Key Takeaways

- Expanding water solutions and bio-based material partnerships position the company to benefit from global sustainability trends and tighter regulations.

- Profitability initiatives, digitalization, and geographic diversification support margin improvement and stable long-term growth prospects.

- Weak end-markets, profitability challenges, and currency volatility threaten Kemira's earnings and growth, while mature industries, competition, and cash flow constraints risk long-term market relevance.

Catalysts

About Kemira Oyj- Operates as a chemicals company in Finland, rest of Europe, the Middle East, Africa, the Americas, and the Asia Pacific.

- Kemira's core Water Solutions business remains resilient and benefits from increasing global demand for clean water and tightening water treatment regulations; ongoing investments and strategic capacity expansions (including innovation partnerships for AI-based material development) are poised to support top-line revenue growth and margin resilience as these regulatory trends strengthen globally.

- The company is actively participating in the shift toward renewable and recycled packaging materials, demonstrated by R&D partnerships (e.g., with Bluepha and Metsä Group) to commercialize fully bio-based materials; this positions Kemira to gain share as ESG and sustainability priorities accelerate, offering future revenue and margin tailwinds as customers seek greener alternatives.

- Execution of a broad profitability improvement program in the Packaging & Hygiene Solutions segment-especially in APAC, where margins are weakest-is expected to deliver significant EBITDA and net margin improvement over the next year through cost base reductions and targeted volume recovery.

- Maintenance of a strong balance sheet and launch of a sizable share buyback program highlight substantial capital allocation flexibility, enabling continued investment in organic and inorganic growth-supporting higher prospective EPS and return on equity as M&A and capacity expansions are executed.

- Strengthening Kemira's presence in high-growth regions (such as North America and select emerging markets), along with ongoing digitalization and value-added specialty chemical innovation, provides a structural platform for stable long-term revenue growth and improvement in earnings quality.

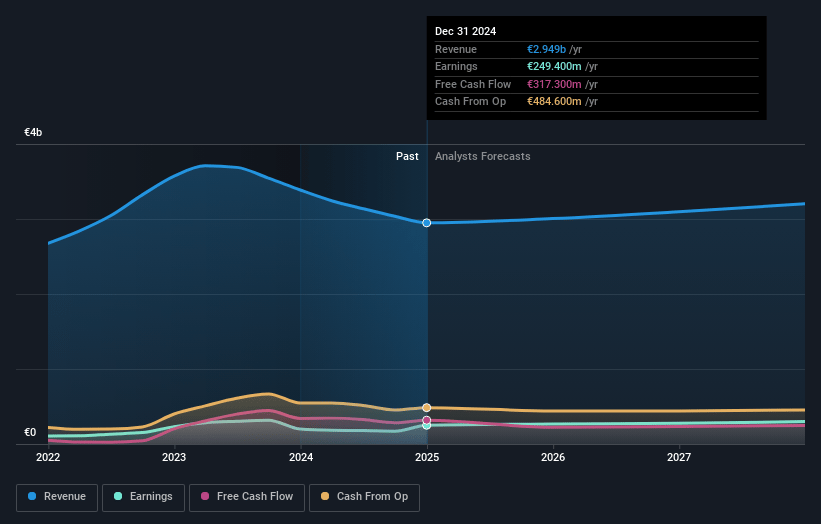

Kemira Oyj Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Kemira Oyj's revenue will grow by 1.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.9% today to 8.8% in 3 years time.

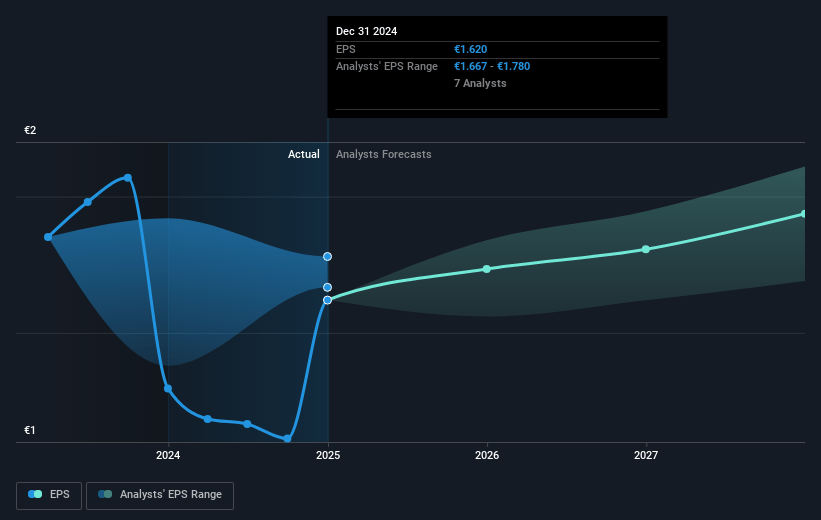

- Analysts expect earnings to reach €262.8 million (and earnings per share of €1.69) by about July 2028, up from €224.5 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as €305 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 16.7x on those 2028 earnings, up from 13.3x today. This future PE is greater than the current PE for the GB Chemicals industry at 12.8x.

- Analysts expect the number of shares outstanding to grow by 0.3% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.55%, as per the Simply Wall St company report.

Kemira Oyj Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Kemira's revenue and organic growth are under sustained pressure from structurally weak end-markets such as Packaging & Hygiene Solutions (PHS) and softness in the pulp industry-suggesting that mature industries and digitalization trends could continue to constrain long-term revenue and volume growth.

- Persistent profitability challenges and negative organic growth in PHS, especially in APAC, highlight Kemira's high fixed cost leverage; if cost-saving measures and volume gains in the segment do not materialize as planned, it could compress net margins and ultimately depress overall earnings.

- Exchange rate volatility, particularly the weakening U.S. dollar, significantly impacts Kemira's reported revenue and EBITDA, exposing the company to unpredictable headwinds that can erode margins and earnings, especially given its international exposure.

- Kemira's ability to optimize working capital and generate adequate operating cash flow is already strained during periods of declining revenue-continued inventory and receivables imbalances amid softened growth could impede future investments, return of capital, and inorganic growth opportunities.

- Heavy reliance on mature geographic markets and core industries (pulp & paper, water treatment) that face structural or secular stagnation, alongside emerging competition from alternative green/biotech water treatment solutions, could gradually erode Kemira's addressable market and revenue streams, directly threatening its long-term growth outlook.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €23.4 for Kemira Oyj based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €24.5, and the most bearish reporting a price target of just €20.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €3.0 billion, earnings will come to €262.8 million, and it would be trading on a PE ratio of 16.7x, assuming you use a discount rate of 6.5%.

- Given the current share price of €19.29, the analyst price target of €23.4 is 17.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.