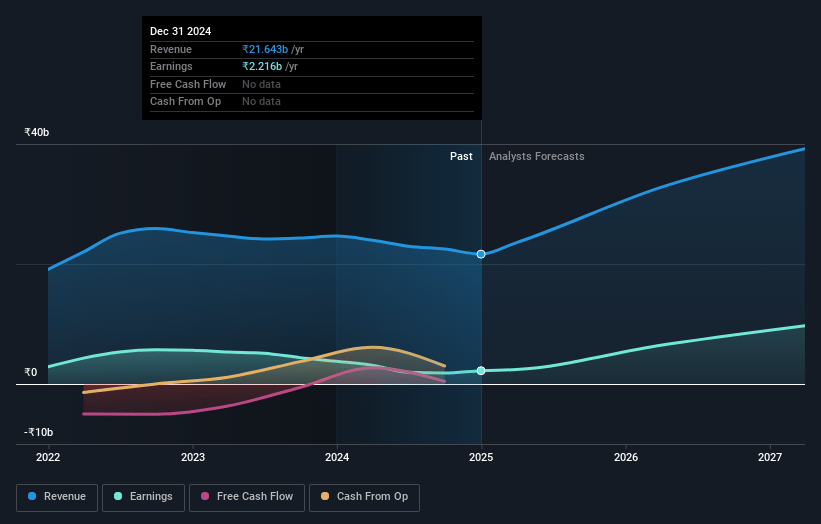

HEG Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming HEG's revenue will grow by 31.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.2% today to 31.8% in 3 years time.

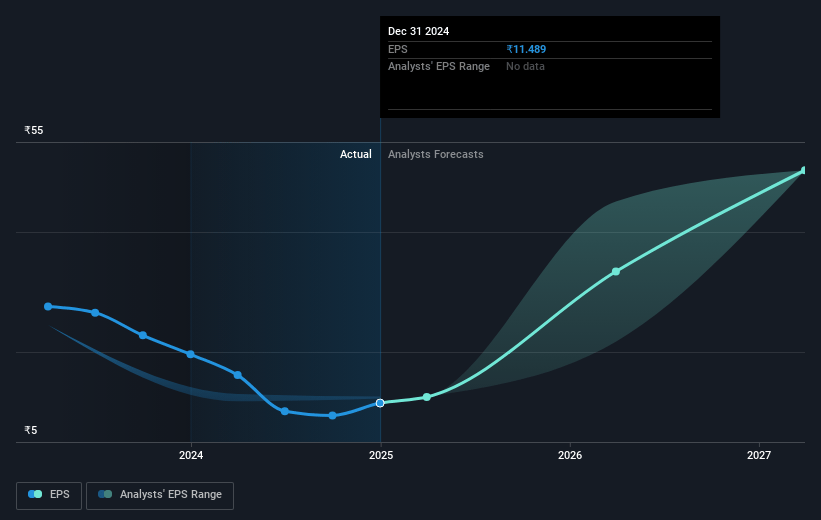

- Analysts expect earnings to reach ₹15.5 billion (and earnings per share of ₹80.52) by about April 2028, up from ₹2.2 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 8.7x on those 2028 earnings, down from 41.2x today. This future PE is lower than the current PE for the IN Electrical industry at 39.1x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 16.08%, as per the Simply Wall St company report.

HEG Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The decline in global crude steel production, especially in major regions like the U.S., Japan, and Korea, could negatively impact the demand for graphite electrodes, affecting HEG's revenue prospects.

- The pressure on electrode pricing due to subdued demand, coupled with the stable needle coke prices, may narrow profit spreads and negatively impact HEG's net margins.

- Uncertainties surrounding the successful implementation of the announced price hikes by global competitors might affect HEG's competitive pricing strategy and revenue stability.

- Potential reciprocal tariffs on exports to the U.S. could reduce HEG’s competitive positioning and compress margins, impacting overall earnings.

- The oversupply of Chinese electrodes in the market resulting from stalled shifts to electric arc furnace production in China may contribute to price declines, adversely impacting HEG's revenue potential.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹450.0 for HEG based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹48.8 billion, earnings will come to ₹15.5 billion, and it would be trading on a PE ratio of 8.7x, assuming you use a discount rate of 16.1%.

- Given the current share price of ₹473.75, the analyst price target of ₹450.0 is 5.3% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.