Key Takeaways

- Growth in Continence and Ostomy Care, driven by new products, could boost revenue and market share, aided by positive market feedback.

- Simplification and expansion strategies, including divestment and manufacturing improvements, may enhance margins and drive profitability.

- Foreign exchange challenges, divestments, product recalls, tax liabilities, and legal proceedings may negatively affect Coloplast's revenue growth, margins, and net earnings.

Catalysts

About Coloplast- Engages in the development and sale of intimate healthcare products and services in Denmark, the United States, the United Kingdom, France, and internationally.

- The approval and upcoming implementation of the Local Coverage Determination (LCD) policy for skin substitutes, which includes Kerecis’ products, is expected to potentially increase volumes for Diabetic Foot Ulcers and steer away from competitors, thereby impacting revenue positively.

- The divestment of the Skin Care business is part of a simplicity and profitability improvement program in the Advanced Wound Care segment. This is expected to contribute an improvement of around 30 basis points to the EBIT margin for the financial year.

- The successful growth of the Continence Care and Ostomy Care businesses, particularly driven by the male catheter Luja and the SenSura Mio portfolio, respectively, could lead to higher revenue and market share gains, especially as new markets are introduced and feedback remains positive.

- Continued investments and expansions in manufacturing operations in Costa Rica and Portugal are expected to provide savings and improve efficiency over time, which could favorably impact gross margins despite initial ramp-up costs.

- The anticipated resolution of the Bladder Health product recall and resumption of sales is expected to recover lost revenue, particularly in emerging markets, contributing to a stronger financial performance in the second half of the fiscal year.

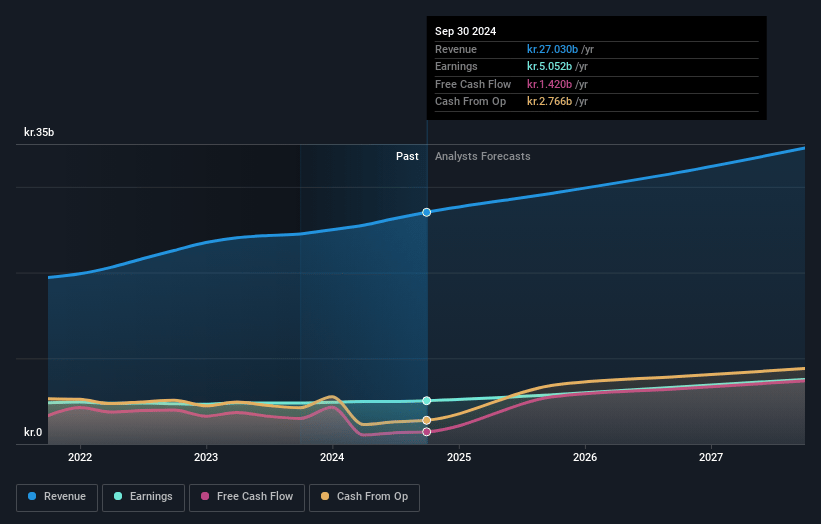

Coloplast Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Coloplast's revenue will grow by 8.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 17.8% today to 21.7% in 3 years time.

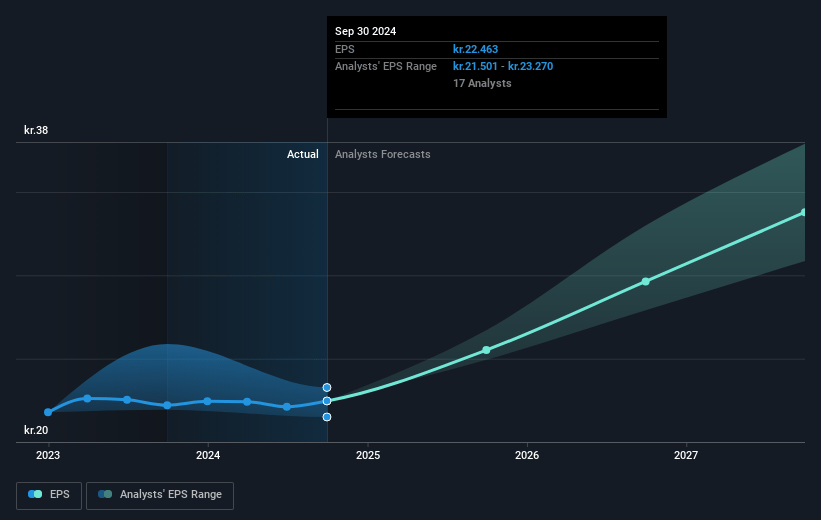

- Analysts expect earnings to reach DKK 7.5 billion (and earnings per share of DKK 33.75) by about May 2028, up from DKK 4.9 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 31.9x on those 2028 earnings, down from 34.2x today. This future PE is greater than the current PE for the GB Medical Equipment industry at 29.6x.

- Analysts expect the number of shares outstanding to grow by 0.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.74%, as per the Simply Wall St company report.

Coloplast Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The divestment of Coloplast's Skin Care business will reduce reported revenue by around DKK 350 million or 1.5 percentage points, impacting overall revenue growth for '24-'25.

- Negative impacts from foreign exchange rates, particularly the depreciation of Emerging market currencies like the Argentinian peso and Brazilian real against the Danish krone, have reduced reported revenue and could continue to impact financial results.

- The voluntary product recall in Interventional Urology due to packaging issues has already impacted growth and will continue to pose challenges in the short term, potentially affecting revenue recovery throughout the year.

- The effective tax rate for this year will be significantly impacted by an extraordinary tax expense related to the transfer of Kerecis intellectual property, which will notably affect net earnings.

- Court proceedings in Denmark related to competition laws could pose reputational risks and the potential for unforeseen liabilities, potentially impacting margins if regulatory findings are unfavorable.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of DKK899.2 for Coloplast based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of DKK1050.0, and the most bearish reporting a price target of just DKK694.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be DKK34.8 billion, earnings will come to DKK7.5 billion, and it would be trading on a PE ratio of 31.9x, assuming you use a discount rate of 5.7%.

- Given the current share price of DKK742.0, the analyst price target of DKK899.2 is 17.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.