Key Takeaways

- Separating into Fiskars and Vita is anticipated to enhance operational efficiency, financial performance, and market-focused revenue growth.

- Investment in demand creation and D2C growth is expected to bolster sales, improve margins, and support long-term revenue and earnings growth.

- Significant risks from tariffs, organizational restructuring, and volatile markets could pressure Fiskars' margins and revenue amidst uncertain global consumer sentiment.

Catalysts

About Fiskars Oyj Abp- Manufactures and markets consumer products for indoor and outdoor living in Europe, the Americas, and the Asia Pacific.

- The separation into two legal entities, Fiskars and Vita, is expected to drive operational efficiency and focus, potentially leading to improved financial performance and EBIT growth as they operate independently. This strategic move can enhance revenue generation by allowing each entity to focus on its specific market dynamics.

- The company's investment in demand creation and marketing, particularly for new categories, new product launches, and innovations, is expected to support future revenue growth and improve earnings by driving higher sales and market penetration.

- The direct-to-consumer (D2C) growth of 9% in own retail and e-commerce channels highlights the strength of Fiskars Group's brands, which is likely to boost future revenue streams by capitalizing on direct consumer relationships and higher-margin sales channels.

- Fiskars Group's strategy to mitigate tariff impacts by diversifying sourcing locations outside of China, leveraging European manufacturing, and engaging in productivity improvements is likely to protect net margins and support earnings resilience under challenging external conditions.

- The ongoing improvements in gross margins, notably a 230 basis point increase for Vita and nearly 400 basis points for Fiskars over three years, demonstrate operational efficiencies and pricing power, which are expected to positively impact future profitability and EBIT.

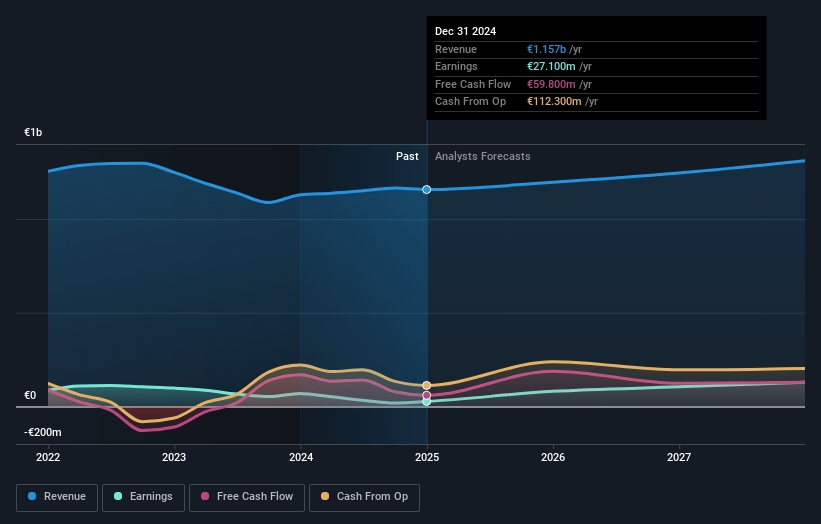

Fiskars Oyj Abp Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Fiskars Oyj Abp's revenue will grow by 3.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.0% today to 8.1% in 3 years time.

- Analysts expect earnings to reach €104.8 million (and earnings per share of €1.3) by about May 2028, up from €11.5 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.4x on those 2028 earnings, down from 102.9x today. This future PE is lower than the current PE for the GB Consumer Durables industry at 59.6x.

- Analysts expect the number of shares outstanding to decline by 0.08% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.59%, as per the Simply Wall St company report.

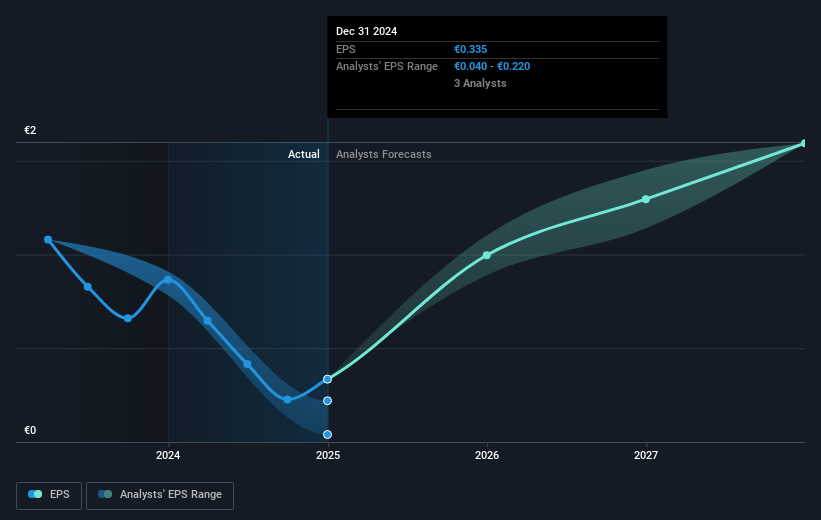

Fiskars Oyj Abp Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The impact of tariffs on products sourced from Asia, particularly China, could increase supply chain costs, potentially reducing net margins if Fiskars is unable to pass these costs onto consumers.

- The ongoing reorganization into two separate entities (Fiskars and Vita) carries execution risk, which could lead to increased expenses and operational inefficiencies, impacting future earnings.

- Challenges in Chinese consumer sentiment and lower sales in China could hurt revenue growth, considering China is a significant market.

- High inventory levels in the U.S. due to tariff-related prebuying might lead to inefficiencies and excess stock, negatively affecting cash flow and revenue if demand fluctuates.

- The dynamic regulatory environment, particularly in the U.S., combined with uncertain consumer confidence globally, adds unpredictability to Fiskars' financial outlook, possibly impacting revenue and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €14.75 for Fiskars Oyj Abp based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €1.3 billion, earnings will come to €104.8 million, and it would be trading on a PE ratio of 14.4x, assuming you use a discount rate of 8.6%.

- Given the current share price of €14.64, the analyst price target of €14.75 is 0.7% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.