Key Takeaways

- Growth in Learning through digital sales and curriculum expansion, especially in Poland, Netherlands, and Spain, is projected to boost future revenues and EBIT.

- Program Solar and balance sheet deleveraging are set to enhance free cash flow, improve margins, and reduce interest burdens, benefiting operational and net earnings.

- Declines in advertising and reliance on seasonal factors, alongside uncertain macroeconomic conditions, threaten Sanoma Oyj's revenue stability and margin improvement efforts.

Catalysts

About Sanoma Oyj- Operates as a media and learning company in Finland, the Netherlands, Poland, Spain, Belgium, and internationally.

- Growth in the Learning segment, especially in the Netherlands and Poland through digital sales and early orders, is expected to drive future increases in both revenue and operational EBIT.

- Program Solar initiatives aimed at cost reduction and efficiency improvements are anticipated to continue enhancing free cash flow and improving operating margins as they are fully realized by 2026.

- Ongoing deleveraging of the balance sheet, reflected in a reduction of net debt and interest expenses, is set to improve net earnings by decreasing interest burdens over time.

- The pivot in Media Finland towards digital subscription sales, as seen in Ruutu+, is expected to compensate for declines in traditional advertising revenues, thus supporting stable, if not improved, operational EBIT.

- The planned expansions in Learning markets, with expected curriculum growth post-2025, especially in Spain, position the company for future revenue boosts as new content cycles create demand.

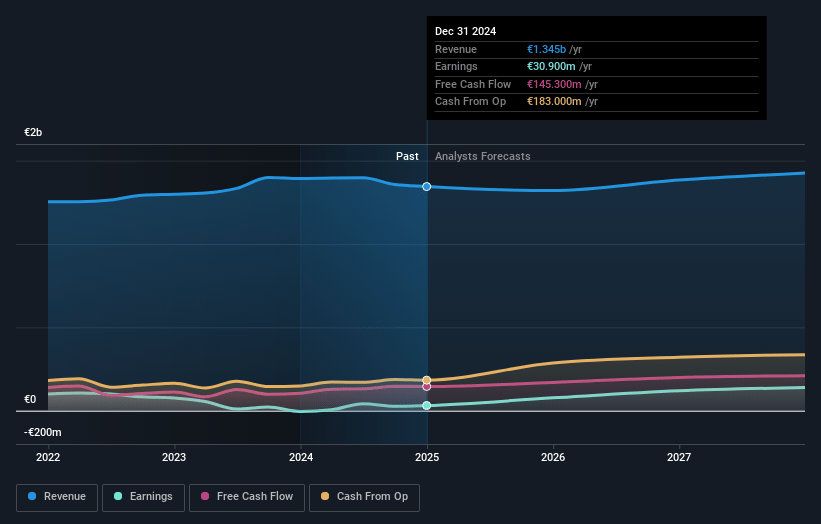

Sanoma Oyj Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Sanoma Oyj's revenue will grow by 2.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.2% today to 9.3% in 3 years time.

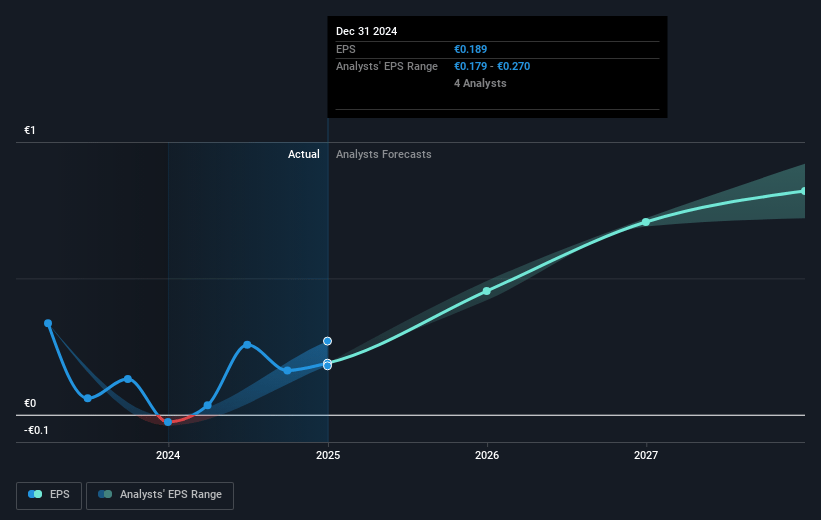

- Analysts expect earnings to reach €133.2 million (and earnings per share of €0.81) by about May 2028, up from €30.1 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as €151.1 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.6x on those 2028 earnings, down from 52.4x today. This future PE is lower than the current PE for the GB Media industry at 17.8x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.12%, as per the Simply Wall St company report.

Sanoma Oyj Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The decrease in advertising sales, particularly in TV, print, and radio, could negatively impact the revenue adversely affecting overall financial performance in the media segment.

- The reliance on seasonal performance and the potential for customer ordering delays in the Learning segment pose risks to revenue consistency, which could impact earnings predictability.

- The uncertain Finnish macroeconomic environment and its potential prolonged weakness may continue to suppress consumer spending, thereby affecting Media Finland's revenue growth and net margins.

- Program Solar's savings impact might take longer to be fully realized and could be less effective in driving immediate margin improvements and cost efficiency, thereby impacting net margins in the short term.

- A decline in third-party TV advertising contracts could result in significant adverse impacts on revenue and net profitability in 2025, given their historical contribution to overall financials.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €10.767 for Sanoma Oyj based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €1.4 billion, earnings will come to €133.2 million, and it would be trading on a PE ratio of 12.6x, assuming you use a discount rate of 6.1%.

- Given the current share price of €9.69, the analyst price target of €10.77 is 10.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.