Key Takeaways

- Diversification into infrastructure, metallurgy, and green energy sectors could enhance future revenue and margin expansion.

- International focus, particularly in the Middle East, offers growth in foreign revenue through new consultancy contracts.

- Heavy reliance on a few large projects and low-margin Turnkey projects, along with geopolitical and sector-specific risks, may affect revenue consistency and growth.

Catalysts

About Engineers India- An engineering consultancy company, provides design, engineering, procurement, construction, and integrated project management services for oil, gas, fertilizers, steel, railways, power, infrastructure, and petrochemical industries worldwide.

- Engineers India has an all-time high order book of ₹11,353 crores, indicating robust future revenue streams and potential top-line growth.

- The company is L1 for major IOCL Paradip packages, suggesting forthcoming project awards and subsequent revenue recognition in subsequent quarters.

- Expansion into new sectors such as infrastructure, metallurgy, coal gasification, and green energy could diversify its portfolio and support future revenue enhancement and margin expansion.

- International expansion, with a focus on the Middle East and potential new consultancy contracts, could enhance foreign revenue streams, supporting overall revenue growth.

- Ongoing discussions and potential future projects in sectors like oil to chemical transformation and petrochemical complexes can offer substantial consulting and execution opportunities, potentially improving revenue and operating margins.

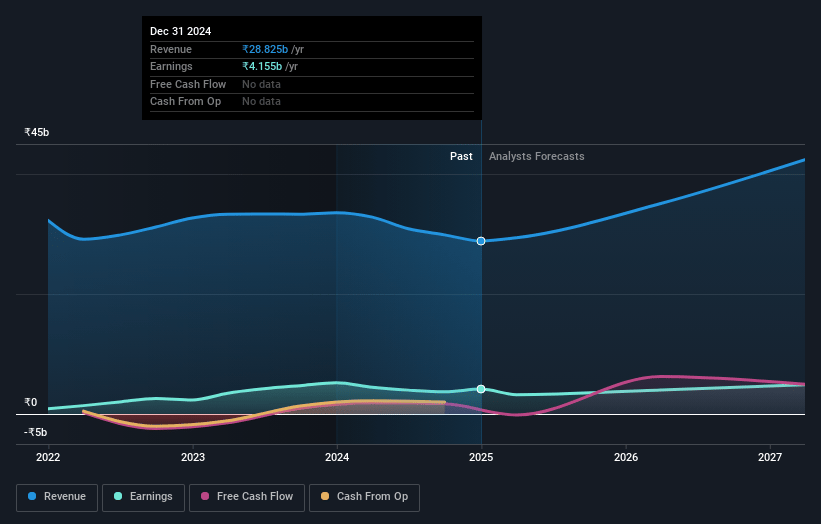

Engineers India Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Engineers India's revenue will grow by 18.5% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 14.4% today to 10.9% in 3 years time.

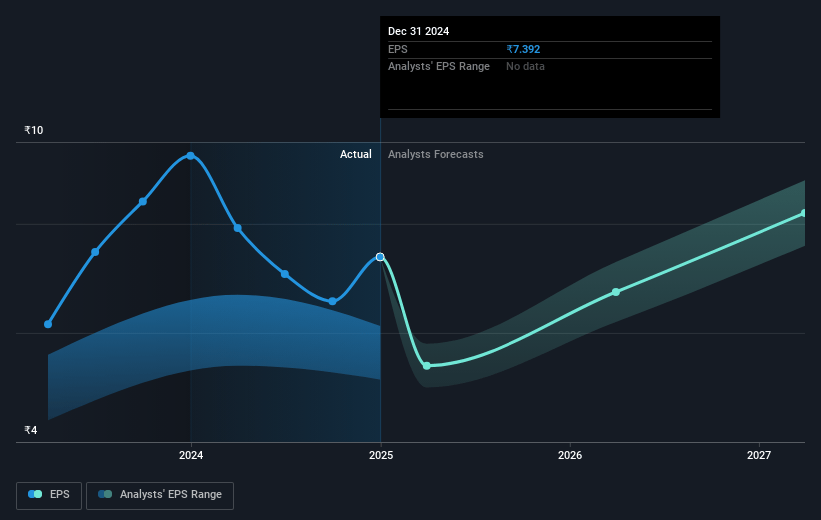

- Analysts expect earnings to reach ₹5.2 billion (and earnings per share of ₹8.64) by about May 2028, up from ₹4.2 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 34.2x on those 2028 earnings, up from 24.2x today. This future PE is greater than the current PE for the IN Construction industry at 21.1x.

- Analysts expect the number of shares outstanding to decline by 0.28% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.03%, as per the Simply Wall St company report.

Engineers India Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- There is significant reliance on large-scale projects from government sectors and specific private-sector clients, which may introduce cyclicality and dependency on a limited number of projects. This could impact revenue consistency if any major projects are delayed or canceled.

- The company's operating profit margins in the Turnkey segment are notably lower (5-6%) compared to the Consultancy segment (around 20%), and an increased proportion of Turnkey projects in the order book could adversely affect overall net margins.

- External factors such as land acquisition issues, as seen with the CPCL Nagapattinam project being on hold, could delay project executions and revenue recognition, impacting earnings and financial forecasts.

- The international market performance is heavily reliant on competitive bidding and geopolitical conditions in regions like the Middle East. The company's growth in international markets might face stiff competition, affecting potential earnings from these regions.

- The investment in specific sectors such as refineries and petrochemicals carries inherent risks, including fluctuating demand and prices in the oil and gas industry, which could impact revenue predictions and the feasibility of ongoing and future projects.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹216.667 for Engineers India based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹242.0, and the most bearish reporting a price target of just ₹190.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹47.9 billion, earnings will come to ₹5.2 billion, and it would be trading on a PE ratio of 34.2x, assuming you use a discount rate of 14.0%.

- Given the current share price of ₹178.65, the analyst price target of ₹216.67 is 17.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.