Key Takeaways

- Expansion into high-demand regions and value-added products is expected to enhance margins and capitalize on global infrastructure and energy trends.

- Strong export-focused order book and supportive government policies position the company for sustained, multi-year growth in revenue and profitability.

- Major expansion and market dependence introduce elevated operational, geopolitical, and demand risks, potentially destabilizing revenue, margins, and overall financial predictability.

Catalysts

About Man Industries (India)- Manufactures, processes, and trades in submerged arc welded pipes and steel products in India.

- Significant capacity expansions in both Saudi Arabia and Jammu are expected to go live within FY '26; with Saudi operations strategically positioned to address strong under-supplied demand in the Middle East, this will likely drive a step-change in revenue and improve margins due to proximity to core demand centers.

- Robust order book (₹3,200 crores) and pipeline (₹15,000 crores in bids) with a high export component (80%) provide strong revenue visibility and position the company to capitalize on global infrastructure and energy investment trends, supporting sustained top-line and order inflow growth.

- Growing demand for oil, gas, and water pipeline infrastructure-particularly in MENA and Southeast Asia, where Man Industries is securing higher-margin export projects-leverages the global push for energy security and urbanization, which should enhance both revenue and margins.

- Diversification into higher-margin value-added products (such as coated and offshore pipeline segments) and targeted shift toward markets with better pricing (supported by product/geographic mix) are expected to further support continued EBITDA and net margin expansion.

- Government policy support in India (via Make in India, GST incentives for Jammu, and subsidies/interest subvention schemes) and the long-term global focus on clean energy transition pipelines will reduce domestic competition, lower operational costs, and provide a foundation for multi-year EPS and margin growth.

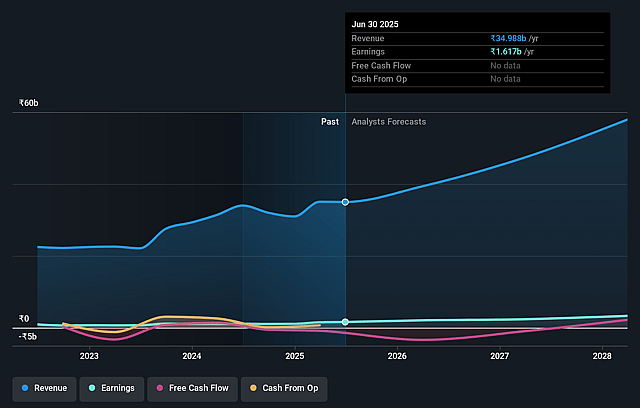

Man Industries (India) Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Man Industries (India)'s revenue will grow by 19.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.6% today to 5.5% in 3 years time.

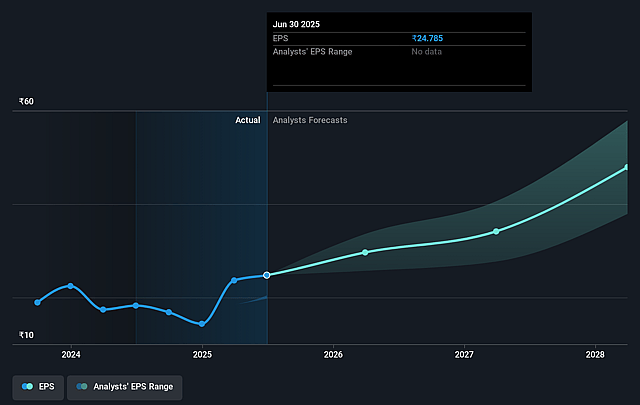

- Analysts expect earnings to reach ₹3.3 billion (and earnings per share of ₹44.44) by about August 2028, up from ₹1.6 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹3.9 billion in earnings, and the most bearish expecting ₹2.8 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.0x on those 2028 earnings, down from 18.2x today. This future PE is lower than the current PE for the IN Construction industry at 20.5x.

- Analysts expect the number of shares outstanding to grow by 3.27% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.55%, as per the Simply Wall St company report.

Man Industries (India) Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Large-scale expansion in Saudi Arabia and Jammu involves significant capital expenditure (₹1,200 crores total, with 630 crores in Saudi and 570 crores in Jammu), introducing heightened execution and ramp-up risk; delays, cost overruns, or underutilization could compress return on capital and adversely affect net margins and earnings.

- Increased domestic and international competition (including new plants by Welspun and Jindal in Saudi Arabia) risks oversupply in core markets such as MENA, potentially pressuring sales prices and operational margins, with direct negative effects on revenue growth and profitability.

- Continued reliance on oil & gas pipeline projects (80% exports, primarily in API segment) exposes Man Industries to any accelerated global shift from fossil fuels or slowdown in oil & gas capital expenditure, which could significantly depress long-term order inflows and revenue.

- Exposure to geopolitical disruptions (e.g., recent Iran-Israel and India-Pakistan tensions) can lead to export shipment delays and logistical bottlenecks, impacting short-term cash flows and increasing volatility of quarterly revenue recognition.

- Significant real estate income recognition and cash flows (up to ₹700–800 crores) are market-driven, and any slowdown in local property demand or delays in project launches could create unpredictability in revenue and profit contribution from this segment.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹465.0 for Man Industries (India) based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹59.3 billion, earnings will come to ₹3.3 billion, and it would be trading on a PE ratio of 18.0x, assuming you use a discount rate of 15.6%.

- Given the current share price of ₹391.75, the analyst price target of ₹465.0 is 15.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.