Key Takeaways

- Record order book and international demand in renewable energy suggest potential revenue growth from new markets and applications.

- Diversification in products, digital integration, and strategic collaborations may enhance margins and earnings through innovation and efficiency.

- High capital expenditure and subdued domestic demand risk pressuring Triveni Turbine's earnings and margins without compensatory growth in other segments.

Catalysts

About Triveni Turbine- Manufactures and supplies power generating equipment and solutions in India and internationally.

- Triveni Turbine has reported a record closing order book, with substantial international demand, specifically in renewable energy segments, indicating potential revenue growth from new geographies and applications.

- The company is focused on diversifying its product offerings and improving internal efficiencies through investments in technology and R&D, which can enhance net margins by expanding into higher value-added segments.

- The introduction of a CO2-based energy storage system, along with a strategic collaboration for its development, opens up a new revenue stream, potentially impacting earnings positively if cost parity with lithium-ion is achieved.

- Strong growth in the Aftermarket segment, particularly through providing upgrades to existing clients and expanding into third-party refurbishment services, suggests an avenue for increased revenues and improved net margins.

- Triveni Turbine's commitment to integrating digital technologies, coupled with alliances with global experts, is likely to fuel sustainable long-term growth, potentially boosting earnings through innovative service offerings.

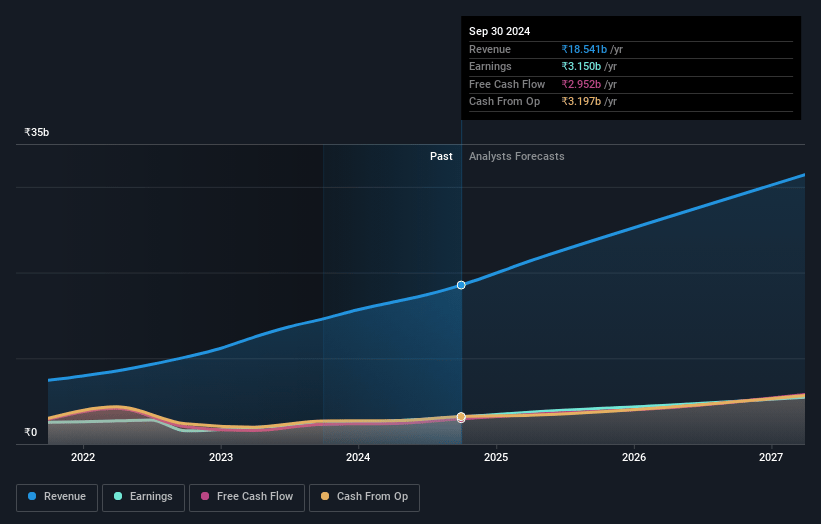

Triveni Turbine Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Triveni Turbine's revenue will grow by 17.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 17.6% today to 17.5% in 3 years time.

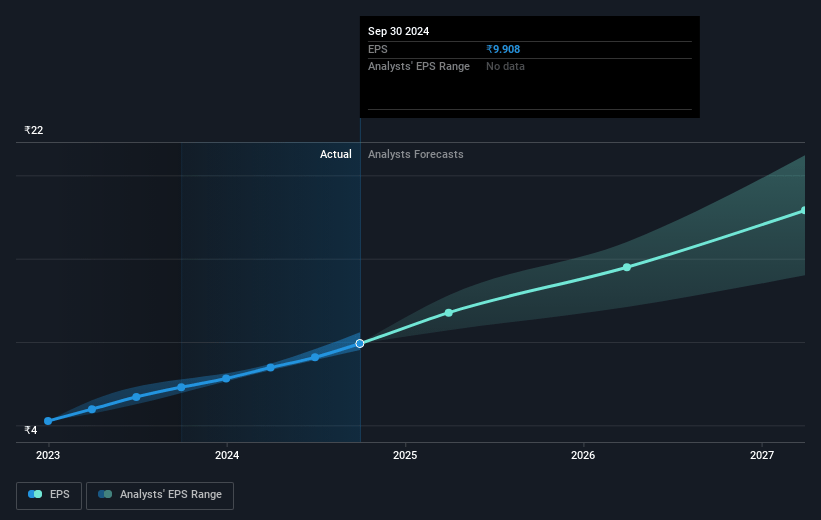

- Analysts expect earnings to reach ₹5.5 billion (and earnings per share of ₹17.16) by about April 2028, up from ₹3.4 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹6.7 billion in earnings, and the most bearish expecting ₹4.3 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 64.5x on those 2028 earnings, up from 48.1x today. This future PE is greater than the current PE for the IN Electrical industry at 38.2x.

- Analysts expect the number of shares outstanding to decline by 0.45% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.69%, as per the Simply Wall St company report.

Triveni Turbine Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Order bookings from India have remained subdued, with only a modest increase in international demand. This reflects potential risks in the domestic market that could impact Triveni Turbine's revenue growth prospects.

- The company is facing a decline in the Aftermarket order bookings, which was down 17% year-over-year, potentially affecting net margins if this trend continues without offsetting gains elsewhere.

- Triveni Turbine is investing heavily in the CO2-based energy storage system, but the initial profitability of these orders is not high, which could pressure earnings if other segments don't perform as expected.

- The company plans significant capital expenditure to expand R&D capabilities and build capacities, which, if not managed well, could impact net margins and earnings due to increased costs.

- The U.S. market entry has led to additional costs, resulting in an anticipated ₹20 crores loss, which could pressure net profit margins if the market does not mature quickly enough.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹744.444 for Triveni Turbine based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹900.0, and the most bearish reporting a price target of just ₹610.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹31.2 billion, earnings will come to ₹5.5 billion, and it would be trading on a PE ratio of 64.5x, assuming you use a discount rate of 14.7%.

- Given the current share price of ₹513.1, the analyst price target of ₹744.44 is 31.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.