Key Takeaways

- Strategic acquisitions and capacity expansion are expected to enhance global manufacturing, supporting revenue growth through increased patient reach.

- Focus on innovative treatments and pipeline expansion aims to strengthen market position and could drive sustainable revenue and earnings growth.

- Rising carbon emissions, heavy CapEx, and R&D costs, along with supply chain challenges, threaten Novo Nordisk's financial stability and shareholder returns.

Catalysts

About Novo Nordisk- Engages in the research and development, manufacture, and distribution of pharmaceutical products in Europe, the Middle East, Africa, Mainland China, Hong Kong, Taiwan, North America, and internationally.

- Novo Nordisk plans to expand patient reach significantly by increasing its manufacturing capacity with the recent acquisition of Catalent sites, expected to enhance global fill and finish capabilities. This supports volume growth and is likely to impact revenue positively in the coming years.

- The R&D pipeline includes potential new treatments, such as CagriSema and amycretin, which show promise for obesity management with strong clinical study results. Successful launches could drive future revenue and market growth.

- Novo Nordisk is strategically enhancing its portfolio with semaglutide 7.2 milligrams and oral semaglutide 25 milligrams, which may offer competitive advantages in various patient segments. These additions could positively impact revenue through market expansion and increased product differentiation.

- The company anticipates significant sales growth driven by GLP-1-based treatments for obesity and diabetes care, reflecting ongoing scaling of the supply chain and continued demand. This is expected to contribute to higher revenue and sustained earnings growth.

- With a strategy focused on innovative treatments and an expanded product portfolio, including next-generation obesity drugs, Novo Nordisk aims to maintain its leadership position and competitive advantage, potentially improving net margins through a higher value product mix.

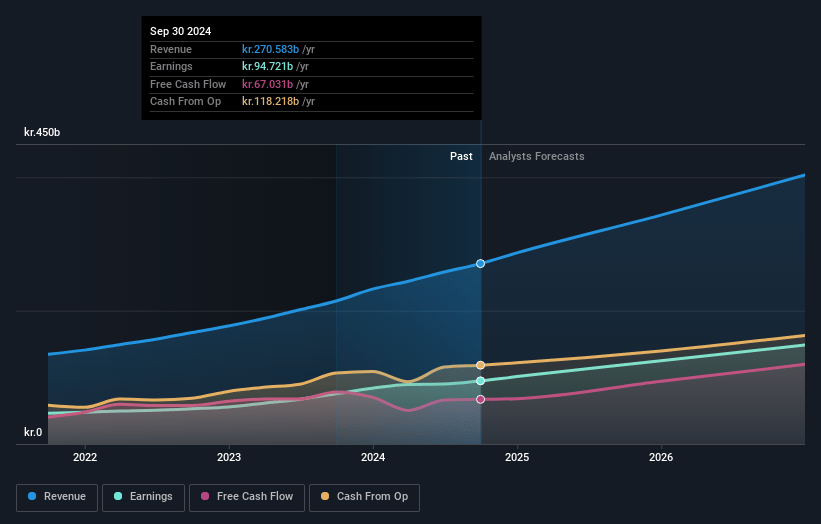

Novo Nordisk Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Novo Nordisk's revenue will grow by 15.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 34.8% today to 36.8% in 3 years time.

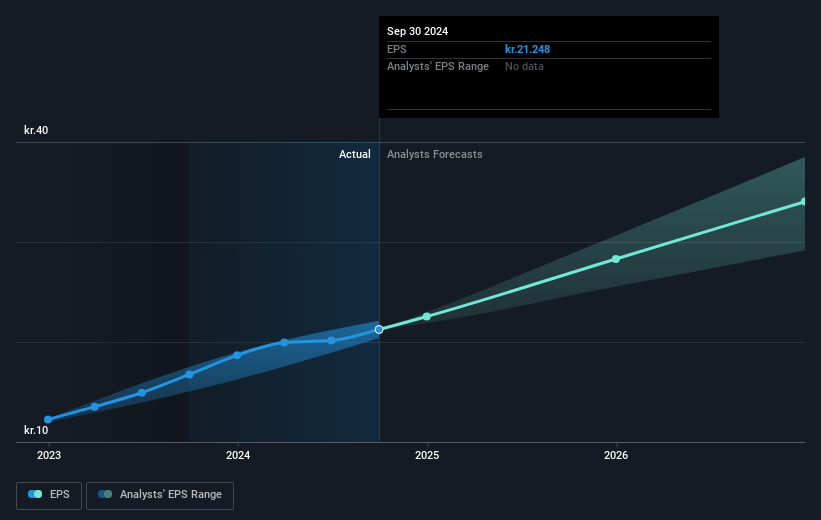

- Analysts expect earnings to reach DKK 164.0 billion (and earnings per share of DKK 37.06) by about April 2028, up from DKK 101.0 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting DKK198.7 billion in earnings, and the most bearish expecting DKK143.2 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 22.3x on those 2028 earnings, up from 17.9x today. This future PE is greater than the current PE for the US Pharmaceuticals industry at 17.1x.

- Analysts expect the number of shares outstanding to decline by 0.42% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 4.74%, as per the Simply Wall St company report.

Novo Nordisk Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Novo Nordisk's total carbon emissions increased by 23% in 2024 due to increased production volumes and capital expenditures, which may impact net margins.

- The significant CapEx investments and the acquisition of Catalent sites could negatively affect free cash flow if not managed efficiently, impacting overall financial stability.

- High research and development costs, increased by 48% in 2024 due to late-stage clinical trials and early research activities, could pressure net profit margins if new products do not meet market expectations.

- The absence of a new share buyback program due to expanded CapEx could reduce short-term shareholder returns, which might affect stock valuations.

- Supply chain challenges, including reliance on evolving market dynamics and potential compound pharmacy impacts, could affect revenue growth if not addressed promptly.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of DKK726.821 for Novo Nordisk based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of DKK1150.0, and the most bearish reporting a price target of just DKK405.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be DKK445.9 billion, earnings will come to DKK164.0 billion, and it would be trading on a PE ratio of 22.3x, assuming you use a discount rate of 4.7%.

- Given the current share price of DKK407.9, the analyst price target of DKK726.82 is 43.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.