Key Takeaways

- Revolutionary compressor stabilizer technology and low-cost models are set to increase sales, market share, and revenue through unique value and underserved market segments.

- Strategic geographic focus and enhanced distribution and service networks aim to boost market penetration, customer retention, and long-term profitability without significant cost burdens.

- Intense competition, cost challenges, and regional sluggishness threaten Elgi Equipments' revenue and profitability unless strategic market improvements and product successes counteract these pressures.

Catalysts

About Elgi Equipments- Manufactures and sells air compressors and related parts in India, Europe, Australia, the United States, and internationally.

- The introduction of the revolutionary compressor stabilizer technology, which offers significant energy savings and improved reliability at a fraction of the cost of existing solutions like VFDs, is expected to drive increased sales and market share. This innovation is likely to positively impact the company's revenue and net margins by offering a unique value proposition.

- The development and upcoming launch of low-cost compressor models to compete with Chinese imports positions the company to capture a significant share of the low-end market. This strategy aims to grow revenue by tapping into a previously underserved segment while maintaining quality and performance standards.

- Strategic geographic focus on key markets such as the U.S., Europe, and Southeast Asia, alongside targeted expansion plans, is designed to capture growth opportunities and increase market penetration. Growth in these regions is expected to bolster revenue and support long-term profitability.

- Enhancements in distribution networks and after-sales service capabilities are likely to improve customer retention and satisfaction, driving revenue growth from both new sales and aftermarket service contracts, which are generally higher margin.

- The company's strong cash position and effective working capital management, leading to reduced interest expenses, position Elgi Equipments to invest in growth initiatives without significant cost burdens. This will support improved net margins and earnings growth.

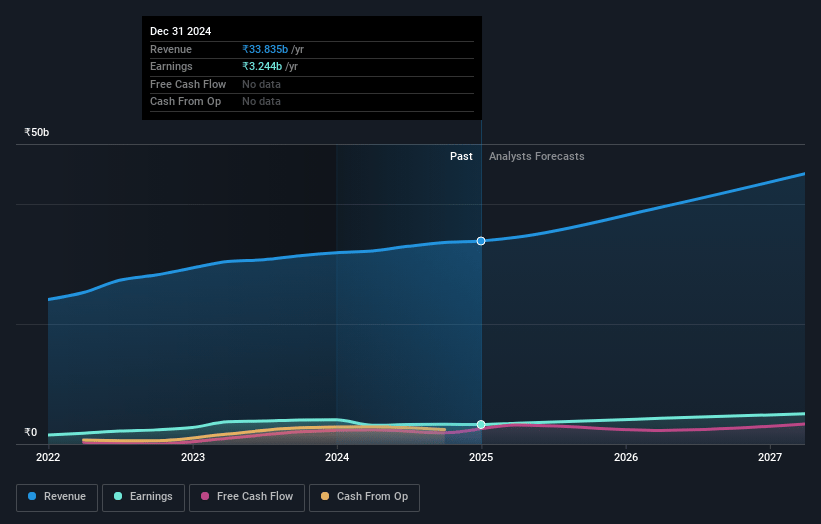

Elgi Equipments Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Elgi Equipments's revenue will grow by 10.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.6% today to 10.2% in 3 years time.

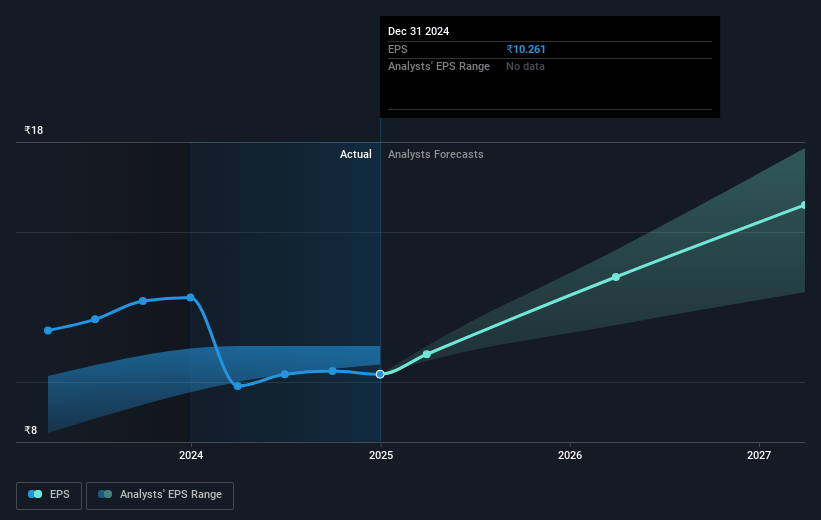

- Analysts expect earnings to reach ₹4.7 billion (and earnings per share of ₹14.74) by about May 2028, up from ₹3.2 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹5.6 billion in earnings, and the most bearish expecting ₹4.1 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 59.1x on those 2028 earnings, up from 43.4x today. This future PE is greater than the current PE for the IN Machinery industry at 30.7x.

- Analysts expect the number of shares outstanding to grow by 0.05% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.04%, as per the Simply Wall St company report.

Elgi Equipments Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's performance in Q3 was affected by a significant increase in fixed costs, transport costs, and warranty provisioning. These onetime issues reduced profitability and could impact earnings if similar costs recur unexpectedly.

- Revenue growth has been constrained by external factors, such as the GST portal issues and sluggish performance in the portable business across key markets like the U.S., Europe, and Australia, which could lead to continued revenue volatility.

- The slowdown in specific sectors and regions, including North America's portable business and sluggish markets in Australia, poses a risk to future revenue and earnings growth if economic conditions do not improve.

- Intense competition from low-cost Chinese imports, especially in the lower-tier compressor market, could pressure margins and market share, affecting profitability unless the company successfully leverages its new product offerings to counteract this threat.

- The European and U.S. operations are currently only achieving breakeven, highlighting a risk that sustained profitability in these regions may not be realized if market conditions do not improve or if the company's strategies in these areas do not yield the expected results.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹588.25 for Elgi Equipments based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹710.0, and the most bearish reporting a price target of just ₹436.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹45.8 billion, earnings will come to ₹4.7 billion, and it would be trading on a PE ratio of 59.1x, assuming you use a discount rate of 14.0%.

- Given the current share price of ₹445.45, the analyst price target of ₹588.25 is 24.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.