Key Takeaways

- Strategic product launches and inventory management are expected to enhance market penetration and improve net margins by increasing dealer profitability.

- Integration with Kubota could drive growth in exports and market share, improving revenue and operating margins through scale efficiencies.

- Challenges in market share, profitability, emission norms, and expansion may impact Escorts Kubota's revenue growth and margins if not addressed effectively.

Catalysts

About Escorts Kubota- Manufactures and sells agri machinery, construction equipment, and railway equipment in India and internationally.

- The launch of the PROMAXX series under the Farmtrac brand is expected to expand the product offerings, potentially increasing revenue through enhanced market penetration, especially in previously underrepresented regions like the Western market.

- The strategic move to reduce channel inventory and rationalize stock levels is aimed at enhancing dealer profitability and operational efficiency, which could improve net margins by reducing carrying costs and enhancing fiscal discipline.

- The development and introduction of the new entry-level Hydra cranes and BLX 75 backhoe loader products, in compliance with Stage 5 emission standards, demonstrate a forward-looking approach that could capture market demand and boost revenue in the Construction Equipment segment.

- The anticipated consolidation and relaunch of certain products following the Kubota integration, including leveraging a captive finance initiative, could increase market share, thereby increasing revenue and potentially improving net earnings.

- Integration with Kubota's global network, especially the renewed focus on export to markets like Europe, is expected to drive high double-digit growth in export volumes, potentially boosting overall revenue and improving operating margins due to scale efficiencies.

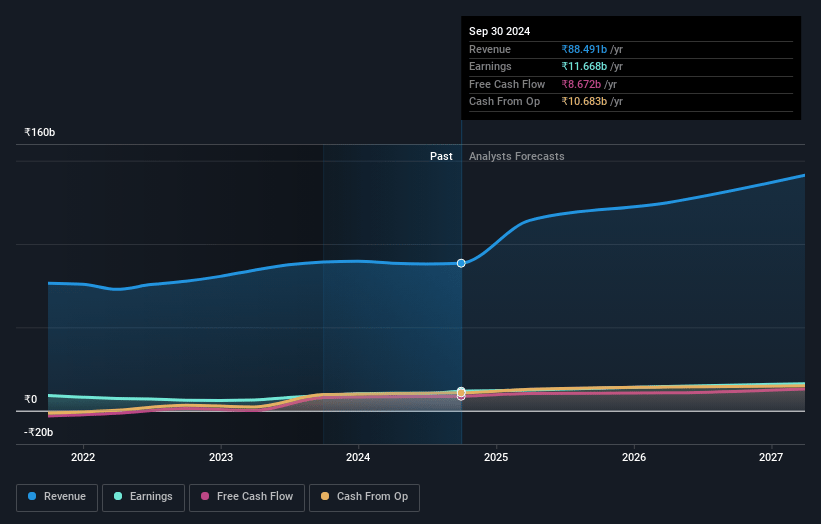

Escorts Kubota Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Escorts Kubota's revenue will grow by 16.3% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 13.1% today to 10.3% in 3 years time.

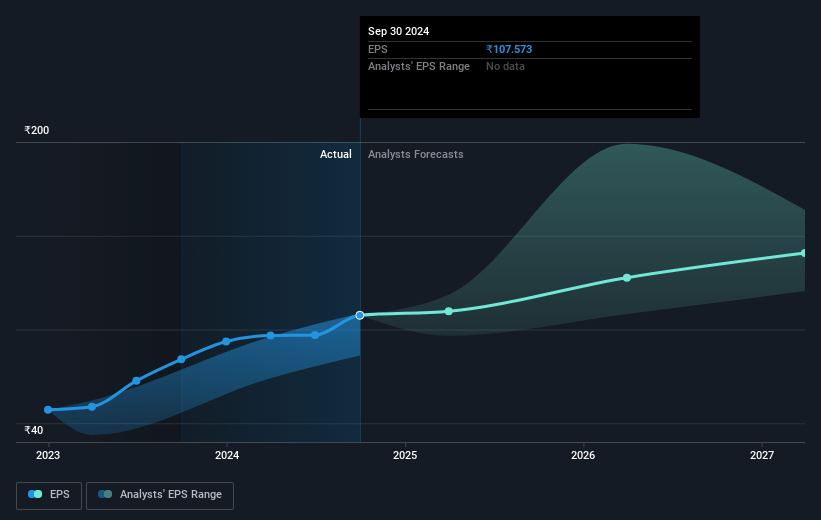

- Analysts expect earnings to reach ₹14.9 billion (and earnings per share of ₹132.64) by about May 2028, up from ₹12.0 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹17.6 billion in earnings, and the most bearish expecting ₹12.9 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 37.1x on those 2028 earnings, up from 30.0x today. This future PE is greater than the current PE for the IN Machinery industry at 30.7x.

- Analysts expect the number of shares outstanding to decline by 0.49% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.23%, as per the Simply Wall St company report.

Escorts Kubota Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's market share in the domestic tractor industry has been lagging, particularly in opportunity markets like South India, Andhra Pradesh, Telangana, and others, which may impact revenue growth and market positioning.

- Despite growth in the Agri Machinery segment, EBIT margins declined to 10.4% from 12.1% due to factors like lower profitability in the non-tractor segment and the impact of inventory correction, which could affect overall profitability.

- The transition to higher emission norms in the Construction Equipment business may result in temporary volume impacts and challenges in passing on cost increases, potentially affecting revenue and margins.

- Inventory buildup in previous quarters and a need for rationalization to ensure dealer profitability may create temporary impacts on revenue recognition and financial stability.

- Delays in the acquisition of land for a new Greenfield plant might impact the company's ability to expand manufacturing capabilities and increase production efficiency, which could affect revenue growth and operating margins if not resolved in a timely manner.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹3331.85 for Escorts Kubota based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹3980.0, and the most bearish reporting a price target of just ₹2533.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹143.7 billion, earnings will come to ₹14.9 billion, and it would be trading on a PE ratio of 37.1x, assuming you use a discount rate of 15.2%.

- Given the current share price of ₹3259.0, the analyst price target of ₹3331.85 is 2.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.